Despite public sector banks' big rally in the last one year, they are still trading at a huge discount as compared to private sector banks in terms of the price-to-book ratio. The main reason behind such a huge gap is the quality of assets, which is quite low in the case of public sector banks, represented by high non-performing assets (NPAs).

Comparing the top five banks as per market capitalisation each in the public sector and the private sector reveals the quantum of difference between them. Have a look at the table and the graphs below.

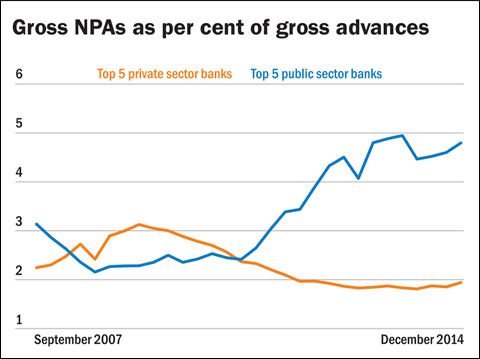

Since 2009 the private sector banks have constantly improved their gross NPAs as per cent of gross advances, whereas the NPAs of the public sector banks have soared to all-time high.

The public sector banks, after improving a while in 2007-2008, again witnessed a significant rise in NPAs due to negligence and new aggressive rules to recognise bad assets. On the other hand, the private sector banks reported higher NPAs during 2008-09 than the public sector banks. This was primarily due to ICICI Bank, which had high NPAs during that time period.

Gross NPAs of top five private and public banks

| Company name | Price to book | Gross NPAs (%) |

| Private sector banks | ||

| HDFC Bank | 5.12 | 1 |

| ICICI Bank | 2.36 | 3.4 |

| Axis Bank | 3.16 | 1.34 |

| Kotak Mahindra Bank | 7.78 | 1.87 |

| IndusInd Bank | 4.71 | 1.05 |

| Public sector banks | ||

| State Bank of India | 1.66 | 4.9 |

| Bank of Baroda | 0.98 | 3.85 |

| Punjab National Bank | 0.79 | 5.97 |

| Canara Bank | 0.73 | 3.35 |

| Central Bank of India | 1.16 | 6.2 |

Ask Value Research ![]()