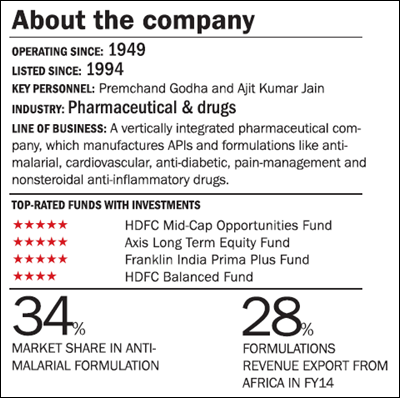

Ipca Laboratories is into pharmaceutical formulations and APIs (active pharmaceutical ingredients). The company is known more for the antimalarial and rheumatoid arthritis solutions. Earlier the company was only into APIs. It has since transformed itself into a complete formulation company, with presence in domestic and international markets. Ipca generates more than 60 per cent of the revenues from exports, with the highest share coming from Europe. From Europe it generated ₹594 crore (18 per cent of the revenues) in FY14. Europe was followed by Africa, with 17 per cent revenue share in FY14. Export formulations accounted for almost 50 per cent of Ipca's revenues in FY14, while the branded generics business accounted for 25 per cent of the exports.

Strengths

Institutional business: Ipca is the market leader in antimalarial formulations and these constitute 35 per cent of the formulations export of the company. The company has a market share of 34 per cent in this segment. The revenues from the antimalarial segment have grown aggressively at a CAGR of 35 per cent, from an estimated ₹146 crore in FY09 to nearly ₹642 crore in FY14. This segment is the most profitable business for the company.

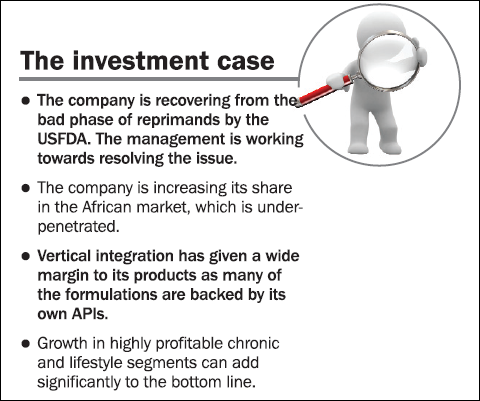

Formulation business: Over the years the company has strategically focused on the finished product formulation business, which has a higher margin than APIs, and managed to grow it by 22 per cent CAGR in the last five years. Formulations, which accounted for 67 per cent of the total revenues in FY09, now contribute 76 per cent of the total revenues. Vertical integration has given a wide margin to its products as many of the formulations are backed by its own APIs.

Shifting of focus from Europe to Africa : Ipca has, over the years, shifted its focus from Europe to Africa in the past five years. Africa is relatively less penetrated and regulated. Africa, which contributed 19 per cent of the exports in FY09, now contributes 28 per cent of the exports and is growing at a high rate of 35 per cent. On the other hand, Europe's contribution to the exports has come down from 38 per cent to 29 per cent during the same period. This has not only diversified Ipca's international market but also insulated it from tougher European norms. However, the export revenue in the American market has also gone up in the same period.

Growth drivers

In the last one quarter, the company had 42 ANDA (abbreviated new drug application) filings, out of which 18 were approved and eight products have already been launched in the US. The company is focusing on the formulations backed by its own APIs. In this regard, its next expansion will still come from the European and American markets. In African countries, which are less regulated, Ipca is trying to establish its brand, and Africa is still an under-penetrated area.

Last year Ipca's Ratlam plant was issued Form 483 by the USFDA. The Form highlighted half-a-dozen violations by the company. Therefore, the company voluntarily decided to hold the export from the plant. Thereafter, in the last quarter, it also got an import alert. The company is working aggressively to resolve the problems. Moreover, recently the US drug regulator exempted its five APIs from ban, and these contribute around 45 per cent of the export revenues to the US. However, this is only a short-term boost as the removal of the ban is a move to avoid shortage of drugs in the US market.

The company's strength has been the domestic formulation business of chronic and lifestyle segments like cardiovasculars, anti-diabetics, pain-management and non-steroidal anti-inflammatory drugs. These segments are very profitable because of their high margins as compared to the antimalarial segment. To further push these products the company has recently expanded the current MR (medical representative) strength to 4,000.

Concerns

Ipca has struggled in the past one year due to regulatory observations on its Ratlam plant in July 2014. Later the company was issued an import alert in January 2015. The export revenues from the APIs to the US market took a hit as the company voluntarily stopped exporting them from the Ratlam plant and is working towards resolving the matter. Second inspection is due in late March and further decision can swing in either side. Any adverse decision can further elongate the company's recovery plan. Moreover, the Ratlam plant had a successful inspection recently by three regulators, EMA, WHO and TGA, which is a positive sign.

The company faces a genetic risk of currency appreciation as 60 per cent of its revenues are from exports. This is the reason its export revenues from the Commonwealth of Independent States (CIS) countries have fallen due to the rupee getting stronger than the ruble. Moreover, currently due to a depreciated currency in the last year, Ipca's FCCB service costs have risen and, therefore, further depreciation may worsen the situation. Therefore, Ipca faces some concern on either-side movement of the currency.

Financials

The revenues have grown at a healthy 20 per cent CAGR. The earnings have grown at 38 per cent in the past five years. This is due to the improvement in the operating margin from 15 per cent in FY09 to 23 per cent in FY14. This improvement is mainly on account of good performance in the formulation business. The return on capital has remained in the attractive area of more than 20 per cent in the past five years. The cash conversion cycle is high, at 98 days. However, it has improved from 140 days in FY09. This is a very healthy sign because relatively low capital will be locked in the working capital.

Valuation and outlook

At the current level, the company is yielding 8 per cent of the operating profits on its enterprise value. This is relatively attractive in the current market. The stock has fallen in the last one year due to USFDA reprimands, but we think that the management should be able to come out of the situation very soon. Dive into this opportunity for the long term if you have high risk appetite and a well-diversified portfolio.

Disclaimer: The analyst owns shares of Ipca Labs in his personal portfolio since September 2014.

This article was originally published on April 01, 2015.

Ask Value Research ![]()