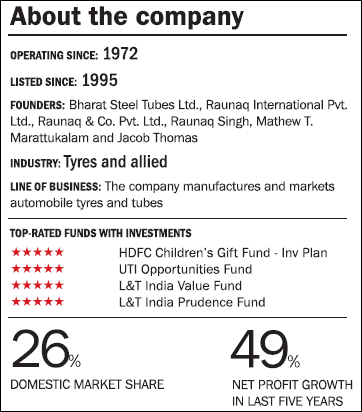

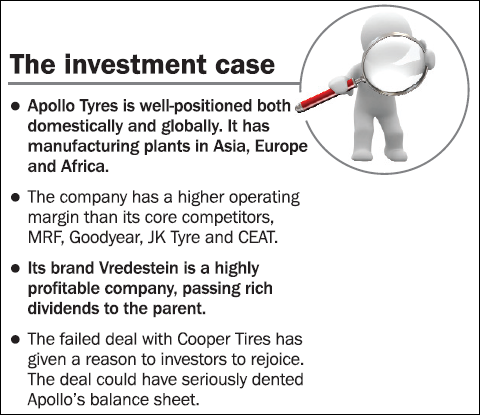

Apollo Tyres manufactures and markets rubber tyres, with a global presence. Headquartered in Gurgaon, Apollo Tyres has manufacturing plants in Asia, Europe and Africa and operates in the segments of passenger cars, light trucks, buses, off-highway and bicycle tyres, retreading material and retreaded tyres. The company's key brands include Apollo, Kaizen, Maloya, Regal and Vredestein.

Its European brand Vredestein, acquired in 2009, is a hundred-year-old brand based in the Netherlands. It designs and manufactures tyres under the Apollo and Vredestein brand names through its offices in Europe and North America. Domestically, it competes with MRF, JK Tyre, CEAT and Balkrishna Industries.

Strengths

Balancing act: Apollo Tyres has positioned itself very well in the domestic and global markets by balancing both the markets. The company has 26 per cent market share in the domestic commercial vehicle tyre segment and 23 per cent in passenger vehicle segment (as per an ICICI Direct report). Through its European subsidiary Vredestein, it has made its global presence strong.

High margin: The company has a high revenue share from the replacement market, which is more than 70 per cent. The replacement market comes with a high margin. Therefore, Apollo Tyres has a higher operating margin than the core competitors, MRF, Goodyear, CEAT and JK Tyre, with the only exception of Balkrishna Industries, which is wholly into the higher-yielding off-road tyre segment.

Global edge: Vredestein specialises in high performance summer and winter tyres and is a highly profit-making company, thus churning rich dividends for the parent company. Vredestein has an operating margin of 18 per cent and a net margin of 14 per cent in FY14, which are much better than domestic business margins. With a relatively higher return on equity, Vredestein is operating at near 90 per cent of its capacity, giving further room for capital expansion and volume growth.

Failed deal with Cooper: Apollo Tyres already has a well-balanced and geographically diversified successful business. But in a hurry to grow aggressively globally, it had hit some hurdles in the medium term with its initial plans to acquire the US-based Cooper Tires. The major issue was the huge debt to be raised for Cooper, which could have raised the consolidated debt/equity substantially. With the failed deal, the company has a debt/equity ratio of 0.30 in FY14, which has improved from 1.0 in FY11. Moreover, there is scope for growth organically with its existing ventures through capital investments, without going for new acquisitions.

Growth drivers

Apollo is already operating in the range of 80-90 per cent of the capacity in the domestic as well as in the European plants. Hence, there is scope for expansion. The Vredestein plant in Europe is working at 90 per cent of capacity and has therefore recently finalised a new greenfield facility in Hungary. The company will be investing EUR 450 million and in addition it has also received the European Union's regulatory approval for a grant of EUR 95.7 million as aid. The new facility will have a capacity of 5.5 million passenger car tyres and 0.7 million truck tyres per annum and is expected to commence in 2017.

Its Chennai plant is operating at 80 per cent of the capacity, and to cater to the future demand the company has planned for expansion, wherein it has earmarked ₹2,000 crore. This capital expenditure will be incurred in FY15 and FY16, and as per the management guidance the company may look towards Kerala for further growth. Moreover, to add to the domestic product portfolio, the company has recently launched its premium brand Vredestein in India to cater to high-end cars and SUVs.

On the cost front, Apollo Tyres, along with its peers, has enjoyed low prices of rubber, its key raw material. The prices in the international market have remained under pressure due to more supply than the demand. The current price of rubber is hovering around ₹120 per kg, which is almost half of the price in 2011. The demand-supply gap is most likely to continue till next year, which means prices will remain under pressure. However, this is just a medium-term relief for the companies in the sector.

Concerns

The principal risk includes its key raw material rubber, which forms almost 60 per cent of the total raw materials. The price of rubber is quite volatile in nature and is dependent on international prices. Though the prices are currently at a low level, any unexpected rise in the prices in future may hamper the profitability margins.

The pace of volume growth is another concern. It has remained subdued in the last few years, in the range of 5-6 per cent in the domestic market and around 7 per cent in the global market. In the absence of volume growth, the revenue may come under pressure due to recent price cuts owing to tough competition in the European and Indian markets. Pricing is a major issue in the tyre sector as smaller unorganised players sometimes spoil the pricing war.

Financials

Apollo has improved its financial position in the last few years despite intensive capital expenditures by utilising the reserves effectively and cutting down the debt at the same time. It has witnessed annualised revenue growth of 21 per cent in the last five years and net profit growth of 49 per cent due to low interest and input costs. Apollo has also managed to generate a positive free cash flow of Rs 786 crore in FY14. The return on equity and capital both have averaged around 21 per cent in the past five years.

Valuation and outlook

At the current price, the company is trading at 9.57 times its trailing twelve-month earnings. This is close to its five-year median of 7.39. The stock has an earning yield of 10.45 per cent and a low debt to equity ratio of 0.56 which makes it attractive. The recent surge in the stock factors in the correction in the price last year in the anticipation of a deal with Cooper. Apollo is still cheaper than its counterpart MRF, Balkrishna Industries and CEAT.

This article was originally published on January 28, 2015.

Ask Value Research ![]()