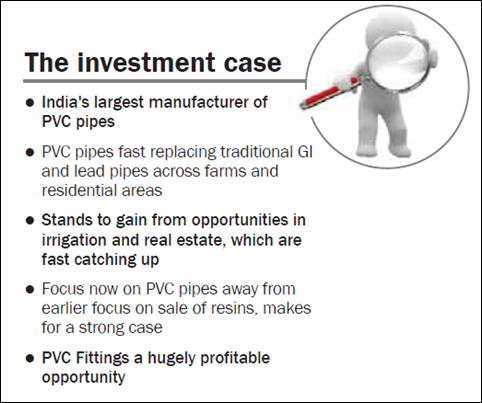

There is a quiet revolution happening in our fields. Farmers are replacing galvanised iron (GI) and lead pipes with PVC pipes. Installing PVC pipes has a number of advantages: they are lightweight, weighing about one-eighth of lead pipes therefore easy to handle and transport, highly resistant to fire, chemicals and the elements. They are also around 20-25 per cent cheaper than GI pipes and more durable with expected life of 20-25 years compared to that of 10-15 years of the latter.

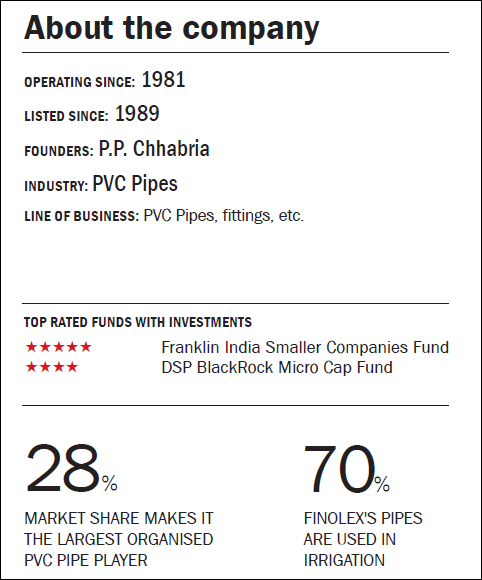

Many companies have made good money selling PVC pipes. Finolex, the largest PVC pipe manufacturer is one of the foremost. Formed a little over 30 years ago, Finolex has captured 28 per cent of the organised market for PVC pipes in the country. Here is why Finolex's journey is far from over.

Strength

Market leader: The domestic PVC pipe market is estimated at around 1.5 million metric tonnes. Half of this market is unorganised and highly fragmented. Organised players bring consistent quality and deeper distribution network that allows them to take market share from the unorganised players. Finolex is the largest PVC pipe manufacturer in India with a capacity of 210,000 MT. It also manufactures PVC fittings and specialty pipes for soil, waste and rain water. More than 70 per cent of Finolex's pipes are used in irrigation.

Opportunity in irrigation: Pipes are an indispensable part of irrigation. Given the advantages PVC has over traditional galvanised iron and lead pipes, the trend of replacement with PVC pipes is likely to continue. There is still a huge untapped opportunity in agriculture. Gross irrigated area constitutes only 45 per cent of the total cropped area. That means PVC pipe manufacturers like Finolex have still far to go.

Opportunity in real estate: PVC pipes are increasingly replacing galvanised iron and lead pipes in homes and residential areas too. Common uses are in water pipes, waste pipes, doors, windows, partitions, electrical casings, etc. Any improvement in the housing market will spur demand for Finolex's residential PVC demand.

Change in strategy: Finolex had initially set its eyes on the lucrative PVC resin market, selling resin to other manufacturers. It now changed its focus to PVC pipes and fittings that is fast emerging a huge opportunity everyone wants to get into. It now uses its own captive resin production for its pipes and fittings. It also intends to utilise the excess capacity of resins to produce pipes. The company is using around 60 per cent of its resin production for its own use. This figure is likely to go up to 90 per cent levels in the next 2-3 years.

Big bucks in PVC fittings: One of the most uninteresting things you can find is PVC fittings. These are elbows, Tees, couplers, reducers and the sort. What many do not know is that this is one of the most profitable items on sale. PVC fittings command a premium of around 25-30 per cent. Finolex makes 30 per cent on fittings. But fittings comprise a small part of Finolex' sales - at only 7.3 per cent. Finolex wants to take this to 10-12 per cent levels in the next couple of years.

Capacity gains: Being the leader is not enough. Finolex's pipe capacity that has grown 18.6 per cent CAGR between FY07-FY14 is building more. In the next three years, Finolex aims to have a capacity of 330,000 MT - that's a little more than 40 per over its existing capacity. This Brownfield expansion is estimated to cost ₹150 crore.

Better current year outlook: The current year has started with a good show. In the June 2014 quarter pipe realisations jumped 15 per cent over the previous year aided by price hikes. Revenue, as a result was up 25 per cent. The management expects pipe and fittings volume to grow by 15 per cent this year. Lower raw material costs and lower forex losses helped Ebitda margin expand by 910 basis points (y-o-y) to 16.3 per cent. Price hikes should help keep margins up.

Higher return ratios ahead: Finolex suffered in the last couple of years on account of forex losses but the company is now wiser. Hedges are now at 70 per cent levels - up from 50 per cent levels in recent past. Margins are inching up too on the back of price hikes and lower buyer credit that is down from 360 to 90 days. Together, these factors should help Finolex post better returns on capital numbers this year and in the future.

Concerns

Dependence on monsoons: With more than 70 per cent of its revenues derived from the agriculture, Finolex's fortunes are linked to the volatility of monsoons. Lower than average rain or even drought that can result in lower income for the farmer will impact investment to improve irrigation systems.

Raw material price volatility. Finolex also has to face the risk of volatility in raw material prices. Finolex's primary raw material, EDC (ethylene di-chloride) is a derivative of ethylene which in turn is derived from crude oil. Price movement of crude therefore has a direct impact on the company's bottom-line as imports are the primary source of the company's raw material. Utilising its own resins for its pipes and fittings will further help reduce raw material price volatility in the quarters ahead.

Forex losses: Imports of raw materials is why the company suffered forex losses in the past. Finolex has sought to correct its past losses with measures mentioned above but notwithstanding its precautions, forex losses cannot really be ruled out in the future.

Financials

Finolex's revenues have compounded by nine per cent annually in the last five years. Earnings per share (EPS) was up 14 per cent during this period. Operating margin averaged at 12 per cent but is likely to go up this year on the back of price hikes and lower raw material prices.

Valuations

Finolex trades at a PE of 18 times its ttm earnings: Valuations are higher than they were a year back but that is now true for most of the market. Finolex has multiple growth drivers that promise to propel the company on the fast growth lane. Its past successes provide confidence the company will capture these opportunities ahead. Buy with a five year horizon.

This article was originally published on September 25, 2014.

Ask Value Research ![]()