Incorporated in 1998 through a joint venture between GAIL, Bharat Petroleum and the Delhi Government, Indraprastha Gas Limited (IGL) is engaged in retail gas distribution business for supply of CNG to transport sector and PNG to domestic, industrial and commercial sectors in Delhi and National Capital Region. It is also engaged in the manufacture of CNG. Currently, IGL has 290 CNG stations, over 3,90,000 residential customers, 922 commercial customers and 401 industrial customers.

Strengths

A gas purchase agreement with its promoter, GAIL, ensures a constant supply of gas at competitive prices that is essential for the growth of the company. This agreement also ensures priority supply of gas in case of any disruption in supply.

* Firm allocation of gas for the region allows IGL to sell CNG at one of the lowest retail price in the country and still protect its margins

* The company does not have any competition and enjoys a premium position in the region it operates in. It is the sole supplier of CNG and PNG in Delhi, Noida, Greater Noida and Ghaziabad, and plans to promote wider usage of gas for various applications through co-generation, gas geysers, gensets, etc.

* The price difference between CNG and petrol will continue to drive the large scale conversion of petrol-driven vehicles to CNG mode. As of now, CNG offers around 11-15 per cent savings over other fuels, thus making it a preferred choice

* Further, more and more automobile companies are introducing CNG variants with pre-fitted kits to tap the growth opportunity which is bound to increase the demand for CNG

* PNG is emerging as a key source of energy for commercial and industrial usage. With increasing prices of LPG and restrictions on the number of cylinders, more and more households are now keen to shift on to PNG. This provides ample opportunity for IGL in future

Growth drivers

IGL has a robust infrastructure of CNG stations and pipeline networks that ensures easy availability to its customers. The company has already shown its expertise in developing and rolling out city gas distribution networks in NCR and this gives it an edge to tap any further growth opportunities in newer areas.

* IGL has a long-term gas sale contract with its largest customer Delhi Transport Corporation, which accounts for nearly 20 per cent of IGL’s sales

* The company is also bound to benefit from the Delhi Government’s initiative to expand the city’s public transport system. More than 5,000 buses and 45,000 autorickshaws are expected to be added by 2015-16

To reduce the burden of the rise in APM prices, IGL is all set to increase the price of CNG by ₹10-11 per kg by March 2014. The state government too is supportive and has not intervened in the company’s pricing decision. This increase should improve its margins that have been under pressure of late. Despite the price rise, IGL should still continue to sell gas cheaper than any other state

* Apart from the current areas of operations, IGL is also targeting industrial and commercial segment for further expanding its PNG network

* RLNG prices are at its peak. Any further correction in the prices or currency appreciation will make PNG competitive as compared to furnace oil

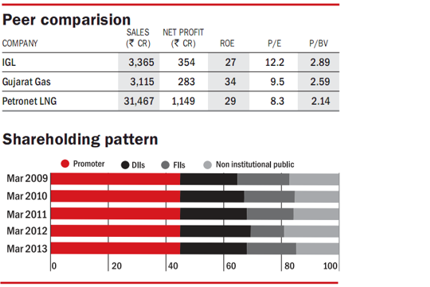

CNG is the major component that contributes to IGL’s revenue -- 75 per cent. While industrial segment (15 per cent) and domestic PNG (10 per cent) make up for the rest. It reported a net sales of ₹3,365 crore for FY13, a 34 per cent increase from last year owing to a strong market presence and a good distribution network.

However, net profit only grew at 16 per cent y-o-y due to increase in raw material costs. The company’s debt as for FY13 stands at ₹303 crore, down 14.5 per cent compared to last year’s debt of ₹347 crore. Its debt to equity stands at 0.44.

Valuations

At the current price of 281, the stock is trading at a price to earnings of 11.12 which is at 24 per cent discount to its 5-year average price to earnings of 13.83. Price to book value to stands at 2.64, lower than the 5-year average of 3.44. Revenues and profits have grown at CAGR of 32.27 per cent and 17.3 per cent. Volumes might be under pressure as of now but IGL’s ability to maintain gross spreads in absolute terms, coupled with decent volume growth, will drive revenue and profit growth.

This article was originally published on September 06, 2013.

Ask Value Research ![]()