Any long-term investor would testify that commodities are a cyclical trade. You buy when the commodities are low and sell when high. But, commodity investing is not this simple. First, you need to know where the commodity cycle currently stands at. There you would need some expertise in estimating how those prices could move especially those that are affected by global dynamics. In spite of the uncertainties, many investors think it as value to buy commodities when the cycle is down. We show why it isn't.

Busting the Myth

The key factor determining commodity prices are not the production costs at some mine. It is simply the supply and demand dynamics that influence prices. As such, there is no way you can assess how much a commodity company will make this financial year independent of the commodity prices that will follow this year. Think of tea prices. Tea is largely impacted by global factors. If the production fails in Argentina, prices will go up in India. Or if there is bumper growth in Kenya, tea prices will cool down. As such, it is very difficult to foresee how commodity prices will shape up going forward.

Buffett is not into investing in commodities. "The problem with commodities is that you are betting on what someone else would pay for in six months. The commodity itself isn't going to do anything for you, it's an entirely different game to buy a lump of something and hope that somebody else pays you more for that lump two years from now than it is to buy something that you expect to produce income for you over time." (CNBC Interview, 2011).

Eye on competitive advantages

But as in other companies, investing in commodity companies with competitive advantages still pays off. In an undifferentiated commodity-like business, being the lowest cost producer is a big competitive advantage. Says Buffett, "Commodity businesses have a lot of risk unless you're a low-cost producer, because the low-cost producer can put you out of business. Our textile business was not the low-cost producer. We had fine management, everybody worked hard, we had cooperative unions, all kinds of things. But we weren't the low-cost producers so it was a risky business. The guy who could sell it cheaper than we could made it risky for us". (Berkshire Annual Meeting 1997).

Buffett has in the past invested in Posco -- a steel company because its competitive advantages. Here is his rationale, "We think Posco is the best steel company in the world.

When we bought it, it was at 4-5x earnings, had a debt-free balance sheet and was the low-cost producer". (Berkshire Annual Meeting 2007)

Commodity companies have another characteristic that Buffett does not like -- they are all capital intensive businesses and require heavy investments just to stay in the game. Says Buffett, "You can find some businesses with minimal capital investment. See's Candy does not require much capital investment. It's a small business, but a wonderful business -- a far better business, adjusted for size, than any steel or oil business. We do everything we can to make it bigger. We do not have a bias towards any commodity-related business. If we have any bias, it's against,"(Berkshire Annual Meeting 2007).

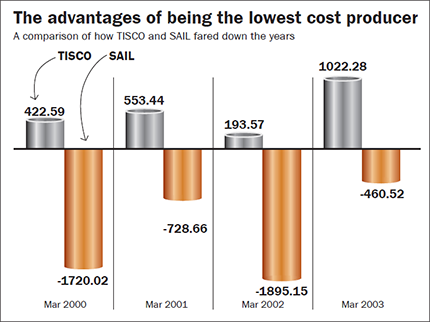

The Indian steel industry is a classic example. When the steel cycle was down between 2000-2003, many steel companies lost money quarter-after-quarter for years at a stretch. Frontline companies like SAIL and JSW Steel continued to remain in the dumps as the cycle remained down. Then there was TISCO (now Tata Steel) one of the lowest cost producers of steel globally. TISCO did get affected by the cycle, but by virtue of its competitive advantage, TISCO did not report a single quarter of losses in the above mentioned period.

With this we end the series on investing myths. Please click here to read the 11 investing myths.

This series was originally published in August 2013.

This article was originally published on August 29, 2013.

Ask Value Research ![]()