Summary: Fixed income investing often comes with a trade-off between returns, risk and predictability. But there’s a fast-growing category that offers a refreshing middle ground. This article breaks down what makes these funds tick and whether they deserve a slot in your portfolio.

Target maturity funds (TMFs) have quickly risen to prominence in the debt fund space. In 2020, just one TMF was launched. But by 2022, the category saw a sharp uptick with 52 new launches that year alone. The momentum has continued, with another 53 TMFs entering the market since then.

Clearly, TMFs are on a roll. But does that mean they deserve a place in your portfolio? Before we answer that, let’s get to know these funds a little better.

What are TMFs?

Target maturity funds are a type of debt funds that come with a fixed maturity date. Basically, these invest in bonds that mature around the same time. Stay invested till the end, and you get your capital back along with the returns earned. Simple, predictable and low on surprises (as long as you don’t bail early).

TMFs are passively managed, meaning they track a bond index and don’t rely on star fund managers making active calls. They’re the debt cousins of passive equity funds: quiet, rule-following and refreshingly low-maintenance.

Being open-ended, TMFs do offer the flexibility to withdraw anytime, but doing so can make your returns less predictable. For best results, it’s ideal to stay invested till maturity.

Category snapshot

There are 109 target maturity funds currently available, including ETFs and FoFs, with combined assets under management (AUM) of Rs 1.88 lakh crore. Interestingly, just eight Bharat Bond ETFs and their FoFs account for a massive 41 per cent of the total AUM, highlighting where investors are placing their biggest bets.

Being passively managed, TMFs come with relatively lower expense ratios compared to other debt funds. For instance, the average expense ratio for TMFs in direct plans is around 0.17 per cent, compared to 0.37 per cent for short-duration funds. While 0.37 per cent isn’t particularly high, TMFs still offer a more cost-efficient option for investors looking to keep expenses minimal.

TMFs also come with different maturity timelines. To see where most of the money is flowing, we grouped them into various maturity buckets and analysed the number of funds and their total AUM in each.

How safe are they?

TMFs largely invest in high-quality, low-risk debt instruments, primarily government securities and AAA-rated PSU and corporate bonds. In fact, out of 103 TMFs (excluding five FoFs and one newly launched fund), 100 funds have over 90 per cent of their portfolios in such safe assets, keeping credit risk to a bare minimum.

This puts them on par with fixed deposits (FDs) in terms of safety, a comparison we’ll explore shortly.

TMF returns: What to expect

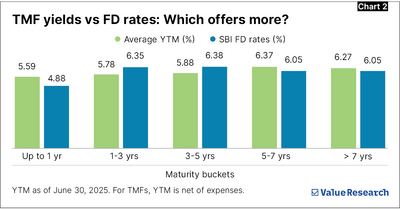

As mentioned earlier, TMFs come with different maturity timelines. To gauge the returns investors can expect, we analysed the yield to maturity (YTM) of TMFs across various maturity buckets. YTM gives a good estimate of your annual return, provided you invest now and stay put till maturity.

For a fair comparison, we also looked at SBI’s fixed deposit (FD) rates for similar timeframes. Chart 2 summarises how TMFs stack up against FDs across various maturity brackets.

Currently, TMFs in the up to one-year, 5–7-year, and 7+ year maturity buckets offer higher yields than SBI FDs. In contrast, FDs have a slight edge in the 1–3 year and 3–5 year segments. That said, the difference in returns isn’t stark, which means neither option is a clear winner on this front.

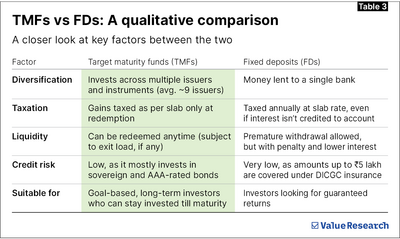

Now, let’s move beyond returns and evaluate how TMFs stack up against FDs on other important parameters. Table 3 highlights the key qualitative differences.

Final words

Target maturity funds are built for investors who value predictability and discipline in their debt allocation. With defined maturity dates and transparent structures, they offer clarity and consistency.

TMFs also serve as a tax-efficient alternative to fixed deposits, especially for longer horizons and are well-suited for those investing a larger corpus while looking to manage credit risk, given the higher issuer concentration in traditional options like FDs.

The key is to stay invested till maturity to truly benefit. For a straightforward, low-maintenance way to grow your fixed income allocation, target maturity funds are well worth considering.

That said, choosing the right fund requires more than just matching maturity dates.

At Value Research Fund Advisor, we look beyond yield and focus on the overall fit—how funds complement your portfolio, match your time horizon and help manage risk.

This article was originally published on August 20, 2025.

Ask Value Research ![]()