Summary: Everyone wants high returns, but not everyone can handle the swings that come with them. This piece dives into how mixing asset classes can not only smooth your investment ride, but also improve long-term returns. Here’s the surprising science behind asset allocation.

The Sensex has compounded at about 14 per cent annually since India’s liberalisation in the early 1990s.

Yet, if one looks at yearly returns, there is almost no year where the Sensex hasn’t fallen 10–20 per cent, and sometimes 30–50 per cent, from peak to trough. This is why compounding in Indian equities is tempting in theory but tough in practice.

Over the last 15 years, equity (BSE Sensex TRI), debt (CRISIL Short Term Bond Index), gold (MCX Gold INR) and global equities (S&P 500 INR) have taken turns at the top. Equity delivered positive returns in 11 of 15 years, with highs like FY21’s 69.8 per cent and lows like FY20’s -22.9 per cent. Debt was positive every year, offering stable and consistent, but low returns. Gold shone in crisis years but lagged elsewhere.

If you’re heavily into equity and expect to maximise outcomes, you must:

- Be one of those Teflon-coated equity investors who don’t lose sleep over market declines.

- Tolerate swings of -50 to +50 per cent in a year.

- Not depend on investments for near-term needs.

- Trust that equities follow long-term economic and corporate growth.

If you don’t tick on every one of the above and some more, then you’d better practice the discipline of appropriate asset allocation. Diversifying across uncorrelated assets cushions volatility, avoids overreliance on any single bet and helps you stay invested.

Hence, if you are not the kind of equity investor that I described as teflon-coated, then you’d better be gold-coated and include fixed income too, in good measure, into your portfolio mix to balance the volatility. Just as in Chemistry, within asset allocation, various asset classes perform differently when combined, depending on the type of asset class and the allocation mix. To elaborate further, let us understand the return-volatility dynamics under various chemistry compositions of asset classes of equity, bond and gold.

Adding equity ≠ always adding risk

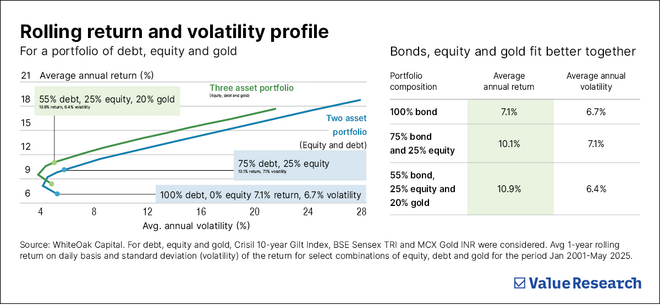

Generally, it is perceived that if we add equity to a bond portfolio, we increase the portfolio’s risk as measured by its volatility (standard deviation or width in the range of investment outcomes relative to the average outcome). But that is not true, always! A 100 per cent bond portfolio (CRISIL 10 Year Gilt Index) has delivered an average return of 7.1 per cent with a volatility of 6.7 per cent over the past ~25 years; by adding 10 per cent equity (BSE Sensex TRI), volatility reduces to 5.9 per cent, and the average return improves by 1.2 per cent.

It is also notable that a 75 per cent bond and 25 per cent equity combination has delivered a 10.1 per cent return on 7.1 per cent volatility. This combination outperforms the 100 per cent bond portfolio on average with a 3.0 per cent higher return over just a 0.4 per cent higher volatility.

The above two illustrations infer that the asset allocation portfolio has delivered better returns with lower risk as compared to a 100 per cent bond portfolio.

Adding gold further smooths returns

A portfolio with 25 per cent equity, 20 per cent gold and 55 per cent bond has exhibited even lower volatility of 6.4 per cent vs 6.7 per cent of the 100 per cent bond portfolio, with an average return of 10.9 per cent (i.e., about 3.8 per cent higher compared to a 7.1 per cent average return from 100 per cent bond portfolio).

This clearly shows that adding a judicious combination of asset classes can achieve a superior return with lower potential risk at a portfolio level.

Successful asset allocators are those who remain steadfast during market volatility, resisting the temptation to make impulsive decisions based on short-term market trends. The process of rebalancing asset class proportion periodically infuses automatically a contrarian mindset, willing to invest in an asset which has underperformed and has declined in proportion due to relative superior performance of another outperforming asset class.

When no one is willing to consider investing in an asset class, the process of rebalancing from outperformer asset classes to underperforming ones works well; like understanding the value of investing in gold when everyone was “dead” sure about equities. It cannot be done by people who are too sure about any asset class or market pattern or caught up in momentum of the performing asset class of recent times. Successful asset allocators must invest in undervalued assets during downturns and reap the benefits when the market recovers. But for the ability to take advantage of a downturn you need to have money in debt or gold or some other asset class to switch or rebalance from into equity.

Open-mindedness and flexibility are also essential, as these individuals reassess and adjust their portfolios in response to changing economic conditions, not just their own financial goals. By maintaining a disciplined approach, by being contrarian, open-minded and probabilistic, i.e., being open to all possibilities and not being “dead” sure about anything, one can effectively navigate the complexities of the market and achieve sustainable growth in wealth with low volatility over time.

Aashish P Somaiyaa spearheads WhiteOak Capital Asset Management Limited as their CEO. An investor education initative of WhiteOak Capital Asset Management Limited.

Looking to balance returns and risk in your portfolio?

Asset allocation isn’t just theory; it’s the difference between riding out volatility and reacting to it. Whether it’s equity, debt or gold, the right mix can enhance returns and reduce risk.

With Value Research Fund Advisor, our analysts shortlist mutual funds across categories, so you can build a well-diversified portfolio suited to your risk appetite and long-term goals.

Start exploring our research-backed fund picks today.

Ask Value Research ![]()