This erstwhile state-owned company has come of its own since the 2004 acquisition by Tata Sons to create its own niche.

Outlook and valuations

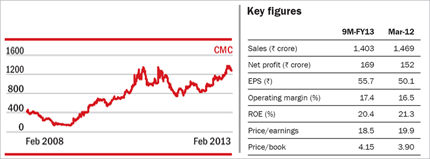

CMC added 26 new clients in Q3, compared to 15 in the previous quarter. Strong growth in its US business along with demand in verticals like embedded software, auto and industrial should help. According to Sandip Agarwal of Edelweiss, the company could add a further Rs 20 per share to its Q4 earnings that could leapfrog earnings by 50 per cent in FY13 (y-o-y). CMC trades at 19 times its ttm earnings. That puts it at its 5 year average trading PE of 19 times.

How they did it

* Strong overall growth and the company's dogged focus on high-margin business have been rewarding. CMC reported a robust overall revenue growth of 7.5 per cent (q-o-q, Dec 2012 quarter)

* International revenue was up 10.6 per cent while US business was up 14 per cent. The Systems Integration (SI) business was up the strongest at 12.4 per cent (q-o-q)

* Margins have gone up from 15.3 per cent (FY12) to 16.7 per cent (9MFY13). The company's focus on high margin verticals of SI (EBIT margin of 21 per cent; up 200 bps, y-o-y) and ITES (EBIT margin of 31.3 per cent-up 410 bps) paid off

* SI and ITES revenues currently stand at 79 per cent, an increase from 72 per cent

This article was originally published on April 05, 2013.

Ask Value Research ![]()