Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

How BAFs allocate between equity and debt and their performance during the recent market downturn

The past year was a bumpy ride for investors, as the market swung wildly between dizzying heights and sharp corrections. In such an unpredictable environment, balanced advantage funds (BAFs), also known as dynamic asset allocation funds, stood out for their promise of cushioning investors from volatility, while still aiming for reasonable returns.

But how well did this approach actually work, and did all BAFs play the same game?

How do BAFs handle market shocks?

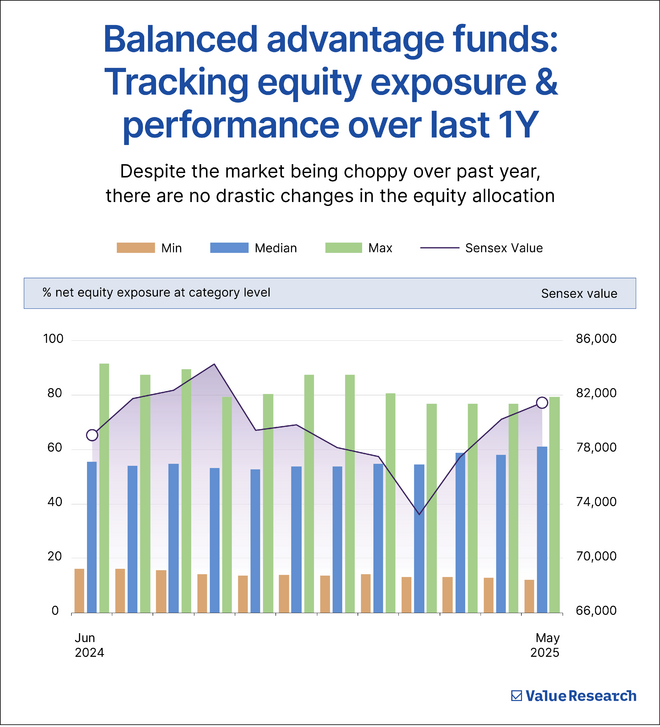

BAFs adjust their exposure to equity and debt based on market valuations, interest rates and other macroeconomic indicators. For instance, when equity valuations are high, they may cut equity exposure and increase allocation to debt or derivatives. When markets are low or undervalued, they may turn more aggressive on equities.

Another key reason BAFs can weather market storms better is their use of hedging strategies. Unlike other hybrid funds that may simply shift assets into debt, many BAFs hedge a portion of their equity exposure using derivatives like futures.

This strategy helps in two ways:

- Reduces downside risk during volatile markets

- Preserves equity classification for tax purposes, even when the net equity risk is low

In effect, investors get the tax benefits of an equity fund, with the risk profile closer to a balanced or debt-oriented portfolio during rough patches.

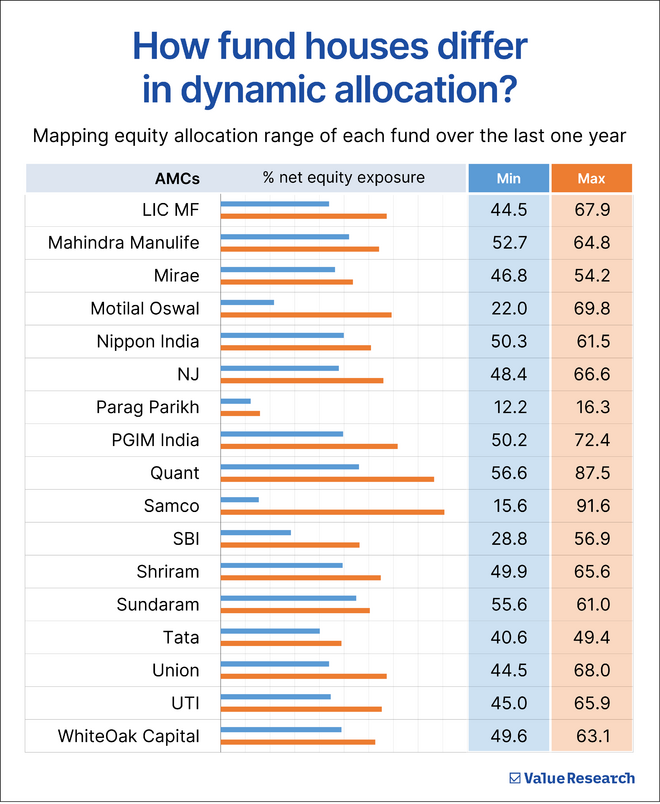

Same category, different fund house moves

This ability to dial risk up or down makes BAFs appealing during uncertain times, but also means that not all BAFs will behave the same way at the same time.

On the conservative end, Parag Parikh’s BAF barely nudged its equity exposure beyond 16.3 per cent, reflecting an extremely cautious stance, possibly prioritising capital protection above all else.

At the other end of the spectrum, fund houses like Samco and Quant took bold calls, pushing their equity exposure close to or above 90 per cent at peak levels. Clearly, these funds leaned more towards participating in market rallies, accepting higher volatility along the way.

Their performance

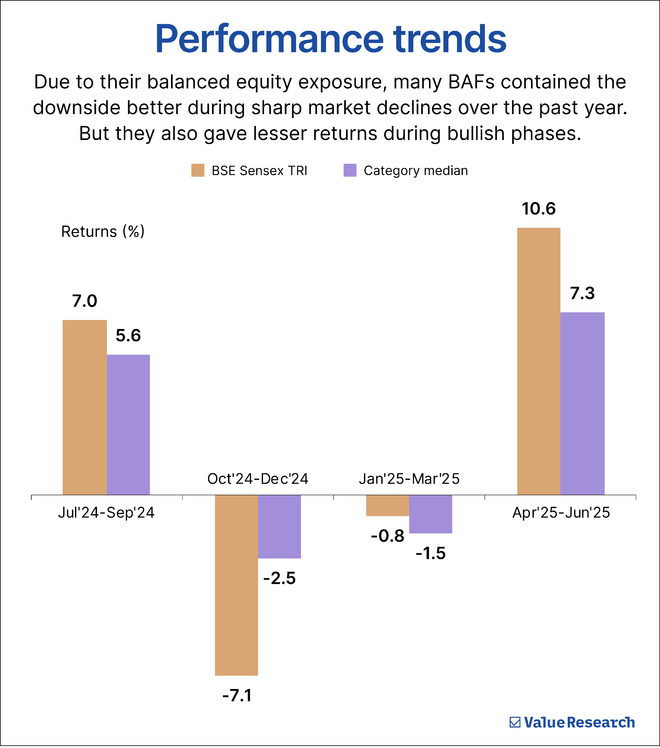

So, has this strategy helped balanced advantage funds?

During the market fall between October 2024 and December 2024, the BSE Sensex TRI sank 7.1 per cent. The BAF, on the other hand, thanks to its dynamic equity-debt allocation, limited its fall to just 2.5 per cent.

But there’s another side to this. When the market soared, like in the April-June 2025 quarter, when the Sensex jumped 10.6 per cent, BAFs could not keep pace, delivering a median return of just 7.3 per cent. A similar case unfolded in July-September 2024, when the broader market delivered 7 per cent while BAFs gave 5.6 per cent.

That’s the trade-off investors must accept. These funds are built for risk-off investors — those who prefer to sacrifice some upside in exchange for protection during downturns.

The takeaway

BAFs shielded investors from the full brunt of market falls. However, that safety net comes at a price. Investors usually miss out on earning outsized gains when the market goes up.

All in all, though, we at Value Research tend to prefer funds with fixed allocations, such as aggressive hybrid or conservative hybrid funds. These offer greater visibility and predictability, since their equity-debt mix doesn’t constantly change. And unlike BAFs, which rely on either models or fund managers to time the market, static allocation funds remove the risk of getting those market calls wrong.

Looking for the right hybrid funds to invest in? Subscribe to Value Research Fund Advisor right now and get a list of our recommended funds that are tailored to your needs and help you meet your financial goals. With our expert guidance, you can be assured of staying on track to building long-term wealth.

Also read: Did MAAFs fall less in the recent market downturn?

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()