Factor investing, which started off as a research concept in the 1960s, has now become one of the most widely used investment strategies. Its widespread acceptance stems from its ability to explain market anomalies, provide systematic investment approaches and deliver consistent risk-adjusted returns over time.

Over the years, factor investing has grown rapidly. Between 2000 and 2024, the assets under management of equity smart-beta funds in the US grew at an annualised rate of nearly 37 per cent, according to Bloomberg Intelligence. As the Indian market evolves, factor investing is set to play a bigger role in portfolio management. But how did this academic concept become a key part of modern investing?

Origins of factor investing: The academic breakthrough

The idea of factor investing originated in the 1960s with CAPM (capital asset pricing model). This model explained how market risk, called 'beta', influenced asset prices. Simply put, CAPM suggested that a stock's returns depended only on how much it moved with the overall market. Imagine a boat floating on water - if the water level rises (market goes up), so does the boat (stock price), and vice versa.

Moving beyond beta: Adding more factors

Over time, researchers found that CAPM had some limitations. It assumed that only market risk mattered, but real-world data showed that other factors played a role, too. Stephen Ross (1976) developed APT (arbitrage pricing theory), which introduced the idea that many factors, beyond just market risk, could explain returns. This was a turning point - it suggested that investors could look beyond beta for better ways to build portfolios.

Studies in the following years further challenged CAPM, showing that additional factors beyond market risk played a significant role in explaining stock returns. These findings identified size and value as key drivers of investment performance. Researchers like Banz (1981) found that small-cap stocks performed better than large caps, a phenomenon called the 'size effect'. Similarly, Basu (1979) discovered that undervalued stocks, or those with low P/E ratios, tended to outperform - a concept now called the 'value effect'. These studies revealed that factors like size and value were key drivers of returns.

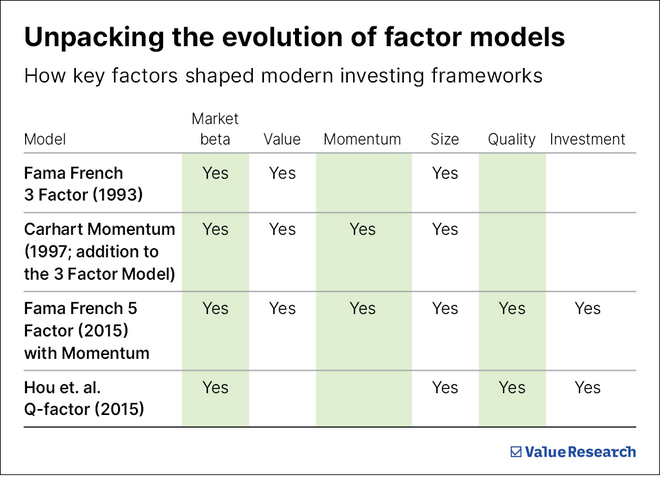

Development of factor models

In 1992, Eugene Fama and Kenneth French built on previous research by introducing the 'Fama-French Three-Factor Model', which added size and value to market beta as key investment factors. This model became the foundation for modern factor investing and led to the launch of factor-based funds, such as the US Small Cap Value Portfolio by Dimensional Fund Advisors (DFA) in 1993.

Later, Mark Carhart (1997) introduced the momentum factor, showing that stocks that had performed well in the past 6-12 months often continued performing well. Unlike value and size, which focus on company fundamentals, momentum investing relies on the market's tendency to continue recent price trends, driven by investor behaviour and sentiment. As research progressed, other factors like quality and low volatility emerged, giving investors even more tools to structure their portfolios.

- Size: Smaller companies often grow faster than large ones but also carry higher risk.

- Value: Stocks that appear cheap compared to their earnings tend to offer higher returns over time.

- Momentum: Stocks that have been rising often continue to perform well for some time.

- Quality: Companies with strong balance sheets and stable profits are safer investments.

- Low volatility: Stocks that experience smaller price swings often provide better risk-adjusted returns.

Real-world validation: Factor investing in action

As factor models gained traction in research, their practical application in portfolio management also became evident. For instance, a 2022 study on Norway's Government Pension Fund (Global) found that most of its active returns came from exposure to factors rather than manager skills. Similarly, a 2013 study on Warren Buffett's investment success (Buffett's Alpha) showed that exposure to value, quality and low-risk factors could explain much of his long-term outperformance.

What lies ahead

Factor-based funds have become widely accessible with the ease of structured data availability, data analytics advancements, and AI-driven insights. At NJ AMC, we recognise the importance of data accuracy and have implemented rigorous data checks and audit processes. The 'NJ Smart Beta', a state-of-the-art platform, ensures error-free data usage, enabling us to back-test and analyse multiple portfolio combinations with just a few clicks.

As investors look for systematic ways to outperform traditional benchmarks, factor investing continues to bridge the gap between academic research and practical success.

Nirmay Choksi is the Director and Head of Investment of NJ Asset Management Private Limited. The views expressed above are his own.

Ask Value Research ![]()