AI-generated image

AI-generated image

If you're nearing retirement with an NPS (National Pension System) Tier 1 account, you now have more flexibility than ever to withdraw your savings. The recent introduction of systematic lump sum withdrawal (SLW) allows you to redeem up to 60 per cent of your corpus in tax-free phases rather than as a single lump sum.

This opens two options you can consider:

-

The first is to remain invested in the NPS and systematically withdraw money from there.

- The second is to move the retirement corpus to an equity savings fund and start a systematic withdrawal plan (SWP) . Equity savings funds are generally recommended for retirees due to their potential for balanced growth and regular income.

But before we dive into a head-to-head comparison between NPS Tier 1 and equity savings funds, here is what you should know about them.

NPS Tier 1 vs Equity savings funds: Key differences

| Feature | NPS Tier 1 with SLW | Equity savings fund with SWP |

|---|---|---|

| Management fees | Low expense ratio, a maximum of 0.09 per cent |

Higher expense ratio Category average: 0.64 per cent |

| Where they invest | Equity and debt | Equity, debt and arbitrage |

| How they invest |

Up to 75 per cent of the contributions can be invested in equity, of which, a major chunk is parked in large caps. The remaining contributions are spread across corporate debt (above 80% in AAA bonds) and government securities. |

Equity: 15-40 per cent Arbitrage: 25-50 per cent The remaining amount is invested in debt instruments |

| How they are taxed | Withdrawals are tax free |

If the units are redeemed within a year, a 20 per cent short-term capital gains tax is applicable. If the units are redeemed after a year, gains beyond Rs 1.25 lakh are taxed at 12.5 per cent |

NPS Tier 1 vs equity savings funds: Performance

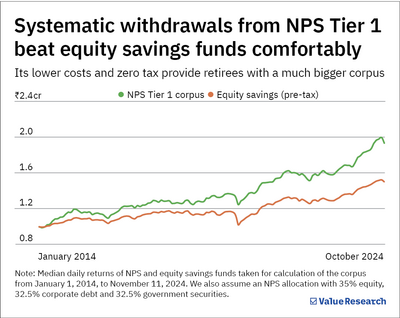

Now, let's check which option is more suitable. We looked at the actual performance data from the past 10 years. We assumed a corpus of Rs 1 crore and a monthly withdrawal of Rs 50,000 (equivalent to a 6 per cent annual withdrawal rate) over this period.

We found the NPS Tier 1 largely stayed ahead of equity savings funds in terms of overall corpus growth.

As seen in the graph below, if you remained in NPS Tier 1 and withdrew from it for 10 years, you would have nearly Rs 1.94 crore left in your account.

On the other hand, if you had taken out your money from NPS and invested the corpus in an equity savings fund, your corpus would be lower by Rs 44 lakh, that is, Rs 1.50 crore. And this is before taxation. Since NPS withdrawals are tax-free, and equity savings funds aren't, this gap would only be wider.

What's more, the NPS fares better despite taking a slightly lower risk.

NPS Tier 1's standard deviation (a metric to gauge an investment's volatility) is 5.35 per cent, while equity savings funds stand slightly higher at 5.4 per cent over a 10-year period, despite them investing in debt instruments with shorter maturities (around 4.22 years vs NPS's around 19 years in the case of government bonds and 7 years for corporate bonds, as of October 31, 2024). For the uninitiated, shorter-term debt securities are less prone to interest rate risks.

So, why does NPS Tier 1 have an edge over equity savings funds? It can be largely due to its lower management fees ( expense ratio ) and tax-free withdrawals. By contrast, equity savings funds face a tax burden of over Rs 1.3 lakh on withdrawals spread over 10 years.

However, it's not all doom and gloom for equity savings funds. They do have their merits.

NPS withdrawal rules: Good, but not perfect

A key drawback of systematic withdrawals from NPS Tier 1 is that you can redeem only a fixed amount every month. There's no provision for ramping up your withdrawals, either. And with inflation going through the roof almost every year, not being able to increase your withdrawal amount can be a handicap.

By contrast, SWPs from an equity savings fund have no such restrictions. You can increase the withdrawal amount and redeem it from your investment as and when needed, provided you cancel the existing SWP and start a new one.

Our verdict

While systematic withdrawals from both NPS Tier 1 and equity savings funds are ideal for retirees seeking steady income, the choice depends on various factors.

If you want the perks of low costs, zero tax and higher returns, stick to your NPS Tier 1 account.

On the other hand, an equity savings fund would be more suited if you want more flexibility and control over your withdrawal amount.

Also read: NPS Tier 2 vs hybrid funds: Which is more suitable for you?

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()