KLG Systel Ltd is Gurgaon — based knowledge company providing solutions to power, process, infrastructure and manufacturing companies.

KLG’s services include engineering and management solutions. The company has built significant Intellectual Properties (IP) that help reduce distribution losses for power distribution companies.

KLG has a country-wide network of 19 offices and serves 2000 clients, which include the top 500 Indian and Indian arms of Fortune 500 companies. The company derives 51 per cent of its revenues from power solutions and the remaining from the lifecycle solutions.

Investment Rationale

Dominant Power Solutions Business

KLG’s power solutions business is set to dominate its portfolio, accounting for an estimated 76.4 per cent of revenues (Rs 510 crore) by FY10E. The company has already booked orders worth Rs 175 crore for the FY2008-09 for the same. Furthermore, state electricity boards (SEB) are reeling under huge losses at the national level and KLG has a bouquet of products and services that will help address their problems like power thefts and insufficient billing and collection.

End-to-end Solutions

KLG Systel offers service and products that addresses all issues with its end-to-end business solutions that encompass survey, mapping and customer indexing in the first stage, installation of AMRs and data acquisition devices in the second stage and finally, revenue management and energy audit in the third stage.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

EPC Contracts to Drive Growth

KLG Systel bagged orders worth Rs 80 crore and Rs 60 crore last year from AVVNL Ajmer and JVVNL Jaipur, respectively. Moreover, the government is awarding contracts under the Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY) with a target to provide electricity for all by 2012. Currently, only 81 per cent of the villages in the country are electrified, posing a huge opportunity for players like KLG Systel. The company is continuing to see traction in this area and is expected to see a higher share of EPC contracts in the near term.

Lifecycle Solutions Business

KLG Systel has been in the lifecycle solutions space, since inception, providing software products from global vendors to the Indian industry. The company has established itself as a major player in this space accounting for 22 per cent of Autodesk’s sales in India and a significant portion for Invensys’ Wonderware. This segment is expected to benefit from the buoyant activity in the engineering and infrastructure sector in India.

Risks & Concerns

Loss of Major Principals

The company’s ability to maintain relationships and target new customers would have a bearing on revenues as well. KLG also depends heavily on its power solutions business and the inability to garner business from this sector would pose a downside risk.

Disappointing Quarterly Results

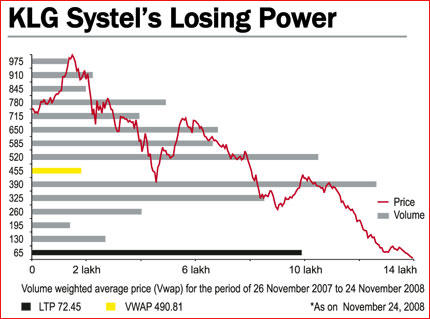

KLG’s net sales dropped drastically from triple digits to single digit in its Q2FY09 results. The company reported net sales of Rs 60.3 crore, a y-o-y growth of merely 5.6 per cent. The weak revenue growth in both of its business segments led to disappointing results. The company’s EBIT margins also crashed by 776 bps (y-o-y), while the net profit margins crashed by 760 bps (y-o-y) on the back of — very high operational costs, high depreciation charged on account of upcoming new facility and high interest cost on working capital loan of Rs 100 crore.

Drastically Revised Guidance

After the poor quarter, KLG has indicated a downward revision of its expected revenue for FY09E by 36 per cent. This has been attributed to the poor order booking in the lifecycle solutions business which is suffering from the current financial distress. The company is experiencing a liquidity crunch as well due to high debtors. This had led to the company taking working capital loans on its books with a high debt cost.

Government Contracts

A large portion of the company’s revenues would come from government contracts going forward. The company plans to gradually bring down the exposure to government contracts from 6.9 months as on FY07 to less than 5 months over time. However, inability to do so would leave the company strapped for cash and would require infusion through debt or equity.

Valuations

KLG currently has an order book of Rs 236 crore with less inflow from SG61 & Vidushi, which are the company’s most profitable propositions. The company has revised down its revenue expectation from the same segment by almost 49 per cent. Furthermore, on the back of the client specific issues confronted in the lifecycle solution space, KLG has revised down its annual revenue estimation for FY09E by almost 27 per cent. On the profitability front, the company is not expected to grow. All these factors will make the company perform badly in the current fiscal.

The stock has corrected to great extent and is trading at 3.4x its EPS estimate of FY09E of Rs 30.3 .On the back of poor visibility of revenue for the current financial year and steep downward revision of guidance by management, the company is valued at 4.1x its EPS for FY09E, which gives a target price of Rs 123.

Source: ICICI Direct

This article was originally published on December 15, 2008.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()