Recently Viewed

Clear All

Powered by

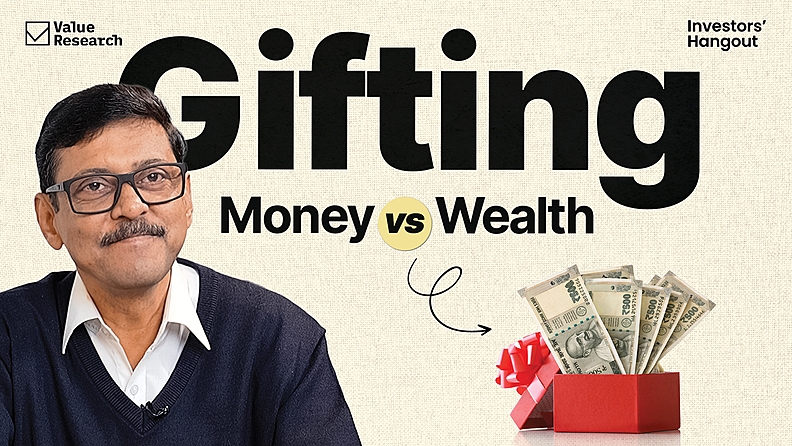

Investors' Hangout | By Dhirendra Kumar | 09-Jan-2026

How to Gift Mutual Funds Today

A simple rule change may have quietly turned gifting mutual funds into a long-term wealth decision. To decode what this means for you, watch this Investors' Hangout.

Mutual funds were always legally giftable, but the process was so complicated that almost nobody did it. The fundamental change is that you no longer need to convert your Statement of Account (SOA) units to demat form to transfer them. SEBI has enabled direct transfers through the registrar records held by CAMS and KFintech, operationalized via MF Central.

As Dhirendra Kumar explains, "The real problem was that if most people buy mutual fund by investing in a mutual fund and getting account statement of account... to gift you had to necessarily dematerialize it. Now it has become possible, SEBI has enabled it that in the records of the registars... the investor can authorize to be his assets to be gifted to somebody and that can be taken care of through a very usual machinery."

This isn't a minor procedural tweak–it's a behavioral shift. Kumar compares it to UPI: "Think of UPI transferring money to somebody was a always a legal thing... But the way it becomes the ease of doing it you go and buy a vegetable and you are able to pay 20 rupees through UPI that makes it mainstream." The same mainstreaming will happen with mutual fund gifting because the friction has been removed.

How Do I Actually Gift Units from an SOA Account? Step-by-Step Process

The process is now digital and straightforward through MF Central:

- Login to MF Central using your credentials

- Select the funds and units you want to gift

- Provide recipient details including their PAN, folio number (if they have one), email, and mobile

- Specify the reason for the transfer

- Complete OTP verification on both sides

- Pay stamp duty of 0.015% on the transfer value

- Units transfer within 2 working days

According to Kumar, "all you have to do is go to MS Central login specify the funds and the units which you want to give to somebody. tell the reason and after that uh all you have to do is that person may have a folio may not have a folio depending on that if he has a folio then it'll be transferred to him seamlessly if it is not then the new folio will be created."

The recipient doesn't need an existing folio–one can be created instantly. There's also a 10-day lock-in period after transfer during which the recipient cannot sell the units.

What Tax Implications Should the Recipient Know About?

This is critical: The giver pays no capital gains tax at the time of gifting. The tax liability passes to the recipient, but with important conditions:

- Cost basis carries over: The recipient's cost of acquisition is the original purchase price, not the value at gift date

- Holding period carries over: The holding period is calculated from the original purchase date, not the gift date

- Tax triggered only on sale: The recipient pays capital gains tax only when they eventually sell the units

Kumar clarifies: "recipient will be liable for the capital gains because the date of purchase of the investment and since then whatever is the capital gains paying that capital gains tax went as and when since... the cost of acquisition remains the original."

For example, if you bought units in January 2024, gift them in November 2025, and the recipient sells in December 2025, the total holding period is nearly two years–qualifying for long-term capital gains taxation based on the original purchase date.

Key Takeaways:

- Zero tax impact for the donor at transfer time

- Recipient inherits original cost basis and purchase date

- Tax efficiency depends on recipient's income slab when they sell

- Clubbing provisions apply if gifting to spouse or minor child (gains clubbed with donor's income)

Is Gifting Mutual Funds Better Than Giving Cash? Practical Use Cases

Yes, for specific goals. The video emphasizes two scenarios:

- Special occasions: Instead of cash for weddings or birthdays, gift already-invested units that continue growing

- Wealth transfer with purpose: Ensure the money remains productive rather than being spent

Kumar explains the difference: "When you give cash to somebody, it is up to him to put it to work. But if your desire is that this investment should be done and it should remain productive for as long as that person wants to, you are effectively... instead of giving cash, you are giving a productive financial asset which keeps working."

This approach combines financial value with long-term impact. The giver maintains control over the form of the gift–whether consumption (physical item), freedom (cash), or productive asset (mutual fund units). For financial goals, the productive asset approach can be more inspiring and purposeful.

Important caveat: The 10-day lock-in means recipients can't immediately liquidate, so plan accordingly for genuine gifting scenarios, not emergency funds.

Other Videos

Why Gold Failed Its Biggest Test

03-Apr-2026 · 13,946 Views

3 Things to Do Before April 1

27-Mar-2026 · 51,744 Views

SEBI's New Rules: What They Mean For You

20-Mar-2026 · 45,986 Views

War, Wealth & What To Do

13-Mar-2026 · 30,169 Views

Women & Wealth: Why Earning Isn't Enough

06-Mar-2026 · 10,233 Views

Multi-Asset or Aggressive Hybrid: Which One Fits You?

27-Feb-2026 · 17,759 Views

SWP & Bucket Strategy for Retirement

20-Feb-2026 · 36,742 Views

NPS Changes 2026: Annuity Escape & Tax Benefits

13-Feb-2026 · 21,125 Views

CAGR vs XIRR vs Rolling Returns: Which Matters?

06-Feb-2026 · 21,819 Views

Union Budget 2026: Investor Checklist

01-Feb-2026 · 15,298 Views

Is ₹5 crore enough for your retirement?

23-Jan-2026 · 29,591 Views

Your first ₹1 Crore Plan

16-Jan-2026 · 62,699 Views

The Only Mutual Fund Advice That Matters in 2026

02-Jan-2026 · 69,990 Views

Outliers, Laggards & the Cost of Chasing Past Performance

26-Dec-2025 · 28,125 Views

Best Mutual Funds for Senior Citizens (3-5 Year Goals)

19-Dec-2025 · 59,136 Views

Your Fund Isn't Performing. Should You Switch?

12-Dec-2025 · 34,112 Views