In what has become a norm in recent years, the name Adani is on the headlines again. Adani Enterprises has come out with one of the biggest and costliest FPOs ever and plans to raise Rs 20,000 crore.

While we have already covered how we feel about the FPO's valuations in our previous story, here are five things you must know before subscribing to the Adani FPO.

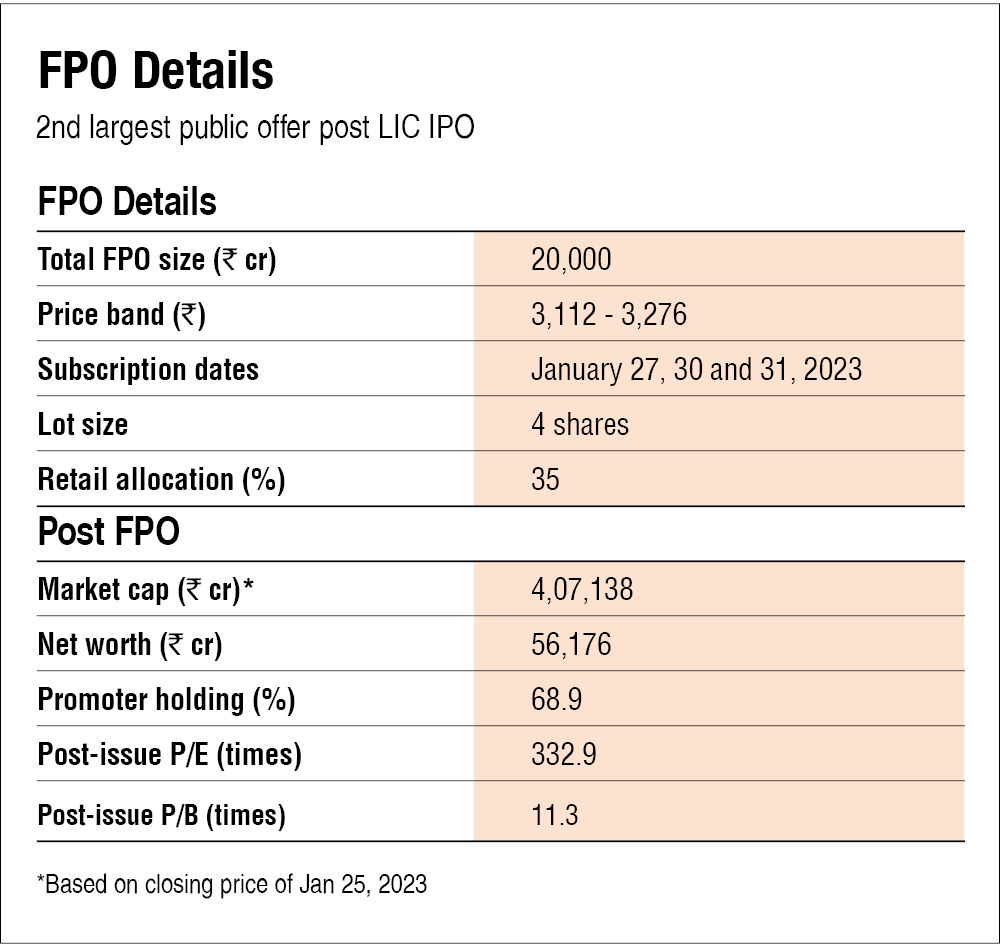

1. Price band

On January 25, 2023, the share price closed at Rs 3,405. The upper price of the band at Rs 3,276 is at a 3.9 per cent discount to the closing price.

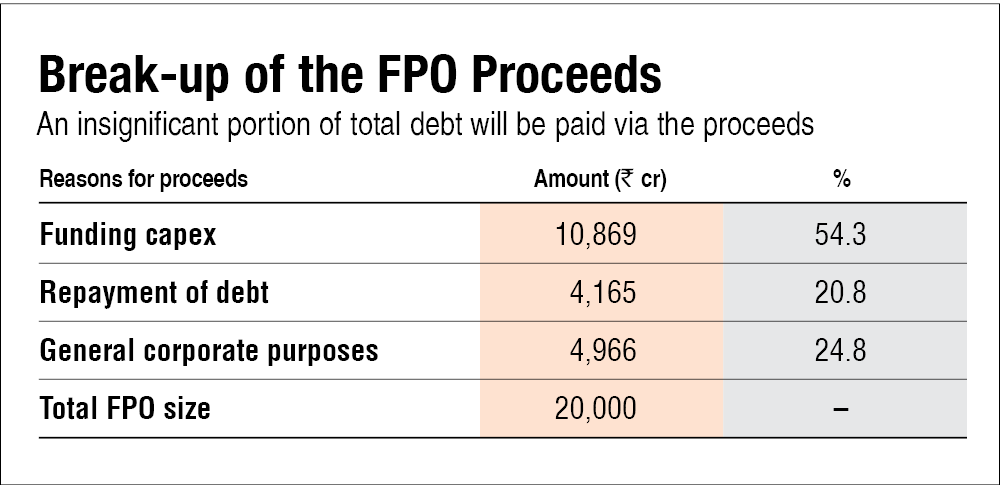

2. The proceeds will be used for capex and debt repayments

54.3 per cent of the total FPO proceeds will be used for the company's and its subsidiaries' capital expenditure requirements. These include the company's green hydrogen ecosystem, improving certain existing airport facilities and construction of the greenfield expressway.

20.8 per cent of the proceeds will go towards debt repayments of the company and three of its subsidiaries, Adani Airport Holding, Adani Road Transport and Mundra Solar. As of September 2022, the company had Rs 40,023 crores of debt on its books. It will use the proceeds to pay back 10.4 per cent of the total debt.

The rest of the proceeds will be held for general corporate purposes.

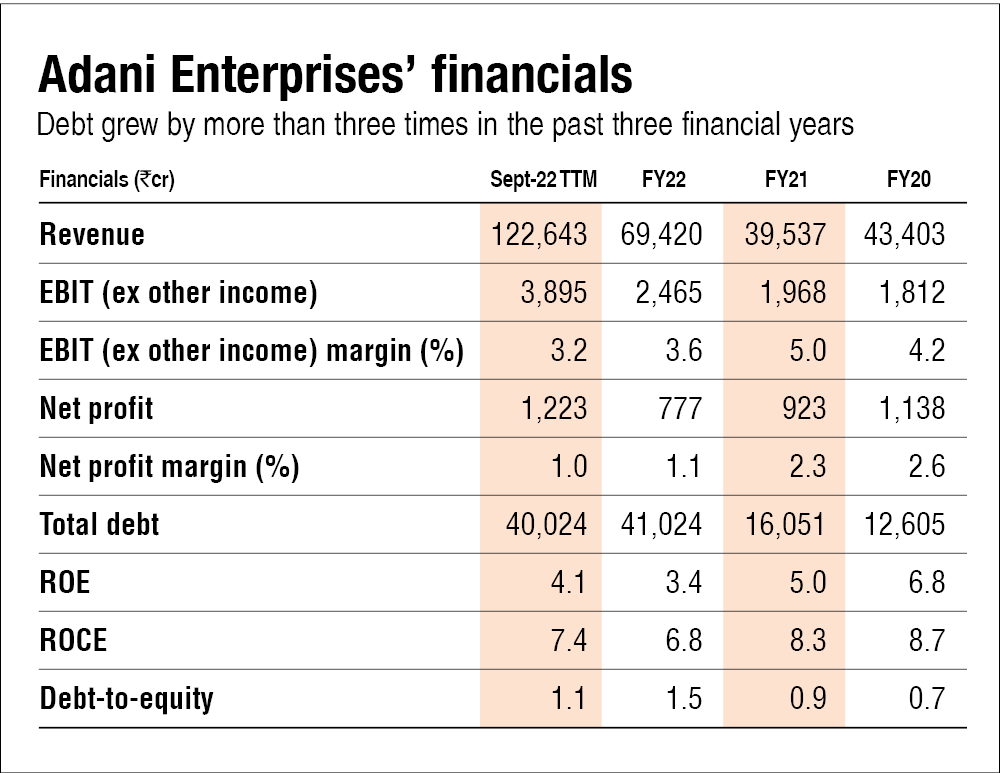

3. Flimsy fundamentals

While the company's topline growth has been healthy, its profitability has been on a downward trajectory since FY20. The company's ROE is at a meagre 4.1 per cent on a trailing twelve-months (TTM) basis (as of September 2022).

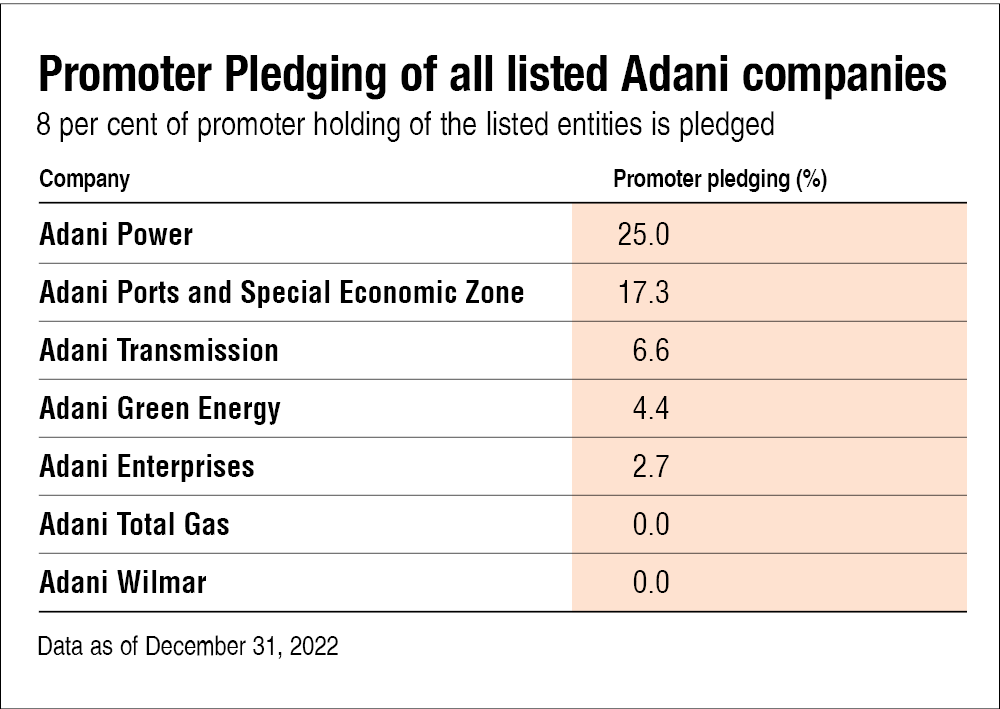

4. Pledging of shares

As mentioned above, the company has significant debt on its books, and promoters' stake has been pledged to take loans. If the promoters default, their stakes will be sold by the lender to recover the loans.

As of December 31, 2022, five out of the seven listed Adani companies have their promoters' stake pledged. Adani Power has pledged 25.0 per cent of its promoters' stake, whereas the flagship company, Adani Enterprises, has pledged a 2.7 per cent stake.

5. Sky-high valuations

As we have mentioned in our previous article, the company's inflated valuation makes us highly uncomfortable. Post-FPO, the stock will have a P/E of around 333 times (versus current P/E of 316 times, as of January 25, 2023), which is 10 times more than its five-year median P/E of 32 times and 14 times more than its 10 year median P/E of 24 times.

To justify such valuations, the company would have to grow at an unprecedented rate, never seen before in the Indian markets.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()