An unsatisfactory life insurance policy is like an unhappy marriage.

We often enter such alliances without knowing what to expect. Perhaps we made a hasty decision or were promised the moon by our relatives or friends...Whatever may be the case, you should be glad you aren't alone.

Such regret is commonplace, especially when it comes to life insurance policies because we understand so little about them.

But we are not here to depress you. Instead, we want to inform you that a life insurance policy's divorce process is relatively straightforward, satisfying and not very messy.

So, let's huddle together to know how you can walk away from this unhappy union.

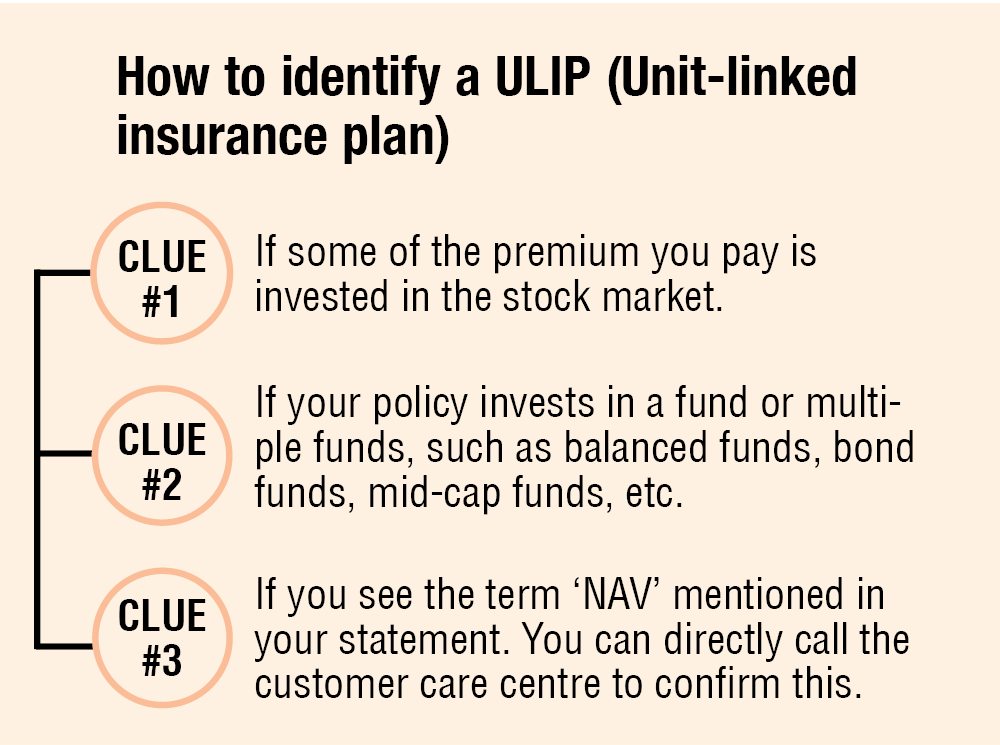

Understanding the type of life insurance policy you have

Before we get into the step-by-step process of how to surrender life insurance policy, it is very important to understand what kind of life insurance policy you have. (That's because different policies have different exit steps).

What we recommend

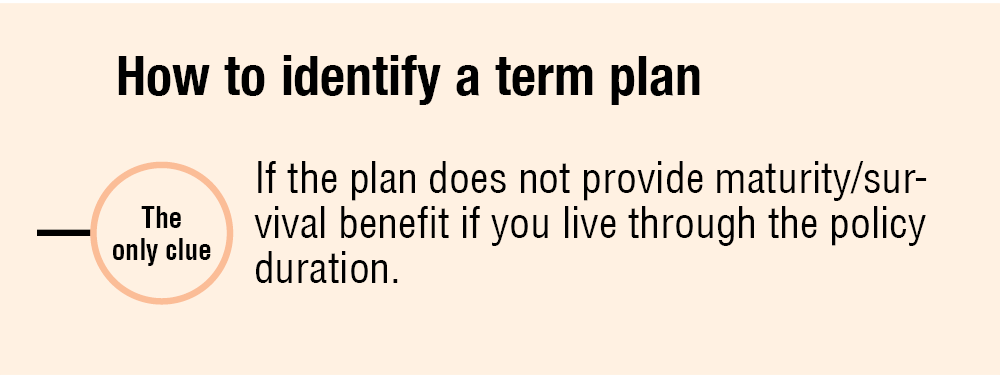

Of the three types of life insurance policies, term plans are the BEST! If you have a term plan, stick with it.

But please note there are a few term plans that promise to return the premium amount at the end of the policy. However, such plans are usually expensive and should be avoided.

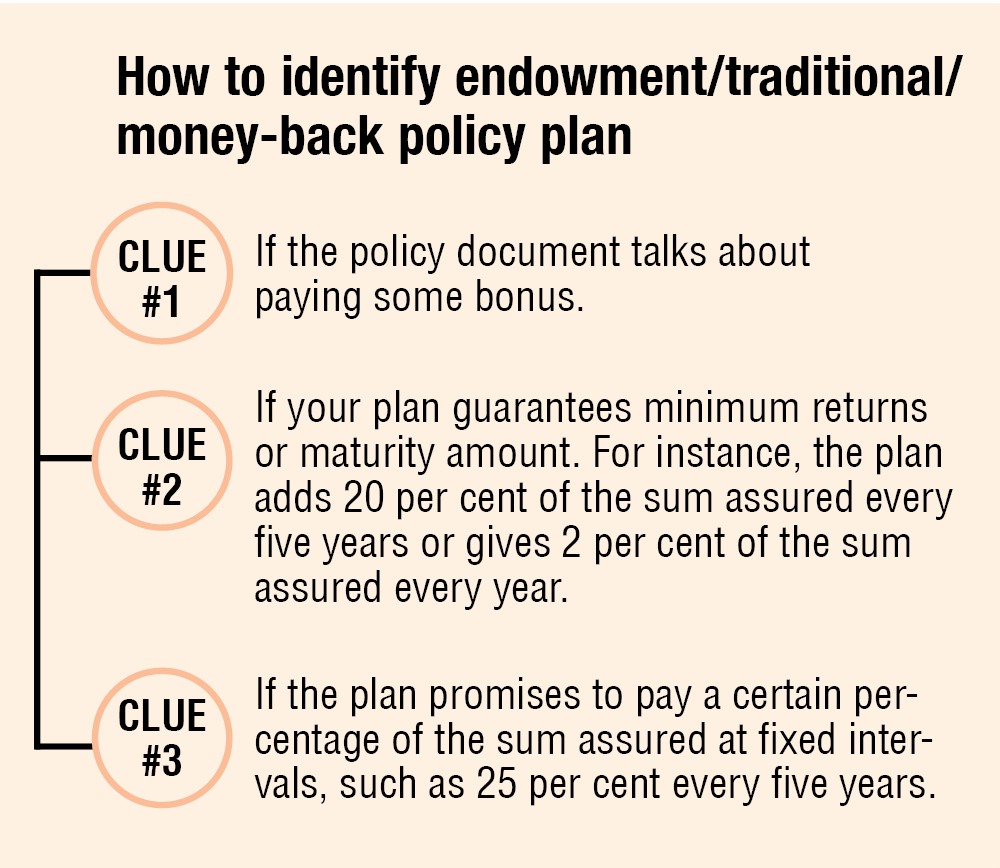

But if you have a ULIP or an endowment/traditional/money-back policy plan and want to discontinue your relationship, here's what you need to do.

In this article, we will focus on how to exit your ULIP. Please visit this page for those with an endowment/traditional/money-back policy plan.

Surrendering process of ULIPs

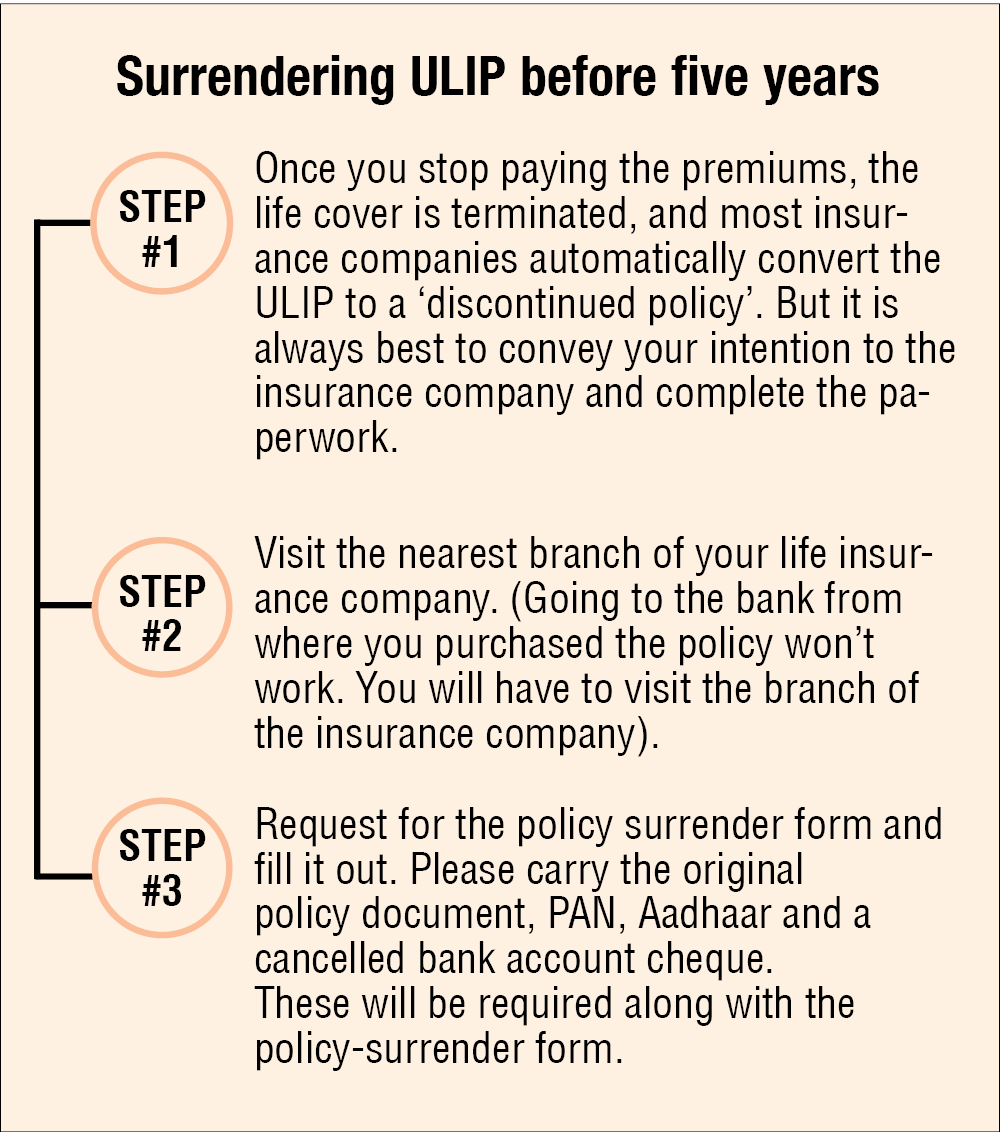

ULIPs come with a mandatory lock-in period of five years; no matter what, you can only get the money you have already invested/paid as a premium after completing the five years.

That said, it doesn't mean you must continue paying the premium for the entire five-year period. In fact, it can be stopped anytime.

Things to keep in mind

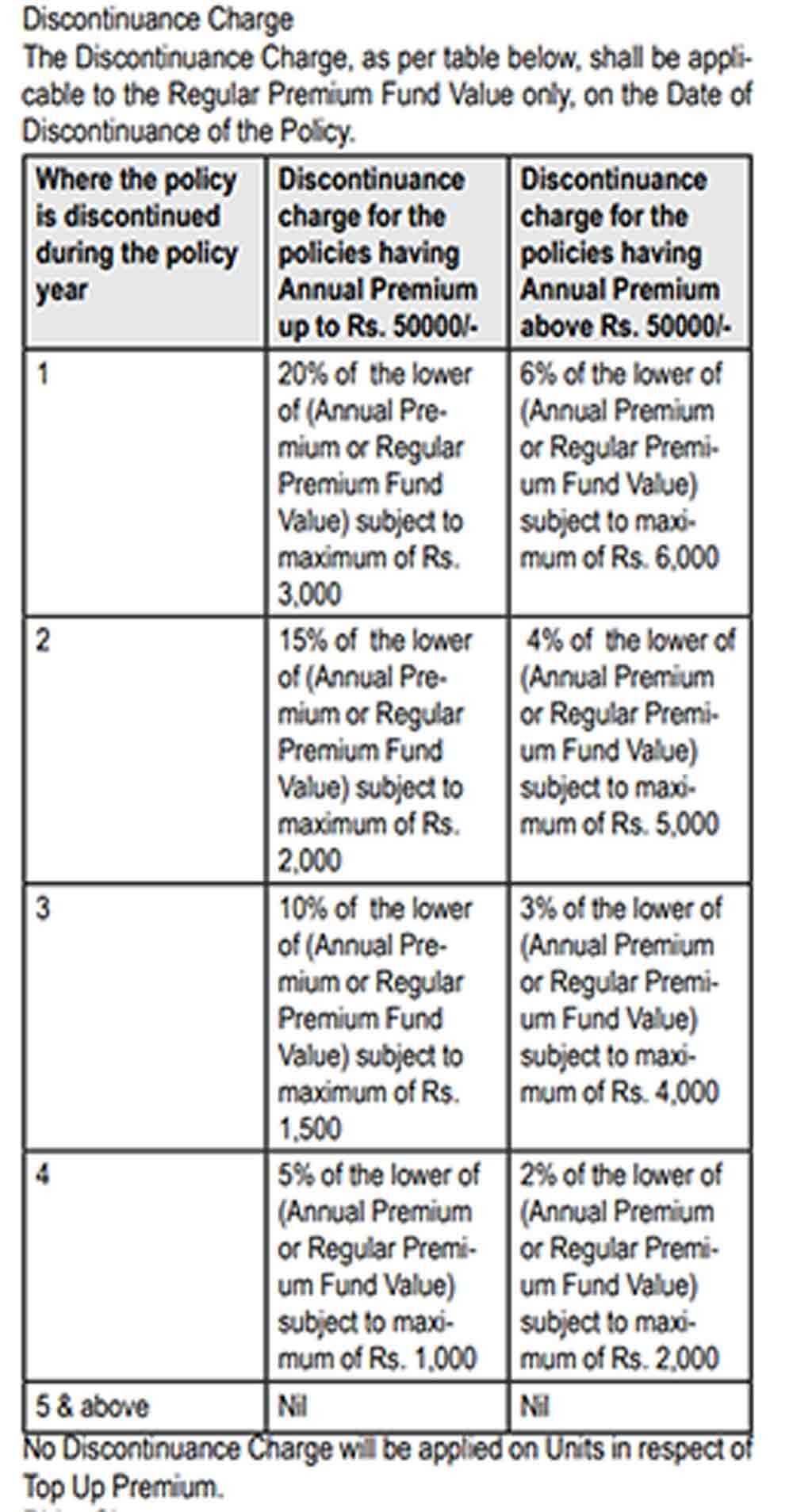

- The insurance company will deduct certain charges (discontinuance charges) from the market value of your investment.

The amount mentioned in the policy document varies from policy to policy. It is usually high in the initial five years. - The remaining money is transferred to a 'discontinued policy fund' where it continues to earn an interest of about 4 per cent every year, until the lock-in period is complete. After that, the proceeds are transferred to your bank account.

- During this period, insurance companies generally continue to deduct a charge of 0.50 per cent.

Surrendering after the lock-in period of five years

The procedure remains the same (as mentioned in the above process). The only difference is that instead of transferring your money to the 'discontinued policy fund', the insurance company will directly pay the proceeds to you after deducting discontinuance charges.

Just to give you a real example, this is how discontinuance charges look for a ULIP by Bajaj Allianz - Future Gain.

Suggested read: Surrendering a ULIP in the lock-in period

This article was originally published on December 21, 2022.

Ask Value Research ![]()