Expense ratio is the fee you need to pay mutual fund companies to manage your money.

Just like you pay a lawyer to manage your legal matters, a chartered accountant to help you file your tax returns and an architect to build your house, mutual fund managers charge a fee for building and managing your investment.

In the world of mutual funds, this fee is known as 'expense ratio'.

Expense ratio includes all the charges that you need to pay a fund house. These charges include:

- Fund management fees

- Agent commission

- Selling and promotional expenses, among others

Should you care about expense ratios?

An expense ratio of even 1.5 per cent can significantly eat into your returns in the long run. Here's how: say you invested Rs 1 lakh for 10 years in a mutual fund that grew at 15 per cent. Your investment value would be about Rs 4 lakh. But if we include the 1.5 per cent expense ratio, your returns would reduce to Rs 3.5 lakh, nearly 13 per cent less than what it would have been without any expenses.

Therefore, it's better for you to choose a consistently top-performing mutual fund that has a low expense ratio.

How to find a fund's expense ratio?

Different funds have different expense ratios. But do note the expense ratio of equity mutual funds can't exceed 2.25 per cent, while it can't be more than 2 per cent in debt funds. This fee is charged irrespective of the fund's performance, be it positive or negative.

To find out the expense ratio of a fund, you can check its disclosures on the website of the given asset management company (AMC). Or you can easily access the same on the respective fund's page on the Value Research website by using the search bar at the top.

What's the best way to reduce expense ratio?

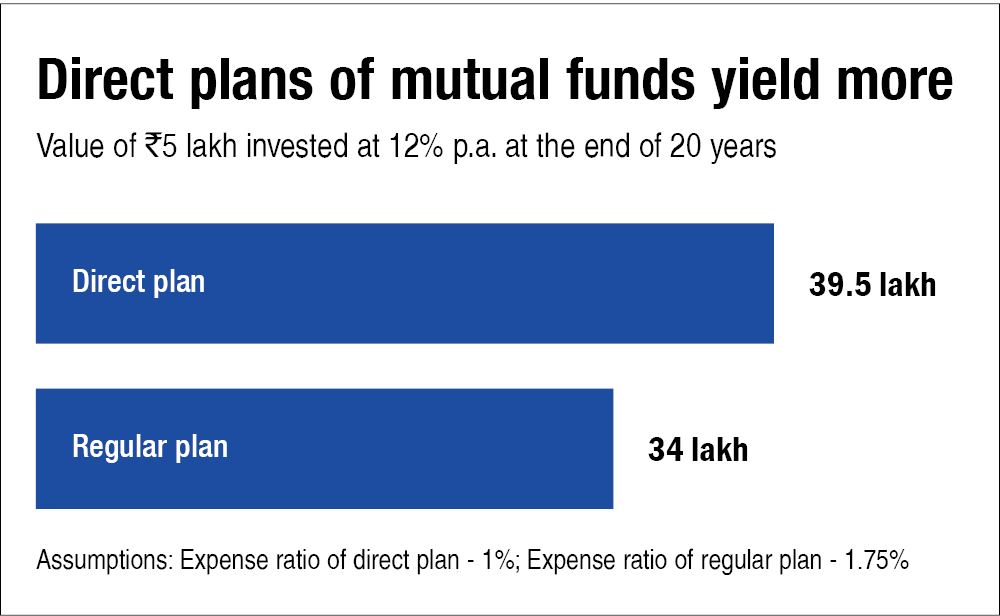

When you are looking to invest in a mutual fund, you'd notice there are two versions of the same mutual fund. One would have 'regular' mentioned in the name, while the other one would have 'direct' written there.

'Regular' mutual funds have a higher expense ratio than 'direct' funds because it includes distributor commissions. Even though it may not look substantial in percentage terms, the impact on the overall corpus becomes meaningful over a period of time as you can see in the graph below.

Therefore, if you are capable of managing your own investments, you may significantly lower your expense ratio and receive higher returns over time by sticking to direct plans.

To sum up, you should check the expense ratio before investing your hard-earned money in a mutual fund. But bear in mind that a lower expense ratio does not necessarily make the fund better. A fund that delivers good returns with minimal expenses is the way to go.

This article was originally published on May 24, 2022, and last updated on October 13, 2022.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()