Raman (33) has received an exciting offer to work for a big company abroad and will be relocating next month. He plans to return to India someday but doesn't see that happening for at least the next five to seven years. He has a few lakhs invested across several mutual fund schemes in India and wants to continue with his SIPs. But he's not sure if he can do so upon becoming a Non-resident Indian (NRI) or if there are any formalities that he needs to complete to ensure continuity.

Sounds relatable? Well, Indians moving abroad is a pretty common phenomenon. But what do they need to do with their investments in domestic mutual fund schemes? Read on as we answer the common questions Raman and others in a similar situation have.

Can NRIs continue with their investments in Indian mutual funds?

Yes. There is no restriction on NRIs investing in Indian mutual fund schemes.

Are there any formalities you need to complete on becoming an NRI?

Yes, you must update your residential status and your bank account details. Here's what you need to do:

- Change your residential status

As a first step, the investor must get his residency status updated in the KYC (Know Your Customer) records from a 'resident' to a 'non-resident'. The NRI needs to visit the investor service centre of any one of the fund houses with which he holds the investment. KYC records are centralised, and a change with one fund house would reflect across all mutual fund investments. However, he needs to be physically present. This updation cannot be done online. Alternatively, one may seek the help of an intermediary to get the KYC records updated instead of visiting himself.

The process involves filling and submitting a form for change in KYC status along with copies of PAN card, passport and proof of local and foreign addresses. A utility bill, rent agreement or house ownership papers in the country of NRI's residence should be accepted as the foreign address proof by most fund houses.

But note that the change can be done only after you have become an NRI, i.e., after you have spent at least 183 days residing outside India during the financial year. This means that you cannot complete this formality before leaving India. But as an alternate, you may explore the possibility of completing the paperwork and leaving them with an intermediary to submit them on your behalf later.

- Convert your bank account to an NRE or NRO account

Many individuals continue with their regular savings bank account in India even after becoming an NRI, but it violates law under the Foreign Exchange and Management Act (FEMA). Further, fund houses are not allowed to accept investments in foreign currency. So, it becomes necessary to convert your bank account into a Non-Resident External (NRE) or Non-Resident Ordinary (NRO) account.

A Non-Resident External account is where you can deposit your foreign earnings. In contrast, in the case of a Non-Resident Ordinary account, you can only deposit the income earned in India. Moreover, money held in a Non-Resident External account can be freely remitted to the country of your residence. This facility is not available in the case of a Non-Resident Ordinary account. Therefore, if you want to use your foreign earnings for investing in Indian funds, opt for the Non-Resident External account.

To convert your bank account, you will need to furnish your foreign address proof, a copy of PAN, and proof of you being an NRI, such as your work permit or the visa stamps on your passport.

After conversion, update the same with the fund houses where you have investments, and this needs to be done individually with each of them. Going forward, this is going to be the bank account for all the debits and credits of your investment and redemption amounts.

- Additional requirements for those relocating to the US or Canada

There are additional compliance requirements for citizens or NRIs based out of the US or Canada under the Foreign Account Tax Compliance Act (FATCA) provisions. Some fund houses do not accept investments from such individuals to avoid the hassle. While such fund houses won't accept fresh inflows from you, there aren't any implications on your existing investments, and you can continue to hold them. But if your fund house does accept investment from NRIs based in the US or Canada, it is likely to get an additional FATCA declaration form filled from you.

- Preferably shift to online modes of transactions

If you've been investing offline so far, it's better to switch to an online platform for convenience in transacting from a remote location.

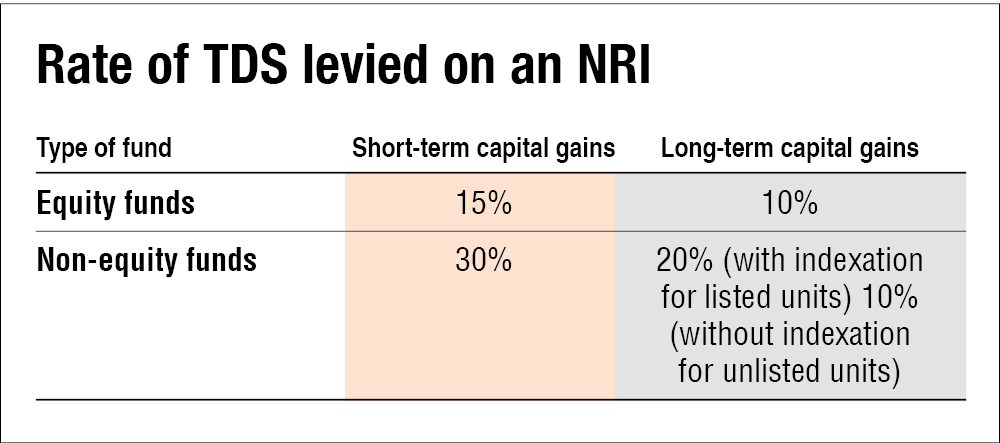

What are the tax implications on an NRI's fund investments in India?

There is no change in the tax incidence, but you will now be subjected to Tax Deducted at Source (TDS) on redemption. The fund house would deduct a portion of your redemption proceeds as TDS at the following rates:

Would you end up paying double tax - in India as well as your country of residence?

India has a Double Taxation Avoidance Agreement (DTAA) with more than 90 countries worldwide. If you reside in one of them, you will get at least a partial relief from double tax. But you should seek more clarity on the tax incidence vis-à-vis your country of residence from a tax expert.

Are there any implications on the nominations on your investments?

No. Your nominations can continue as before.

Also read: Mutual fund investments for NRIs

This article was originally published on March 23, 2022, and last updated on January 04, 2023.

Ask Value Research ![]()