Health insurance works as a financial-protection tool against medical expenses. It usually provides either direct payment or reimbursement for the expenses associated with illness, injuries and hospitalisation, as detailed in the scope of the policy cover.

The cost and range of protection provided by a health insurance policy depend on the insurer and the type of policy purchased by the policyholder. Some policies also cover pre- and post-hospitalisation expenses.

ASPECTS OF HEALTH INSURANCE

Features of health insurance

- Eligibility: Any adult can buy health insurance; children can also be covered under the policy.

- Entry age: From 18 up to 65 in most cases. Policies for senior citizens can be taken from the age of 60. Policies for children are also available, with the entry age being three months. Dependent children can be added to the policies taken by parents.

- Maximum age till which cover is offered: Typically 85 years. Some policies offer lifetime coverage.

- Policy tenure: Most policies are annual-renewal policies. Some insurers provide policies with a tenure of up to three years.

- Premium: Depends on the insured person's age and health condition. Depends on the policy type and sum assured.

- Sum assured: Depends on the policy type. Depends on the policy tenure.

- Other aspects: Premium frequency is annual. In some cases, it can be two or three yearly. There is also a grace period in premium payment. However, no risk is covered during the grace period.

- Policy holding: Individual, family and group.

- Nomination: Not available.

Capital protection and inflation protection

The sum assured in a health-insurance policy is guaranteed as per the terms of the policy as long as the premiums are paid regularly and the policy is in force. Health insurance is not inflation protected, which means whenever insurance needs to increase or the cost of healthcare goes up, one needs to buy an additional cover. Some policies do provide the facility of adding to the cover with time, which can address inflation at an additional cost.

Guarantees

The sum assured is guaranteed. However, the premium is not fixed and increases with the age of the insured. This is because of the increased risk.

Portability

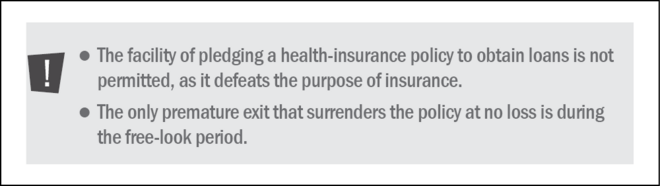

Health-insurance policies are portable, which means that one can move from one insurer to another by transferring one's existing policies to a new insurer. Portability also enables the transfer of the credit gained by the policyholder for pre-existing conditions if the policyholder chooses to switch from one insurer to another or from one plan to another plan of the same insurer, provided the previous policy has been maintained without any break.

- A policy can be ported only at the time of renewal.

- Apart from the waiting-period credit, all other terms of the new policy, including the premium, are at the discretion of the new insurance company.

- At least 45 days before renewal, you need to inform your existing company about the switch and the company you want to switch to. You must renew your policy without a break (there is a 30-day grace period if porting is under process)

Other risks

Premium rates may go up or down on renewal. The scope of policy cover can also change depending on the insurer, since health insurance is typically an annual contract.

Health insurance tax benefits

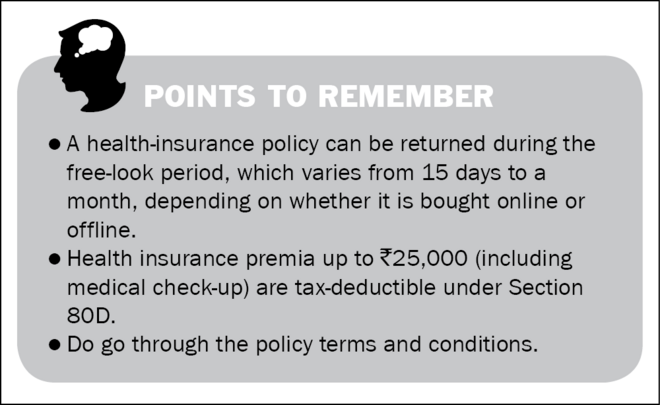

The premiums paid towards health insurance are tax deductible under Section 80D of the Income Tax Act.

- Premium up to Rs 25,000 for the assessee (including spouse and dependent children).

- Additional deduction up to Rs 25,000 on the premium paid for parents.

- For senior citizens, premiums are deductible up to enhanced limit of Rs 50,000.

Above limits also include a maximum payment of Rs 5,000 (for assessee, spouse, parents and dependant children) for a preventive health check-up.

Where to buy health insurance

A health-insurance policy can be bought from individual health insurance agents, banks, insurance brokers or on the internet.

How to buy health insurance

Once you have evaluated the amount of insurance you need and found the insurer offering the policy, you will need to fill the proposal form provided by the insurer. Further,

- You will need documents to prove your date of birth, identity proof, such as a copy of driving licence or voter's card. Alternatively, Aadhaar card can be used for this purpose, which is now mandatory.

- You may have to undergo medical tests depending on your age or the cover that you are seeking.

Types of health insurance

- Death: Lump-sum payment in the case of death due to accident.

- Permanent total disability: Lump-sum payment in the case of loss of limbs, resulting in permanent total disability.

- Permanent partial disability: Lump-sum payment in the case of permanent partial disability; for instance, partial vision or hearing loss.

- Temporary disability: Lump-sum payment in the case of a temporary disability arising from an accident; for instance, a fractured leg.

- Individual health plan: These are traditional healthcare plans modelled on the old mediclaim-type policies offered by insurers. Typically, the benefits include room and other hospital services, such as X-ray, lab expenses and operating-room use. The cover extends to pre- and post-hospitalisation expenses on medication and diagnostics, subject to limits and conditions in the policy.

- Family-floater plans: An extension of the individual plan, these cover a family by spreading risk across the members. For instance, a Rs 2 lakh cover is spread across four family members: two adults and two children.

- Arogya Sanjeevani plans: IRDAI has mandated all insurance companies to provide these plans from April 2020. It is a simple and affordable health-insurance product with basic features that cover healthcare expenses up to Rs 5 lakh. This coverage includes pre- and post-hospitalisation expenses, hospital room rent, ICU services etc. They are available in both individual and family floater alternatives.

- Senior-citizen health plans: Entry after the age of 60 but offer lower cover and more stringent terms and conditions.

- Group health plans: For employees in organisations; these come with certain benefits tailored specifically to fit the needs of the group.

- Hospitalisation-cash plans: Pay a fixed sum for each day spent in the hospital; they are totally independent of the room rental and treatment costs.

- Critical-illness plans: Cover a host of high-cost, low-incidence critical-health conditions, such as heart attack, cancer, stroke or kidney failure

- Life-insurance plans with riders (accident benefit, critical illness, hospital cash, waiver of premium, etc.): Riders are add-ons to the basic insurance policy to supplement the insurance cover. These are defined-benefit plans with fixed payouts and may not compensate in full for the cause.

Exclusions in health-insurance policies

Here are a few common exclusions in most health insurance policies.

- No-claim/waiting period on pre-existing diseases: Diseases that have been in existence before the policy commencement are not covered, even if you were unaware of their existence. Some companies now relax this requirement by covering them after the passage of two-four years from the commencement of the policy. Some do so after four no-claim years on a policy.

- Cool-off period: This is the period when claims are not paid on the medical expenses incurred on the treatment of any health-related condition occurring within 30 days of the policy coming into force (except through bodily injuries due to accidents). Also, in some cases, such as in cataract surgery, there are sub-limits on reimbursement even after the cool-off period.

- Eye-related expenses: Expenses on the laser treatment of eyesight and costs of spectacles or contact lenses are not usually covered.

- Dental and cosmetic surgeries: Expenses incurred on dental treatment or cosmetic surgery are typically excluded.

- War injuries: Injuries due to wars and invasions or any claim directly or indirectly caused or contributed by nuclear weapons are not covered.

- Smoker's premium: Some insurers have a higher premium for smokers. If you were a smoker in the past, you must have a five-year period of abstinence to be termed a non-smoker.

- Others: Treatment through non-allopathic methods, such as Ayurveda or Unani medicine, is not compensated.

There are also provisions that curb the facilities you can avail of during hospitalisation. Insurers restrict certain discretionary costs associated with hospitalisation by introducing sub-limits for reimbursement in the manner shown below.

- Room rent: 1.5 per cent of the sum insured per day. If your insurance cover is Rs 2 lakh, room rent will be capped at Rs 3,000 per day.

- ICU charges: 3 per cent of the sum insured per day.

- Doctor's fees: 40 per cent of the sum insured.

Also read:

How to buy the right health cover?

Should I buy health insurance now or when I retire?

How to create a healthcare corpus?

This article was originally published on December 13, 2021, and last updated on October 13, 2022.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()