Incorporated in 2004, Clean Science and Technology (CST) is a speciality-chemical player dealing in niche chemical compounds. Unlike other chemical players, it develops and uses eco-friendly chemistries based on catalytic technology.

Its products are used as polymerisation inhibitors, intermediates for agrochemicals and pharmaceuticals, anti-oxidants, UV blockers, anti-retroviral reagents and others. Although CST focuses on niche products, it is the largest producer of primary products, including MEHQ, BHA and others. The company exports its products to various regulated markets, such as China, Europe and the US. Exports account for 70 per cent of the company's total revenue.

The Indian speciality-chemicals industry is expected to grow to $147 bn from $78 bn in 2019, owing to factors like the introduction of stringent environmental norms in China, the availability of cheap labour and the R&D skillset in India, the Indian government's export push, amongst others. To capitalise on the opportunity, CST is augmenting its current production capacity of 29,900 MT, which will be funded internally. The company also plans to introduce new products with varied applications across industries.

Strengths

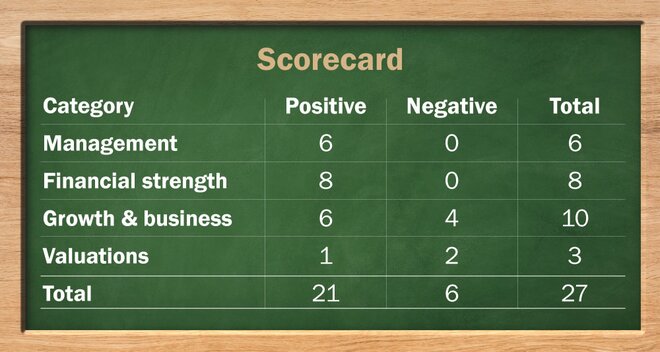

- Over the last few years, the company has successfully backward-integrated its processes. This had led to margin improvement (the EBITDA margin of 55.5 per cent in FY21 as compared to 37.5 per cent in FY19).

- For many of its products such as MEHQ, BHA and others, the company is either the largest or one of the leading manufacturers in the world. It enables the company to compete effectively against both existing and new entrants.

- The company has developed clean chemistries based on catalytic processes. Therefore, most of its current production processes release either zero liquid or only water as the discharge.

- In speciality chemicals, the entire process right from product ideation to commercialisation takes two-three years and companies need to work closely with their customers. Hence, it leads to higher switching costs for customers.

Risks/weaknesses

- MEHQ contributes 46-48 per cent to the company's top line, leading to a high product concentration.

- R&D expense, accounting for around 0.1-0.2 per cent of the company's total revenue, is lower than that of industry-leading players (PI Industries: 3-4 per cent). Further, owing to the absence of any patents or contracts with global innovators, the company does not have any enduring competitive advantage.

- Customer-concentration risk poses a threat to the company, as in FY21, the top 10 and topmost customers contributed 47.9 per cent and 13.3 per cent, respectively, to the top line.

- The company's primary raw material phenol (44 per cent of the costs of raw materials) is prone to crude-oil price fluctuations.

- The top three promoter-cum-management personnel (including the MD) are each paid around 4 per cent of the profits as the performance bonus, which is quite high as compared to other publicly listed companies.

IPO questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

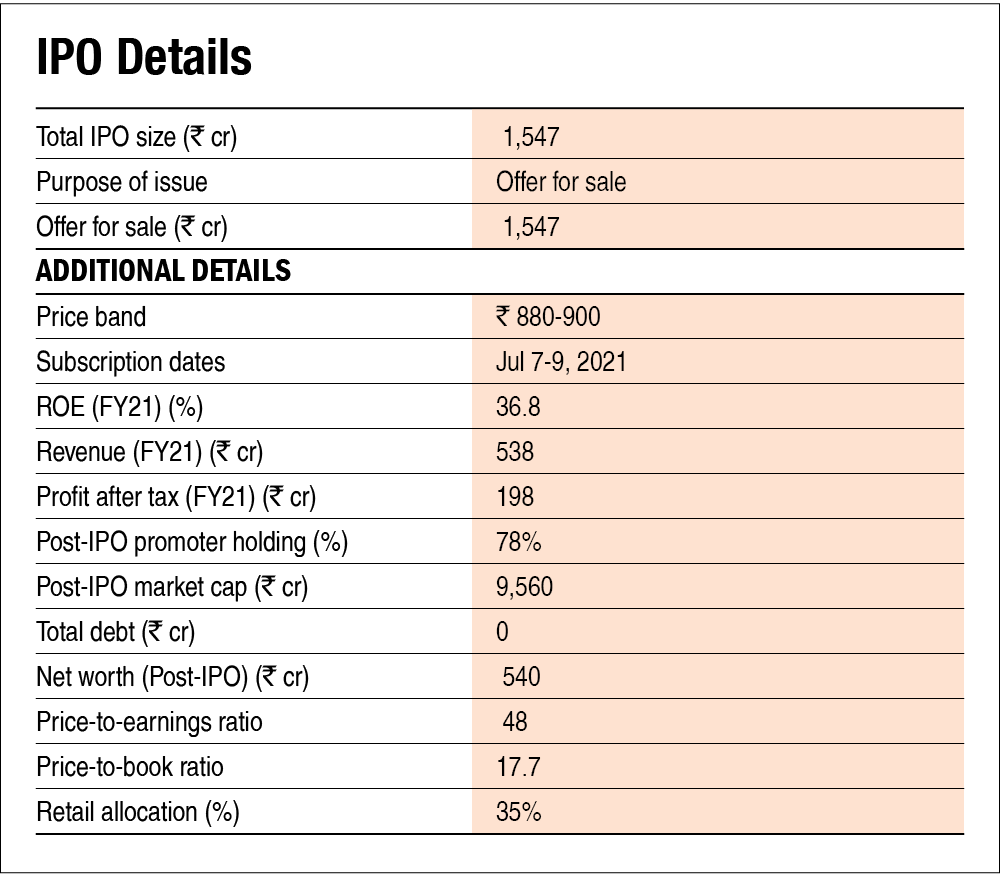

Yes, the company reported a PBT of Rs 267 crore for FY21.

2. Will the company be able to scale up its business?

Yes. The company manufactures niche-yet-critical speciality chemicals used in various industries, such as agrochemicals, paints, pharma, FMCG and others. Moreover, the company follows eco-friendly manufacturing processes, which provide it with further growth opportunities. With current capacity utilisation pegging at 72 per cent, planned capacity expansion, zero debt, diverse applications and industry tailwinds, the company will be able to scale up its business.

3. Does the company have recognisable brand/s, truly valued by its customers?

Not applicable. Since the company is primarily a B2B supplier of speciality chemicals, the concept of brand recognition is not really applicable.

4. Does the company have high repeat customer usage?

Yes. The company's products are used as the key starting-level materials, like inhibitors or additives by its customers, for making finished products. The criticality of products leads to long-term relationships and high repeat usage between the company and the customers. Revenues generated from the top 10 customers accounted for 47.9 per cent of the company's total revenues in FY21. As indicated by the management in the call, the company has not lost even a single customer in the past ten years.

5. Does the company have a credible moat?

Yes, the company is either the largest or one of the leading producers in the world for its primary products such as MEHQ, BHA, guaiacol, anisole and others. Additionally, the company has backward-integrated its operations with the manufacturing of anisole from phenol by deploying vapour phase technology, which is environment friendly.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No. The chemical industry is hazardous and causes pollution. Although green chemistry - the processes that reduce or eliminate the generation of hazardous substances - is gaining popularity, the current state of industry makes it prone to regulatory risks.

7. Is the business of the company immune from easy replication by new players?

Yes. Speciality chemicals are highly technical in nature. Further, close relationships with customers and a long gestation period of around three years for new product commercialisation make the business immune from easy replication by new players.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. The nature of the company's various chemical products is not expected to be disrupted or outdated. Moreover, chemical companies have started producing chemicals in an eco-friendly manner and the company is already involved in such practices, as most of its production processes release zero liquid or only water as discharge.

9. Are the customers of the company devoid of significant bargaining power?

No. Customers of the company are various B2B players in India and other regulated markets such as China, Canada, Europe and others. The top 10 customers accounted for around 48 per cent of its FY21 revenue. The dominance of such big customers provides them with significant bargaining power.

10. Are the suppliers of the company devoid of significant bargaining power?

No. The primary raw materials used in manufacturing products include crude-oil derivatives and other commodities such as hydrogen peroxide. The company doesn't enter into long-term supply contracts and generally does spot purchases.

11. Is the level of competition the company faces relatively low?

No. Although the company has a market share of around 44 per cent in performance chemicals (around 70 per cent of the FY21 revenue), the overall competition in the chemical sector is intense, owing to the presence of several large and smaller players.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. Post the IPO, the promoter group will hold around 78 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. Family members of the promoter group are in the top management and have a combined experience of more than 15 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. The company is free from any material litigation.

16. Is the company's accounting policy stable?

Yes. As per the auditor's report, the company has a stable accounting policy.

17. Is the company free of promoter pledging of its shares?

Yes. None of the promoter's shares are pledged.

Financials

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes. The last three-year average ROE and ROCE stood at 37.8 per cent and 61 per cent, respectively.

19. Was the company's operating cash flow positive during the previous three years?

Yes. The company had positive operating cash flow in the past three years till FY21.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. During FY19-21, its revenues grew by 15.3 per cent YoY.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes. The company is debt-free.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. The working-capital cycle for the company came down to 47 days in FY21 from 69 days in FY19. Moreover, it is free from short-term debt and has ample current assets in the form of investments (Rs 232 crore as of FY21) to meet working-capital needs.

23. Can the company run its business without relying on external funding in the next three years?

Yes. The company in the past has done capacity building through internal accruals without relying on external debt. Capacity utilisation across its units currently stands at around 72 per cent, which provides room for further growth without any need for external capital. Moreover, the management plans to do further capacity expansion by using internal accruals.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. As of FY21, the company did not carry any short-term borrowings.

25. Is the company free from meaningful contingent liabilities?

Yes. The company doesn't have any meaningful contingent liabilities.

The stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. Based on post IPO enterprise value, the company will give an operating-earnings yield of around 3 per cent.

27. Is the stock's price-to-earnings less than its peers' median level?

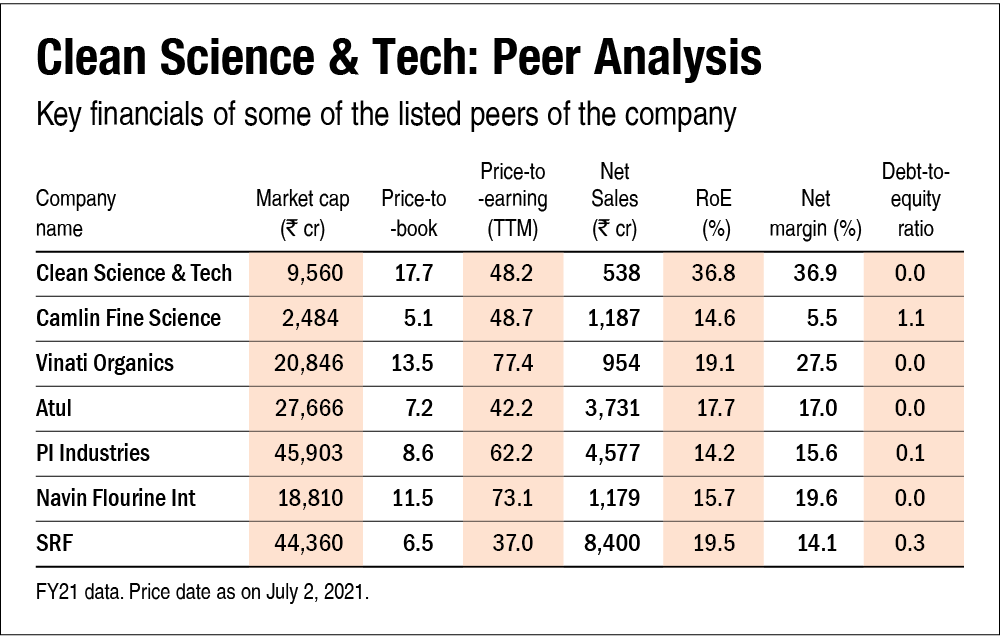

Yes. Post IPO, the company will trade at a P/E of 48.2 based on FY21 earnings, which is lower than the industry's median P/E of 55.5.

28. Is the stock's price-to-book value less than its peers' average level?

No. Post IPO, the company will trade at a P/B of 17.7 based on FY21 book value, which is higher than the industry's median P/B of 8.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()