The largest supplier of buns to quick service restaurant (QSR) chains like McDonald's, Burger King, KFC and others in India, Mrs. Bectors Food Specialties (Mrs Bectors) is coming out with its IPO. Mrs Bectors belongs to the Punjab-based Cremica group. The group deals with a range of food products like sauces, snacks, jams, spreads, syrups, biscuits, bakery and others. In 2013-14, group businesses were divided among three brothers, with Mr Anoop Bector heading Mrs Bectors.

Primarily involved in manufacturing premium and mid-premium biscuits (65 per cent of FY20 revenue) and premium bakery (34 per cent) products, Mrs Bectors sells a range of biscuits, such as cookies, creams, crackers, digestives and glucose under the parent brand Mrs Bector's Cremica. On the other hand, its bakery division sells bread, buns, pizza bases and cakes under the English Oven brand in Delhi NCR, Mumbai, Pune and Bengaluru. Bakery products are sold to both retail and institutional customers, including QSR chains. The company also exports biscuits to around 64 countries, which accounted for 22 per cent of the FY20 revenue.

With its focus mainly in North India, Mrs Bectors has a distribution reach of 458,000 retail outlets under the biscuits division and over 14,000 retail outlets under its bakery division. The company is still a minnow compared to other big players. In FY20, it had a market share of just 4.5 per cent in the premium and mid-premium biscuits segment in North India, whereas its market share in the branded bread market was just 5 per cent.

The company has aggressive plans to pursue growth in other parts of the country and is planning to go for a Rs 100 crore greenfield project in Madhya Pradesh in 2023. The company's growth story looks promising, now it's the execution that would matter.

The Issue

The total size of the issue is Rs 540.54 crore. Majority part of the issue is offer for sale aggregating Rs 500 crore by Linus Private Limited, Mabel Private Limited, GW Crown PTE. Ltd and GW Confectionary PTE. Ltd. On the other hand, the proceeds from a fresh issue of Rs 40.54 crore will be used to finance the project costs of its Rajpura expansion plan, which is aimed at establishing a new production line for biscuits.

Strengths

- Quality control through in-house manufacturing: The company has six in-house manufacturing facilities across five states. It has quality certifications from various regulatory bodies, such as FSSC 22000, the US FDA, the British Retail Consortium and others.

- Strong relationship with institutional and QSR players: The company has been associated with McDonald's since 1996 and is its sole supplier of buns in India. Besides, it is the largest supplier of buns to other QSR chains like Burger King, KFC, Carl's Jr and others. Its relationship with multinational companies has helped the company maintain high-end product quality control and standardisation.

- Strong brand image: The company sells its biscuits under the brand name 'Mrs. Bector's Cremica'. Although it is restricted to use this brand name only for biscuits, the Cremica brand is associated with a range of food products like sauces, snacks, jams, spreads, syrups and others. This umbrella of various brands provides better visibility to the company.

Risks/Concerns

- The company is vulnerable to political and regulatory changes. It exports its biscuits to around 64 countries, including to African countries, North America, Europe, MENA and others. In FY19, owing to political and financial instability in certain African countries, the company faced issues like delayed payment and even non-payment. Therefore, it had to reduce exports to African countries.

- A formidable FMCG business is built on a strong distribution channel. Despite focusing on the North Indian market, the company's retail touchpoints at around 4 lacs is less than one fourth that of Parle's.

- The company is restricted to use the brand, Mrs. Bector's Cremica, only for the biscuits segment. For launching new brands and products, it will need to continuously incur advertisement and marketing expenses, which can affect its profitability.

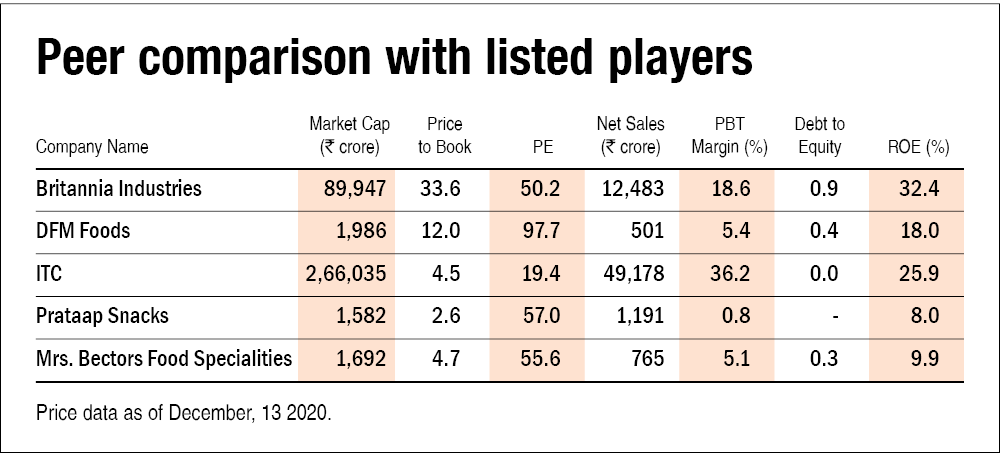

- During the last three years till March 2020, the company spent roughly 1.6-2 per cent of the revenue on ad expenses, which was way lower than that done by bigger players. For example, Britannia Industries, which has the largest market share in the Indian-branded biscuits market, spends around 4 per cent of its revenue on advertising and marketing expenses.

- The company operates in highly competitive biscuits and bakery industries. In both industries, the company is a minnow. In the biscuits division, it has a market share of just 1 per cent of the branded biscuits division, while in the branded bread division, its market share is 5 per cent. Its small size prevents the company from having a durable competitive advantage.

Total IPO size: Rs 540.54 crore

Purpose of issue: Disinvestment of the stake by P/E firms and expansion of Rajpura manufacturing facility

Fresh issue: Rs 40.54 crore

Offer for sale: Rs 500 crore

Additional details

Price band: Rs 286-288

Subscription dates: December 15-17

ROE (FY20): 9.92 per cent

Revenue (FY20): Rs 762 crore

Profit after tax (FY20): Rs 30 crore

Post-IPO, promoter holding: 51 per cent

Post-IPO, market cap: Rs 1680-1692 crore

Total debt: Rs 101.2 crore as on September 30, 2020

Net worth (Post IPO): Rs 398 crore (as on Sep 30, 2020)

Price/earnings ratio: 28.6 based on TTM net profit

Price/book ratio: 4.7 as of September 2020

Retail allocation: 35 per cent

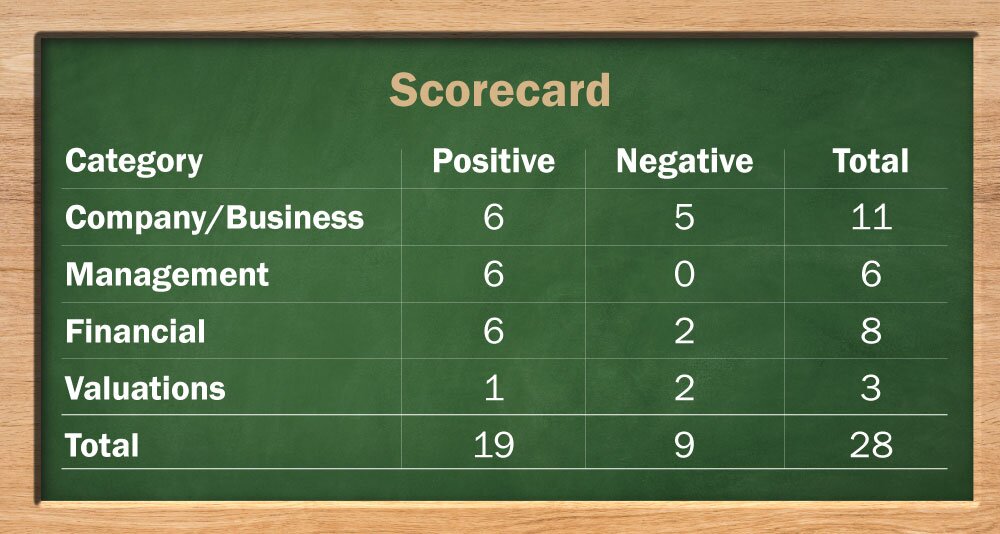

Company/Business

1. Are the company's earnings before tax more than Rs 50 cr in the past twelve months?

No, the company reported profit before tax of Rs 39.2 crore as of March 2020.

2. Will the company be able to scale up its business?

Yes. Even though the company has a major focus on North India, its market share in the premium and mid-premium biscuits for this region remains low at 4.5 per cent. On the other hand, the company's bakery business, under the brand name 'English Oven', is one of the fastest-growing large-scale bakery brands in India. With six manufacturing facilities across five states, the distribution reach to more than 4 lakh retail outlets and new product launches, the company can scale up its business.

3. Does the company have a recognisable brand (s), which is truly valued by its customers?

Yes, following the Cremica group's business division in 2013-14 (see intro), the company was restricted to use Mrs Bector Cremica only for its biscuits business. However, the brand 'Mrs. Bector's Cremica' has a strong brand appeal among customers who associate the brand not only with biscuits but also with sauces, snacks etc. Also, the company's bakery brand, English Oven, which started in 2013, has quickly scaled up and occupies around 5 per cent of the branded bread market in India.

4. Does the company have high repeat customer usage?

Yes, the company's main products - biscuits and bakery - have a short shelf life and are consumed on a daily basis. In the biscuits division, the company is mainly a regional brand with a focus on North India. Britannia and Mrs Bector Cremica are the top two biscuit players in the premium and mid-premium biscuit segments in Punjab, Himachal Pradesh, Ladakh and J&K. Also, the company has a strong association with QSR chains. It is the largest supplier of buns to chains, such as McDonald's, Burger King, KFC and others. Its association with McDonald's dates back to 1996. Repeated consumption, moderate dominance in the focused markets and long-term relationship with institutional customers provide the company with high repeat customer usage.

5. Does the company have a credible moat?

No, the company competes with big national players like Britannia, Parle and ITC in the biscuits segment. These three players together occupy around 65 per cent of the branded biscuit market in India as compared to just 1 per cent of the Mrs Bectors. Even in the bread division, the company holds a market share of just 5 per cent. The company's ad and marketing expenses stand at around just 1.6 per cent of the revenue as compared to 4 per cent of Britannia Industries. Its retail touchpoints in North India for biscuits is less than one-fourth that of Parle. Low brand-building expense, small-scale operations and insufficient retail reach prevent the company from forming a credible moat.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company's export business, which contributes roughly 22 per cent, suffered in FY20 because of political and financial instability in certain African countries in FY19. Although the company has in-house manufacturing facilities and is certified from major food regulators, food companies are especially vulnerable to quality risks.

7. Is the company's business immune from easy replication by new players?

Yes. The company's products like premium and mid-premium biscuits varieties like cookies, creams, digestives and forms of bread and bakery products can be replicated easily. However, the brand name and recognition and the distribution channel built over the years are very hard for newer players to replicate.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, the company's main products are biscuits and bakery products. Although these products have seen premiumisation because of improving lifestyle and rising income level of consumers, they can't be substituted or outdated easily.

9. Are the customers of the company devoid of significant bargaining power?

No, the biscuits and bakery industries in India are highly competitive. When it comes to retail customers which contribute roughly 78-80 per cent to the revenue, they have the choice of not only switching to other biscuit brands but also changing their consumption habit.

On the other hand, the institutional customers like QSRs, canteen store department (CSD) and others, which contribute roughly 20-23 per cent to the revenue, have significant bargaining power because of their size.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, primary raw materials include refined wheat flour, oil and fats, sugar, packaging materials and others. These formed around 53.5 per cent of FY20 revenues. Since these items are commoditised nature, suppliers don't have any significant bargaining power.

11. Is the level of competition the company faces relatively low?

No, the biscuits and bread industries in India are highly competitive. In the branded biscuits market, the company's market share was just 1 per cent, while in the branded bread market, its market share was 5 per cent as of FY20. In both these markets, the top three players dominate the market share.

Management

12. Does any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, following the IPO, the promoter group will hold around 51.1 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, the promoter and MD, Anoop Bector, has been associated with the company since the beginning and has an experience of 25 years. On the other hand, the chief financial officer has been associated with the company for more than 10 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise. However, in the past, the promoter of the company has been subject to disciplinary action by an erstwhile recognised stock exchange, OTC Exchange of India, for the violation of the listing requirement of a promoter group company, CAFL, in which the promoter has 1.12 per cent stake.

15. Is the company free of litigation in court or with the regulator that casts doubt on the intention of the management?

Yes, there is no material litigation going on against the company.

16. Is the company's accounting policy stable?

Yes, the company's accounting policy has been stable.

17. Is the company free of promoter pledging of its shares?

Yes, none of the shares held by promoters are pledged.

Financial

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the last five-year average ROE till March 2020 stood at 14 per cent.

19. Was the company's operating cash-flow positive during the previous year and at least four out of the last five years?

Yes, cash from operations stood at Rs 109 crore and has been positive in each of the last five years.

20. Did the company increase its revenue by 10 per cent CAGR in the last five years?

No, the company grew its sales by around 5.5 per cent during the last five years till March 2020.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company has a net debt-to-equity ratio of 0.23 as of September, 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company's working capital stood at around 6 per cent of sales as of FY20. However, the working-capital days are inching up over the last few years and stood at around 35 days as of March 2020.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company is raising Rs 40 crore from the IPO for the expansion of biscuit production at its Rajpura, Punjab facility. Further, the company is planning to do a greenfield project in Madhya Pradesh in 2023. This project is expected to cost Rs 100 crore and the entire amount will be funded through internal accruals.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the company has reduced its short-term borrowings over the years and had zero short-term borrowings as of September 2020.

25. Is the company free from meaningful contingent liabilities?

Yes, the entire amount of contingent liabilities stood at roughly 3.5 per cent of equity as of September 2020, which isn't problematic.

The Stock/Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No, the stock will offer a yield of 5 per cent post IPO based on September 2020 numbers.

27. Is the stock's price to earnings less than its peers' median level?

No, following the IPO, the stock will be priced at around 55 times its FY20 net profit, which is around the peers' median P/E of 54. However, based on TTM earnings the P/E stands at 28.6.

28. Is the stock's price-to-book value less than its peers' average level?

Yes, following the IPO, the stock will be priced at 4.7 times its September-2020 book value, which is lower than the peers' median PB of 8.2.

BRLM- SBI Capital Markets, ICICI Securities, IIFL Securities

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()