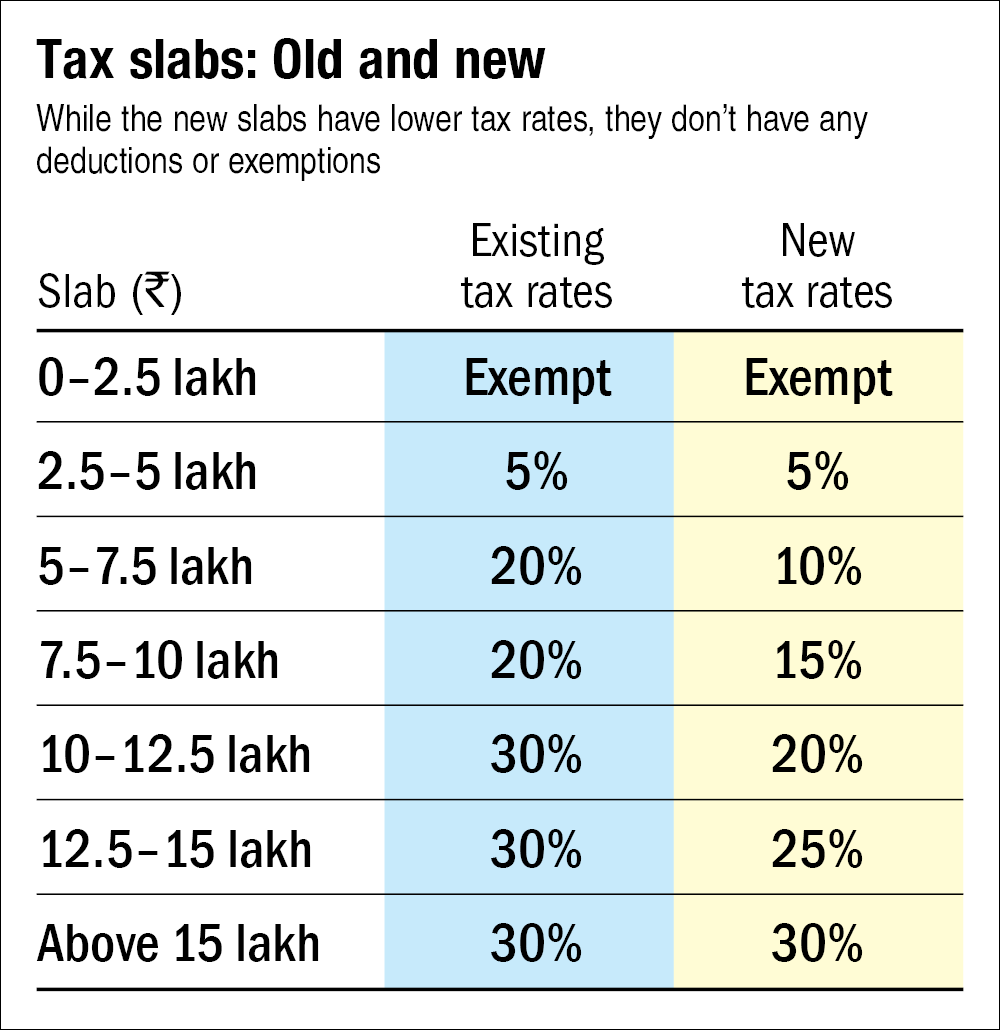

This financial year comes with new tax slabs, though the old ones also remain. You have to choose between the two. While the older ones allow you to avail many exemptions and deductions, which can bring down your overall taxable income, the new tax slabs have lower rates of taxation but you will have to forgo your exemptions and deductions. In such a scenario, many are wondering which tax slabs they should choose. Before we start, have a look at both the old and new tax slabs:

Why the new slabs?

In her Budget speech, the finance minister said that simplification was the main motive behind the new tax slabs, apart from easing the tax burden. She said, "It was surprising to know that currently more than one hundred exemptions and deductions of different nature are provided in the Income Tax Act. I have removed around 70 of them in the new simplified regime. We will review and rationalise the remaining exemptions and deductions in the coming years with a view to further simplifying the tax system and lowering the tax rate."

In the new tax structure, while some 70 exemptions have been removed, about 50 do stay. These include the deduction for agricultural income, leave encashment on retirement, standard deduction on rent and some other miscellaneous items. However, all those exemptions and deductions that are generally the mainstay of tax-planning are gone in the new tax structure. Fortunately, the new tax structure is optional. If the existing slabs and exemptions save you more tax, you can very well adhere to them. What's more, the salaried can choose between the original and the new tax structures every year. But businesspersons don't have this flexibility. They have to follow the same taxation system in the future after they have chosen between the two options.

Which should you choose?

The new tax slabs are indeed simpler. You don't have to worry about documentation or last-minute tax planning. For those who want more money in hand, such as those in lower income brackets or those who want to take control of their finances rather than let the government decide where to invest, these could be useful. However, this simplicity comes at a cost.

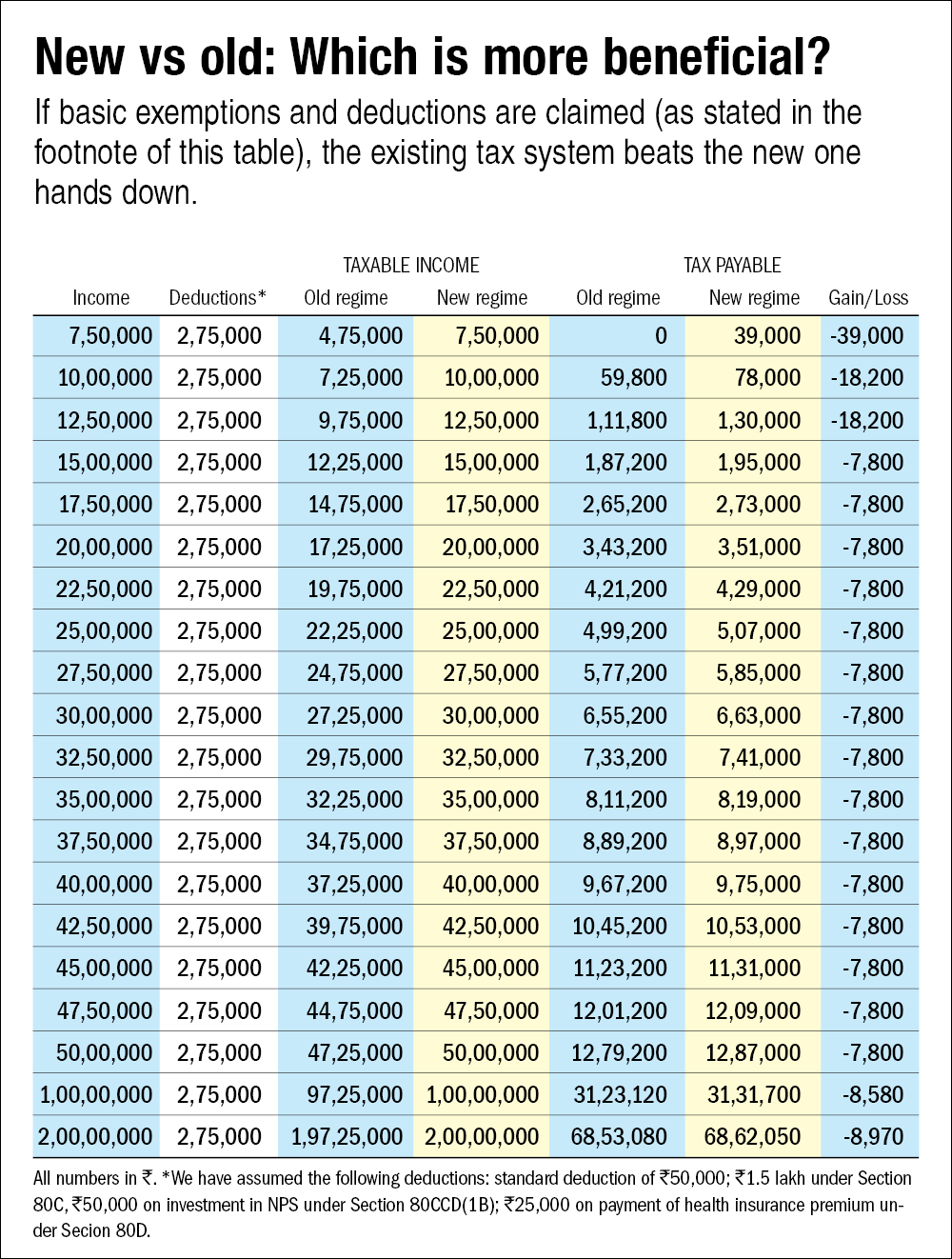

The first cost is that you don't really pay less tax with the new tax structure, as claimed by the finance minister. The table 'New vs old: Which is more beneficial?' shows that if you claim the basic exemptions and deductions - Rs 1.5 lakh under Section 80C, Rs 50,000 under Section 80CCD(1B) and Rs 25,000 under Section 80D, apart from the default standard deduction of Rs 50,000 - you can pay less tax than that in the new system. Of course, if you include other exemptions and deductions, such as house-rent allowance, you could be paying even less tax. Even if you exclude the Rs 50,000 NPS contribution in the table, still you save more than that in the new system.

The second cost is that if you follow the new tax slabs, you may compromise on savings. No matter if tax-planning is pesky for some of us, it forces us to save. If not forced to, many of us don't save enough. This can result in financial complications in the future, including during retirement. For the young generation especially, the new tax slabs can result in higher spending and less saving. With rising consumerism, there are many avenues to spend and with the new tax slabs, one major saving avenue will be gone.

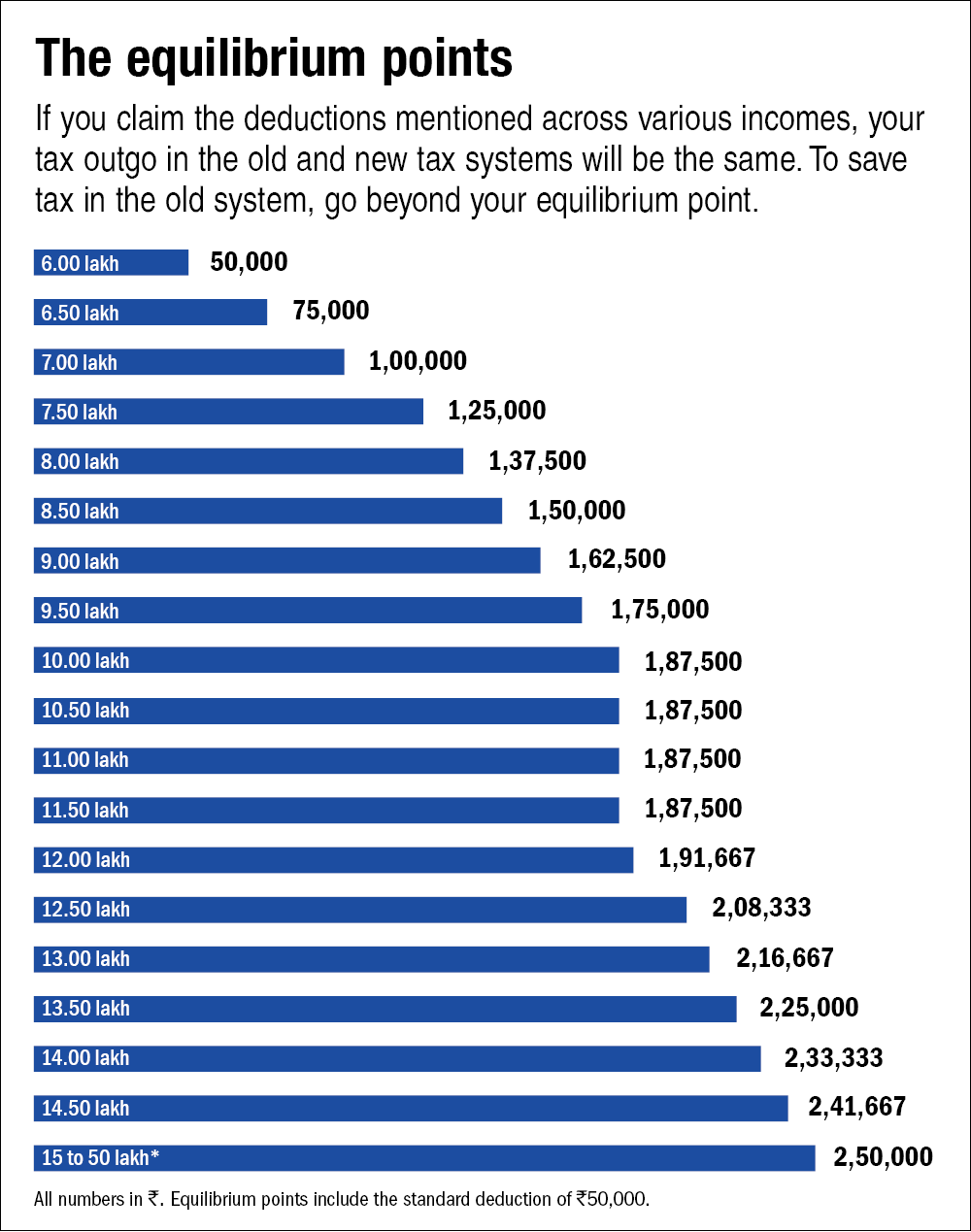

Everyone will have their own set of deductions and exemptions. Hence, we have worked out equilibrium points for various income groups. These represent the amount of deduction that brings the old and new tax structure at par in terms of the tax payable. Any further deductions from these equilibrium points will make the old system beneficial as your tax outgo would reduce. If your tax-admissible expenses and investments (not just 80C and 80D ones but also your HRA, donations under Section 80G, etc.) are more than the given equilibrium level, you can stay with the old tax structure. Otherwise, the new one's for you.

For stock lovers

Those who want to invest in stocks for their tax-saving requirements have the following options: tax-saving funds, National Pension System (NPS) and unit-linked insurance policies (ULIPs). Even the Employees' Provident Fund invests part of its corpus in index ETFs. All these come under the Section 80C of the Income Tax Act. Let's look at each of them.

ULIPs provide you insurance cover and invest your premiums in the stock market. This sounds like a great deal but it isn't. Neither the insurance cover nor the returns are optimal. The costs involved are high and there is often a lack of transparency. At Value Research, we advise investors to keep their insurance and investments separate. For life insurance, buy a good term plan.

Next comes the NPS, which is a retirement-investment vehicle. It provides auto and active options. The auto option has a pre-decided equity and fixed-income mix that keeps tapering with your age in favour of fixed income. The active choice lets you decide your equity- debt mix subject to some age-related upper limits.

The NPS is especially useful to avail an additional tax deduction of Rs 50,000 under Section 80CCD(1B). Its low cost is another plus. However, since it's a retirement tool, the NPS locks in your money until you turn 60, though there are some avenues when you can make partial withdrawals. On maturity, you must use 40 per cent of the proceeds to buy an annuity. The rest 60 per cent can be withdrawn as a lump sum. NPS proceeds are tax-free but annuity payouts are taxable as per your slab.

Tax-saving funds are the most efficient way to save tax and build a long-term corpus. They invest in equity and can invest in companies of all sizes. They are transparent, have the shortest lock-in period of three years among 80C investment options and can be most rewarding if held for the long run. The competition between the ELSS schemes of various fund houses ensures that the fund managers are on their toes to deliver.

You can find an elaborate coverage of tax-saving funds here. If you type the name of such a fund in the search bar, you will get a page full of information about that fund, including its rating, returns, portfolio, expense and so on.

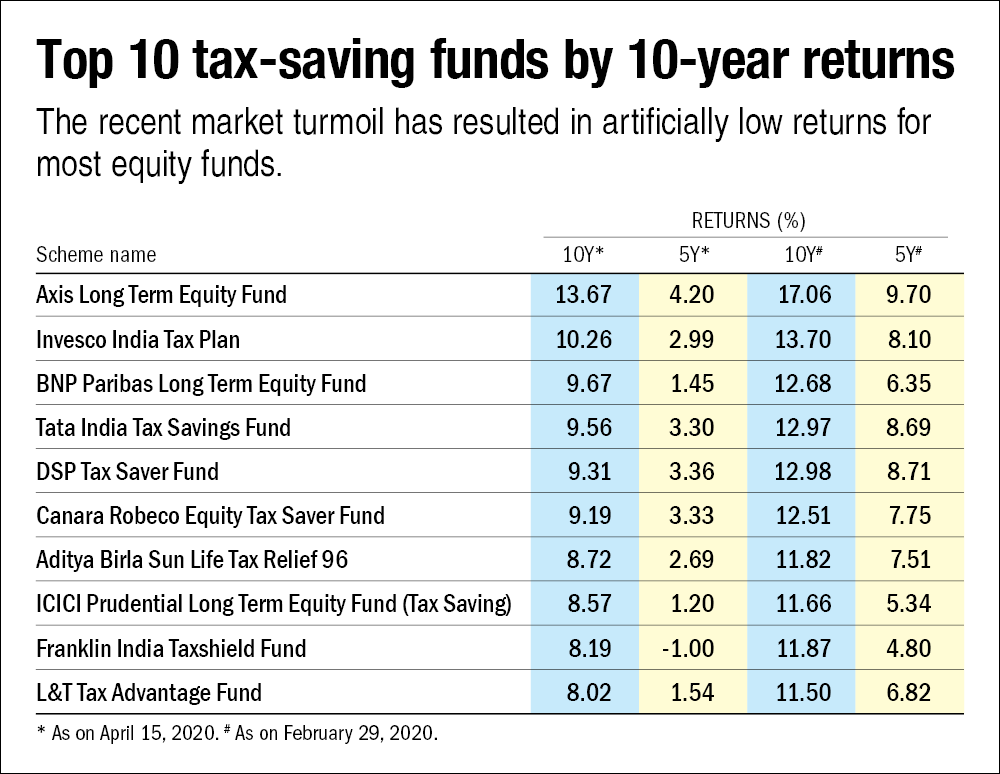

The table below lists top 10 tax-saving funds over the last 10 years. Because of the recent fall in the market, their returns may appear subdued but if you see their returns until February 2020, they are not just ahead of inflation but also highly rewarding.

Tax-saving funds are the best choice to save tax and build a corpus for a long-term goal. Systematic investments in them throughout the year don't just help you efficiently save tax but also help you average your investment cost.

This article was originally published on June 18, 2020.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()