2018 was a lacklustre year for the markets. Following a dry run of listings, a couple of IPOs have recently listed in the markets, with Metropolis Healthcare coming out with a Rs 1200-crore IPO on April 3, 2019.

A leading diagnostics chain in India, Metropolis Healthcare provides a wide range of clinical laboratory tests for the detection and diagnosis of diseases. At present, it is providing 3487 clinical laboratory tests and 530 profiles. Leveraging a 'hub and spoke' model, the company now has 115 clinical laboratories, with its main 'hub' being in Mumbai. This Mumbai-based hub is the company's global reference laboratory wherein a majority of tests are conducted. Its satellite laboratories (the 'spokes'), on the other hand, are well-equipped to conduct all routine and semi-specialised tests. Currently, the company is operating a total of 56 satellite labs, along with 44 express labs which conduct routine tests.

A leading diagnostics chain in India, Metropolis Healthcare provides a wide range of clinical laboratory tests for the detection and diagnosis of diseases. At present, it is providing 3487 clinical laboratory tests and 530 profiles. Leveraging a 'hub and spoke' model, the company now has 115 clinical laboratories, with its main 'hub' being in Mumbai. This Mumbai-based hub is the company's global reference laboratory wherein a majority of tests are conducted. Its satellite laboratories (the 'spokes'), on the other hand, are well-equipped to conduct all routine and semi-specialised tests. Currently, the company is operating a total of 56 satellite labs, along with 44 express labs which conduct routine tests.

In India, the company has a presence in 197 cities. Besides, it enjoys a global footprint with 17 clinical laboratories, 28 patient touch points and seven assisted referral centres.

Strengths

As a professionally-managed, promoter-led company, Metropolis Healthcare was transformed from a standalone pathology laboratory into a recognised national diagnostic chain by its managing director, Ms Ameera Shah. With 1631 patient touch points and 9552 institutional touch points, the company boasts a strong network, which provides it with an edge in the market. The company was able to gain the highest revenue per patient at Rs 847 in nine months ending December 31, 2018, which was significantly higher than its listed competitors, Dr Lal Pathlabs and Thyrocare.

Over the past few years, the company has achieved inorganic growth through acquisitions. However, despite this, it has been net debt free for the past three years. In FY18, Metropolis gave a higher return on net worth of 27 per cent as against 25 per cent of Dr Lal Pathlabs and 21 per cent of Thyrocare.

When it comes to revenue generation, the contribution from its individual patients increased to 51 per cent in 9MFY19. Going further, the company is planning to increase it to 60 per cent by expanding its network through third-party patient service centres.

Weaknesses

Even though the company boasts of its widespread presence, about 50 per cent of its revenues come from five cities, namely Mumbai, Bengaluru, Chennai, Surat and Pune. This makes Metropolis prone to various region-specific risks.

Another point to consider is its high dependence on vendors for its testing equipment. The company has agreed upon certain minimum quantities and values of purchasing the equipment. However, any breach can suspend its relations with vendors, thereby disrupting its operations.

Furthermore, its promoters have pledged 28 per cent of the total share capital, owing to loans taken by one of its promoters, Mets Advisory LLP. Promoters have also given personal guarantees for the same debt.

Risks and Concerns

In this sector, there are some stringent regulations, such as disposing of biomedical waste, which attracts penalties. Further, if the government introduces any price regulation on tests, it may have an adverse impact on the company's margins. A high degree of competitive intensity in the field lowers the scope to increase the company's operating margins.

The company, its directors and promoters, on the other hand, are involved in several civil and criminal cases, which may attract penalties and affect the company's operations adversely.

Another major risk is the quality and collection of specimens. Since Metropolis depends significantly on third-party service providers for the collection of specimens, any negligence by these service providers or their franchisees can give a serious blow to its brand name.

Industry

In India, the diagnostic industry has a mere 16 per cent market share in the healthcare sector. Hospital-based laboratories have the advantage of a captive patient base with inpatients and outpatients. On the other hand, standalone labs have loyalty among local customers. So, these two factors provide stiff competition to diagnostic chains. As per the company's prospectus the Indian diagnostics market was valued at Rs 596 billion in the financial year 2018.

Furthermore, the absence of any major regulatory hurdles has paved the way for standalone laboratories and various startups to replicate the business. These days, diagnostic chains are increasing their presence by adopting the franchisee model or acquiring smaller players in the market. Besides, a change has been noticed in consumer behaviour, with people choosing branded players over local laboratories.

How would the IPO proceeds be applied

Fresh issue -NIL

Offer for sale - Rs 1200 - Rs 1204 crores

Dr. Sushil Kanubhai Shah - Rs 551 crores

CA Lotus Investments - Rs 652 crores

Additional details

Price Band - Rs 877-880

Total IPO size - Rs 1200 - 1,204 crores

Subscription Dates - 03-05 April, 2019

ROE (FY 2018) - 27.7 per cent

Revenue (FY 2018) - Rs 643.6 crores

Post-IPO, promoter holding will fall from 67.8 to 55.3 per cent

Post IPO valuation - Rs4401 - 4416 crores

Total net debt (Post IPO) - Nil

Equity (Post IPO) - Rs 468 crores

Retail Allocation : 10 percent

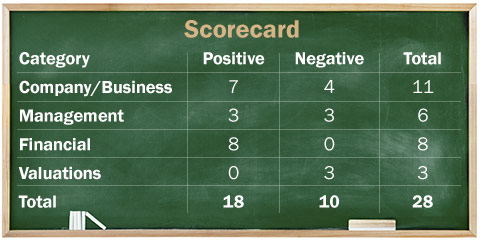

Company / Business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes. Profit before tax for FY18 is Rs 160 crore

2. Will the company be able to scale up its business?

Yes. The company has identified eight seeding cities and regions where it sees the potential to expand. The company has serviced largely lesser number of patients (6.6 million) compared to its listed peer Dr Lal Pathlabs (13.3 million). So, it should add more patient touch points to expand its reach. Furthermore, the growing awareness of preventive healthcare and wellness will also provide a major boost to the company.

3. Does the company have a recognisable brand/s truly valued by its customers?

Yes. The company has built itself a recognisable brand in 5 cities, namely Mumbai, Bengaluru, Chennai, Surat and Pune.

4. Does the company have high repeat customer usage?

Yes. Given its continued focus on five cities and the nature of the diagnostic chain business, high repeat customer usage is common. Furthermore, it is planning to increase its share of revenues from its individual patients up to 60 per cent in the coming years.

5. Does the company have a credible moat?

No. The company's business can be easily replicated as is evident with the intense competition it faces. Further, there aren't any major regulatory hurdles that may come in the way of setting up such a business.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No. Any changes in regulations, such as pricing caps on the tests, can have an impact on the company's financials. Any further geopolitical or regulatory risks in its 5 focus cities can impact its operations adversely as well.

7. Is the business of the company immune from easy replication by new players?

No. The business model is not unique and has low barriers to entry, along with no major regulatory hurdles.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. As of now, there is no such technology and testing processes available.

9. Are the customers of the company devoid of significant bargaining power?

Yes. Metropolis like other diagnostic chains offers a comprehensive range of tests under a recognised brand name. Their tests which come in customised packages and offer higher quality and lower probability of errors due to their stringent quality control measures are preferred by their customers. Hence customers do not really try to bargain at such centres as prices are fixed to a large extent.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes. There are no such shortage of suppliers in the market for medical testing equipment however there are very few diagnostic chains like metropolis that have a constant need for equipment on lease. This can be credited to their aggressive expansion plans.

11. Is the level of competition the company faces relatively low?

No. The company faces stiff competition from the unorganised sector and hospital-based laboratories. Hospitals have the advantage of a captive patient base and local standalone clinics have customer loyalty in the areas they operate and hence are able to compete with diagnostic chains to some extent.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. The promoters hold 67.8 per cent, prior to the issue and will hold 55.3 per cent post the issue.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. Dr Nilesh Shah (Group president and head of science and innovation) has been associated with the company since 1987. However, its CEO and CFO have been associated with the company since 2016.

14. Is the management trustworthy? Is it transparent in its disclosures in line with Sebi guidelines?

No. There are several civil and criminal cases against the promoters. These include allegations of criminal breach of trust and trespassing owing to illegal constructions carried out in its registered office; filing of forged documents with the ROC; illegal dumping of medical waste; defamation and so on.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No. There are several litigations against the company that include medical negligence, non-payment of employee provident funds and illegal constructions carried out on its premises.

16. Is the company's accounting policy stable?

Yes. However, auditors have qualified the report in the past on unavailability of data of one of the companies it acquired a stake in.

17. Is the company free of promoter pledging of its shares?

No. Promoters have pledged 42 per cent of their holding post the issue, which translates into 28 per cent of the total share capital.

Financial

18. Did the company generate current and five-year average returns on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes. The company generated current ROE of 27.7 per cent in FY18 and a 5-year average of 24.5 per cent. The company generated current ROCE of 43.7 per cent and 5-year average ROCE of 38.6 per cent.

19. Was the company's operating cash flow-positive during the previous year and at least four out of the last five years?

Yes. The company's operating cash flows have been positive for the last 5 years.

20. Did the company increase its revenue by 10 per cent CAGR in the last four years?

Yes. The company has increased its revenue by 13.5 per cent CAGR in the last four years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes. The company is debt free on a net debt basis (cash and bank less total debt).

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. The company follows an asset-light model and its working capital requirements have been stable in the past.

23. Can the company run its business without relying on external funding in the next three years?

Yes. The company follows an asset-light model and has sufficient cash and bank balances and generates positive free cash-flows, which is sufficient for operations.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15%)?

Yes. The company is free from any short-term debt on a net debt basis.

25. Is the company free from meaningful contingent liabilities?

Yes. The company has quantified its contingent liabilities as on December 31, 2018, to the tune of Rs 13.19 crore. This is only around 2.8 per cent of their net worth of Rs 468 crore as on December 31, 2018.

Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No. The stock at the upper price band offers an earnings yield of 3.72 per cent.

27. Is the stock's price to earnings less than its peers' average level?

No. The stock at the upper price band will trade at a PE (earnings of FY 18) of 43 times at the upper price band as compared to its peers' median level of 37 times.

28. Is the stock's price-to-book value less than its peers' average level?

No. The stock's price-to-book value of 9.4 is more than its peers' average level of 8 times.

Book running managers:

JM Financial Limited,Credit Suisse Securities (India) Private Limited, Goldman Sachs (India) Securities Private Limited, HDFC Bank Limited and Kotak Mahindra Capital Company Limited

* The lower the score you find here, the riskier the stock

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()