Every fund house and brokerage that markets its money-management expertise to investors claims that it follows a process steeped in 'fundamental research'. The implicit assumption is that corporate earnings drive stock prices over the medium to long term and by making reliable forecasts of these earnings, a portfolio can be positioned for better-than-benchmark performance. But what if this were not quite the case? What if reported earnings were unable to adequately explain future price movements?

Baruch Lev, a professor at NYU Stern School, and Feng Gu of the University of Buffalo published The End of accounting and the Path Forward for investors and Managers in 2016. It makes compelling reading even while dealing with a subject as dry as accounting.

Usefulness of financial information

Quoting from Financial Accounting Standards Board, USA, the authors point out, "The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders, and other creditors in making decisions about providing resources to the entity."

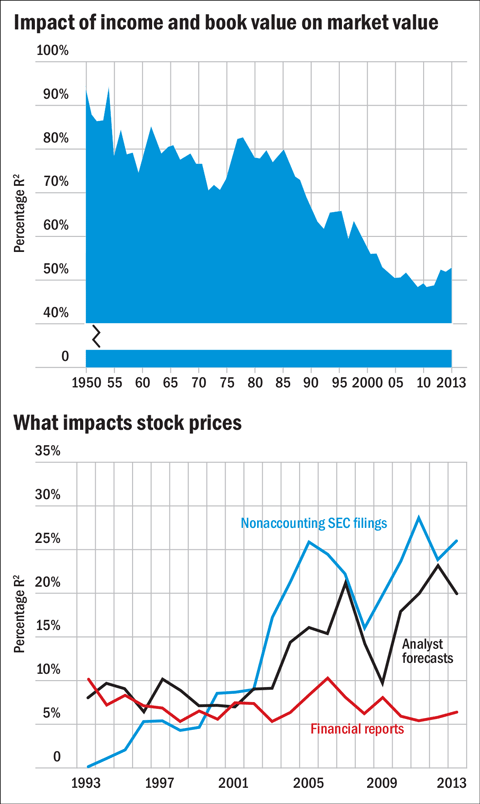

To measure how much store the equity market puts in financial numbers, Lev and Gu chose earnings or net profits and book value and regressed them against market capitalisation (see the first graph). As the figure indicates, while the decade of the 50s saw net income and book value explain between 80 and 90 per cent of market value, this has fallen to half in the current decade. This, despite increasingly complex disclosure requirements. The book then goes on to rigorously examine the separate information content of both inputs - with similar results. A whole series of test with other variables from the balance sheet and income statement does not improve results. It appears that financial numbers reported by corporates are not what is driving stock prices anymore.

To complete the investigation on what drives prices, the authors used other parameters.

As the second graph reveals, financial reports - both quarterly earnings and annual reports - seem to contribute around 5 per cent of the movement in stock prices. Large contributions are from analyst estimates and other non-accounting reports such as order wins, patent filings and the like.

In his blog on the book, Prof Lev quotes a study which seems to support the rather provocative blog title, 'Who Reads Financial Reports - Nobody!'. So what ails accounting and financial reporting?

Distorting facts

A telecom or media company spends money to acquire a customer. The subscriber is likely to pay over a period of time. The cost of client acquisition is required to be written off in the period the subscriber is acquired. This violates the concept of matching revenues and expenses. Consequently, for a rapidly growing company, while future earnings build up, current profits are low. The market will recognise this and pay (higher stock prices) while the accounting reports show losses. Accounting standards do not require the company to separately report the cost of customer acquisition, churn rate (rate at which subscribers drop off) - metrics crucial to forecast future profitability.

Software developed in-house, for example, by a bank or insurance company, will presumably provide long-term value and should qualify to be treated like an asset. Usually, software-development expense in the form of manpower cost is required to be written off, thereby increasing current cost and lowering asset value. Strangely, if the same software could be purchased from a vendor, it is capitalised. This and other intangibles like money spent on research and development, developing patents, business processes and networks, branding are all intangible assets that are not reflected in the balance sheets of companies despite these being 'strategic assets' that create future value. On the other hand, commoditised assets like land, building and computers - all purchasable with little differentiation - enjoy pride of place in financial reports.

In addition, requiring managements to estimate market values of non-tradeable assets and liabilities and to adjust for these in the earnings statement takes away from facts by bringing in subjectivity and, many a time, management fudge. There is no provision for disclosing how much of the reported earnings are based on estimates. Worse, there is no requirement to report how far off estimates turned out to be from reality. This allows management a wide latitude to report numbers that cannot be challenged or verified.

Effectively, the authors make a case that in trying to 'improve' financial reporting, standard setters have moved so far away from reality that the primary user of these reports - investors - no longer find these reports useful.

Back to basics

Lev and Gu make several specific recommendations on how financial reports can be made relevant again - by reporting numbers in a way that emphasises 'strategic assets' and how they are nurtured and grown by organisations. Further, they suggest that modified cash flows (adjusted for investments in these assets and after taking into account the cost of capital) are best used by investors for deciding on investments.

Another key recommendation is to reduce frequency of reporting to twice a year, with only a sales- and margin-reporting requirement for the quarter.

Like most regulations, the law of unintended consequences seems to have caught up with accounting. As the authors point out, despite the lip service paid to principle-based accounting, in reality, accounting regulations have become exceedingly complex in trying to lay out details of treatment for specific cases - thereby protecting managements and auditors - but to the detriment of actual users. Its time the trend be reversed. Regulations are difficult to change, but a wide reading of this book can throw up some debate on this much needed correction.

This article was originally published on November 13, 2018.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()