The best way is to say it bluntly: Your long-term investments must be kept in equity-backed investments. Not doing so will expose you to the dire spectre of old-age poverty. Except for the small proportion of people who have inherently inflation-linked lifelong income, everyone else must invest almost all their long-term investments in equity. Last week, I had concluded this column by showing that deposit-type savings yield very little real (above inflation rate) rates of return and those who depend on these exclusively need to save a lot more in order to avoid hardship in the future. Unless you have earn rental income that can be hiked periodically, or you have a government pension, you will have to fight inflation yourself.

How will you fight this battle? There's only one weapon you have, which is equity backed investments. However, the problem is India's investment culture, which is changing, but not fast enough.

Once upon a time, India was pure fixed-income country. Except for a tiny handful of punters, all financial investments were made into deposits of one kind or another. This was true at least till the mid-nineties. The only time the investor dabbled into equities was when he filled out his application form for an IPO, or just 'issue', as it was then called. And in any case, this 'issue' was seen more as a lottery ticket than a reasoned investment. Then, from about the mid-nineties onwards, there arose a small but distinct equity culture where individuals started investing in equity mutual funds in reasonable numbers. However, when seen in the context of the size of the saving population and the kind of money that is invested in deposit-type products, equity exposure is tiny.

To understand why inflation can be beaten substantially only by equity, let's step back and think from the basics. There are only two ways of investing money--either you can lend it to someone, or you can own your own business. When you lend, you get a basic return but do not share in the upside. For anyone who is good at doing business, the best way to invest is in your own. Fortunately, because of the existence of stock markets, any of us can become owners (or rather, part-owners) in a business. We can reap the financial advantages of being owners with very few challenges that the real owners face.

This means investing in equity. Equity could mean buying shares but for beginners it generally means investing in equity-based mutual funds. This may sound like a dogmatic statement, but it's actually a realistic one. To appreciate this, one should understand the source of equity profits. The ultimate source of profits in equity is the general growth of the economy. On an average, stocks should grow at a rate that is at least equivalent to the growth of the economy. And the inflation rate is built into the growth of the economy. If inflation is 5 per cent and the real economy grows at 5 per cent, then stocks on the whole could match 10 per cent.

And that's just the average. On top of that, as an investor, if you are able to select stocks that are better than the average (through a good equity mutual fund, for example), then you can beat the general rate of economic growth by a larger margin.

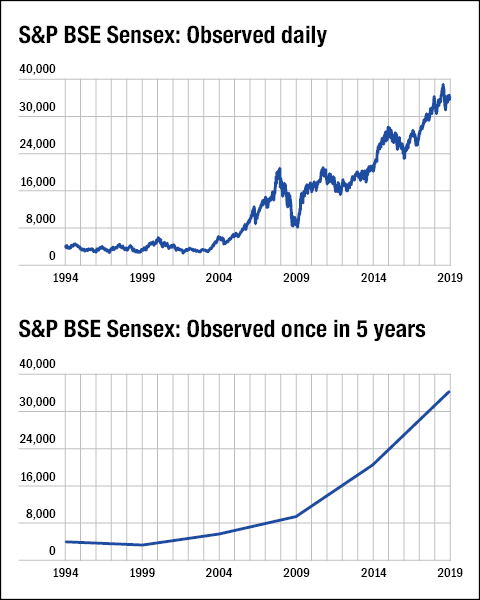

The fear that people have is that of volatility. The daily noise (I won't call it news) from the stock markets is such that the overwhelming impression we get is of volatility. However, this is but an illusion. If you were to look at the equity markets once every five years, you would consider them (and rightly so) the greatest investments in the world. Don't believe me? Take a look at the accompanying graphs. They tell a story you should take to heart and never forget.

Ask Value Research ![]()