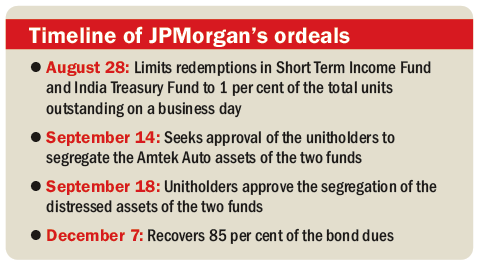

JPMorgan Mutual Fund has finally been able to recover 85 per cent of its exposure to Amtek Auto's stressed bonds. The crisis manifested itself when the fund house, on August 28, limited redemptions in two of its debt funds, Short Term Income Fund and India Treasury Fund, to 1 per cent of the total units outstanding on a business day. The fund house had to do so because the two funds had exposure to Amtek Auto's bonds for which the credit rating had been withdrawn. The withdrawal of the credit rating had made the fund house treat its exposure to Amtek Auto bonds as stressed. The redemption limits were meant to control the exodus of the investors from the two funds. The NAVs of the two funds were also hit on August 28. While the NAV of Short Term Income Fund declined from 15.335 to 13.310, India Treasury Fund fell from an NAV of 18.765 to 17.440.

On September 24, the fund house decided to segregate the stressed assets of the two funds into one fund and sought unitholders' approval for that. The resolution was approved on September 18.

This affair sent ripples through the entire industry. The exposure of debt funds to corporate bonds came under the SEBI's lens. The regulator stated at a couple of occasions that there is a need to control the risk that such exposures to corporate bonds bring. The SEBI also said that it's necessary to control credit-rating agencies. If credit ratings are going to change dramatically overnight, as what happened in Amtek Auto's case, then the role of the agencies awarding the ratings also becomes questionable. The regulator also felt a need for capping sectoral/company exposures for debt funds.

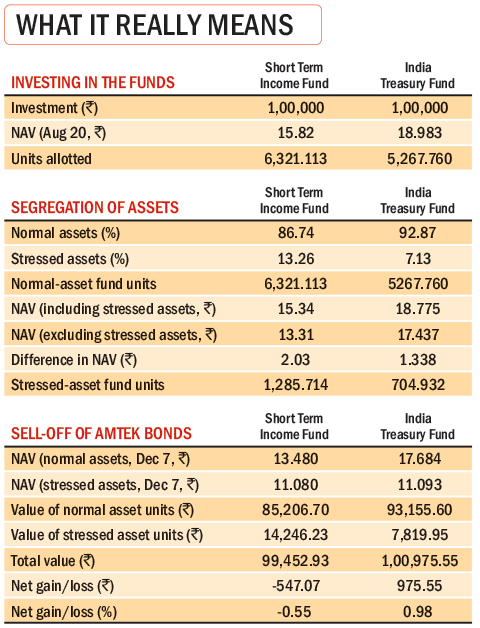

But what does all this really mean to an investor who had invested in the two funds? How much did he lose? If you had invested ₹1 lakh in Short Term Income Fund on August 20 and redeemed your units on December 7, when the news regarding selling of distressed Amtek bonds came, you would have made a small loss of ₹547. On the other hand, if you had invested ₹1 lakh in India Treasury Fund on August 20 and sold off your units on December 7, you would have actally made a gain of ₹976. The adjacent tables summarise what happened to your money during the course.

Indeed, there are many lessons to be learned from the JPMorgan case and quite a few questions are to be answered. So, while the entire affair may lead to revisiting the way debt funds are managed in India, the good news is that the impact on the JPMorgan investors has been minimal.

Ask Value Research ![]()