Analysts from reputed research firms periodically reiterate their buy or hold recommendations on Reliance Industries. The underlying theme of most of these recommendations is mostly the same. The richest man in the country has some impressive things lined up in the coming years. However, the recent performance of the stock since the division of the empire between two brothers would make even the ardent fans of the company a bit nervous.

The stock has been consistently lagging the S&P BSE Sensex in the last seven years. The difference in the returns of the two has been huge in the last few years. (See table: How they compare?) Looking at the historical data, recent slump in oil prices and the inability of the company to channelise its surplus of ₹379 billion into profitable avenues, investors should be extremely wary of investing in the company.

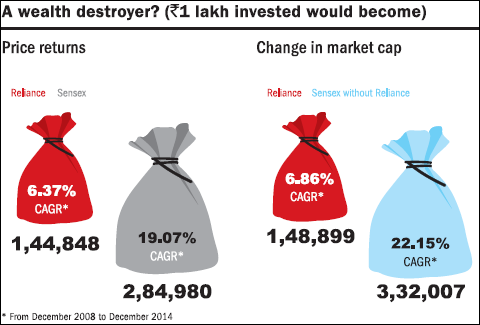

In fact, investors who had bought the stock after the economic turmoil in 2008 barely made single-digit returns. The company has offered an annualized return of 6.37 per cent, which is lower than the inflation rate during the period. Even an investment in the public provident fund (PPF) would have fetched more returns to investors. An investor would have earned ₹1.4 lakh more on an investment of ₹1 lakh in an index fund made in 2008. (See table: A wealth destroyer?)

How they compare?*

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |

| Reliance | 0.7391 | 1.2479 | -0.5679 | 0.771 | -0.0286 | -0.3452 | 0.211 | 0.0664 | -0.0041 |

| Sensex | 0.467 | 0.4715 | -0.5245 | 0.8103 | 0.1743 | -0.2464 | 0.257 | 0.0898 | 0.2989 |

| *Year-on-year return | |||||||||

Ambitious plans

On its 40th AGM (June 18, 2014) Mukesh Ambani announced an expenditure of ₹1.80 lakh crore for the next three years on its petrochemicals, telecom and retail ventures. It will also raise 60,000 debt for these investments, he said. The company is investing close to $16 billion in expanding petrochemical production capacity and to lower feed and fuel costs to boost profits. It is investing $4.6 billion in an integrated gasification combined cycle project that will convert captive petrocoke to synthetic gas (syngas), which can be used to generate power, steam and hydrogen. These are currently being produced using expensive imported LNG.The firm will spend another $1.5 billion to import ethane from the US to replace higher cost propane imports and naphtha, he said, adding that all these projects will be completed by FY18.

That means that we will have to wait for a few years to see the impact of these investments on the company. The immediate impact will be felt on the return on equity, though. Reliance's return on equity is mediocre at 11.92 per cent after tax. It has been falling consistently for the last five years.

Freely falling numbers

In fact, all key numbers have been failing the company in the last few years. Analysts used to point towards its impressive track record of growth in net sales (23.50 per cent in the last five years) until recently. However, it plunged to a single digit in 2014. The operating profits have shown an annualised growth of a lowly 2.57 per cent in the last three years. Net profits have shown an annualised growth of only 5.37 per cent in the last three years. The EPS over the last five years has grown by only 1.69 per cent in the last three years. The operating margin of 19.50 per cent before the demerger has now almost halved to 9.81 per cent. The net profit margin has also more than halved to 5.05 per cent from 10.35 per cent.

Reliance derives more than 95 per cent of its revenues from the oil refining and petrochemicals segment. These two segments contribute about 92 per cent of its operating profits. The margins on refining, which contribute about 50 per cent of operating profits have slumped below 5 per cent since 2009 from above 10 per cent. The margins of the petrochemical division have remained stable at 9 per cent. Its overdependence on petrochemicals could be a cause for concern. Intense competition from global players may make matters difficult for the company.

Can all these adverse factors be softened by Reliance's ambitious 4G foray or by its retail business, which has hit profits after seven years?

Ask Value Research ![]()