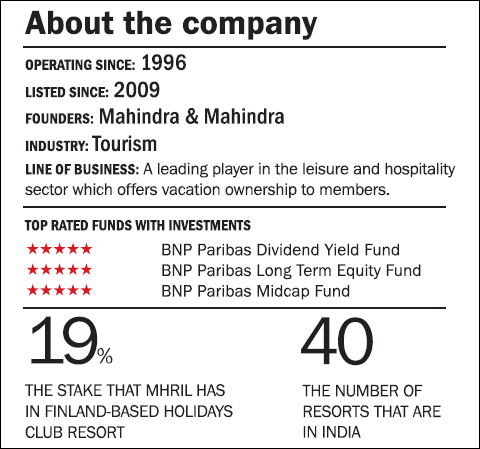

Mahindra Holidays & Resorts India (MHRIL) is into the leisure and hospitality sector which offers vacation ownership. The company operates with its flagship brand 'Club Mahindra Holidays' and other brands like 'Club Mahindra Fundays' and 'Club Mahindra Traveland'. The company has a customer base of 11.7 lakh and owns 40 resorts across India and abroad.

MHRIL offers vacation ownership (VO) to its customers who pay an upfront amount to stay in their resorts for the next 25 years or as per the plan they opt for. For the astute holiday traveller, this option works well because it saves them from the increasing cost of holiday stay in future. Moreover, with the MHRIL resorts spread across the country; they can decide a holiday depending on the available resort in the vicinity.

For the company, this VO model ensures that upfront they get a sum that starts at ₹2.5 lakh, which goes as investments into new resort locations and expansion. MHRIL recognises admission fees as income in the current year and then an entitlement fee, which is recognised as income that is equated over the tenure of the membership. Until such time, income is considered as deferred revenue in the balance sheet of the company.

Strength

MHRIL's biggest strength is its business model. The company raises the capital from its customers to develop and expand resorts and properties. By doing this, it saves itself from relying heavily on debt and hence improves its margins due to absence of interest costs. In this way, MHRIL derives a financial advantage over real estate and hotel companies where they have to rely on taking debt, which proves expensive in the long run.

Brand Mahindra and the parent Mahindra & Mahindra exude confidence among members who are willing to upfront shell out a fee for a VO over the next 25 years. The trust factor is strengthened by the experience that MHRIL offers and the faith that has built over the years about the safety of one's membership benefits.

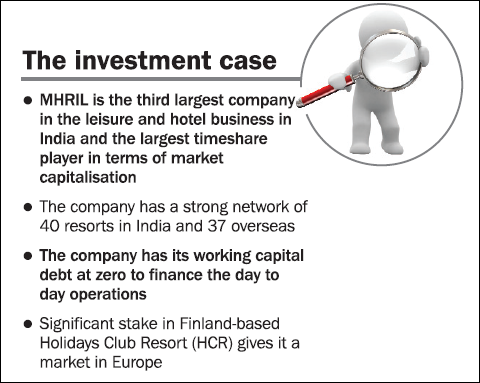

MHRIL is the third largest company in the leisure and hotel business in India. It is also the largest timeshare player in terms of market capitalisation and revenue among the listed companies in this space. Moreover, with its strong network of 40 resorts in India and 37 overseas; the company has a wide choice for customers to pick from. These factors make MHRIL preferred over other players in the segment, which was reflected in its occupancy ratio in the last quarter which stood at 88 per cent, which bodes a healthy sign.

Growth Drivers

With a 19 per cent stake in Finland-based Holidays Club Resort (HCR) for 13 million Euros (₹110 crore); MHRIL is spreading its operations. Moreover, the company has the right to increase its stake n HCR over the next two years. What it gets in return is a strong 50,000 VO members that HCR along with its 32 resorts of which 24 are situated in Finland, 2 in Sweden and 6 in Spain. In a single stroke MHRIL has access the European markets and will become largest VOS outside the US.

The changing dynamics of rising income and lifestyles among Indians is resulting in more people opting for leisure time and travel. Travel destinations are also finding easy access with improved airline-footprint, active communities discussing travel and leisure destinations on the Internet. Although new memberships has slowed down in the past few quarters, it is likely to get a push from the company's new marketing strategy of family referral system. Besides, the company is adding to its room capacity and according to the management, plans are on anvil to add around 500-600 rooms in next 18 months with capital expenditure of around Rs 400 crore. However, the expansion plan has been slow to takeoff.

Concerns

From the upfront payment made by a member, the admission fee is considered as income in the current year and rest of the entitlement fee is carried forward as deferred revenue for the future years. The admission fee amounts to almost 60 per cent of the upfront payment received and therefore revenue recognition model becomes a little aggressive. But the company argues that major expense are sales related expenses and the same are incurred in the current year, when members join.

However, the big concern is over dwindling addition of new members, which has gone down in the past few quarters. In Q1FY15 the company added only 2,059 new members which was low compared to previous quarters. Other than member additions, capacity expansion plans to add more room has also been on a slow pace. Therefore, the company is not able to reap the benefits in the peak season when the bookings are usually full. As more inventory means more revenue from sales to non members during the peak season. Further, margins have taken a hit in the last few years due to factors like low inventory, rise in maintenance cost and increase in selling and marketing costs.

Financials

MHRIL has a deferred income of ₹1,390 crore which will contribute to its future revenue earnings. The company is virtually a debt free and drives it capital expenditure from advances paid by customers. Revenues have grown at an annualised 15 per cent over the last 5 years but earnings per share has fallen by 3 per cent. Also the return on equity has fallen to 13 per cent in FY14 from 47 per cent in FY09, due to the low net worth base then. MHRIL has consistently generated positive cash flow from operating activities, which has helped it keep the working capital debt at zero to finance the day to day operations.

Valuations

At the current price level, the company is trading at price to book value of 3.28 which is 37 per cent discount to the 5-year average of 5.23. No doubt the stock is undervalued in contrast to the overall market scenario but this is due to fall in the pace of earning growth. The realisation of the stock is solely dependent on the revival in the membership additions and speedy additions of capacity. Invest only if you already have a well diversified portfolio as investment in this stock needs a high risk appetite.

This article was originally published on November 11, 2014.

Ask Value Research ![]()