Powered by

Investors' Hangout | 24-Apr-2026

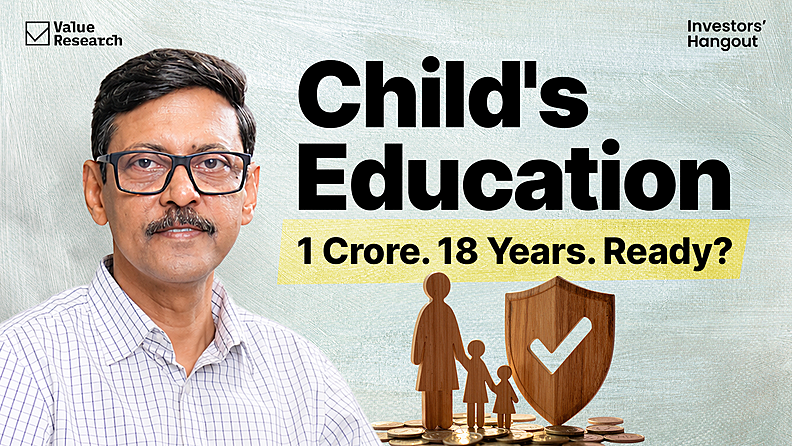

You invest Rs 30 lakh. The market adds Rs 70 lakh.

Rs 14,000 a month for 18 years builds a one crore education fund. Here is how the math actually works.

Your child's college admission is 17 or 18 years away. But the number that will matter most on that day is being decided right now, by what you do or don't do this month.

One crore rupees is the target this video sets for a private college degree, 17 to 18 years from now. If that sounds large, consider that a private engineering degree already costs between 15 and 30 lakh today. If you want to see how this compounds across different monthly amounts and time horizons with real SIP calculations, this step-by-step guide to investing for your child's education is the clearest place to start.

Most parents with a young child carry a quiet, persistent worry: they know education is expensive, they know it is getting more expensive every year, but they cannot pin down a specific number and a specific monthly action. The number keeps shifting, the years keep passing, and the conversation keeps getting postponed. This episode of Investors Hangout, hosted by Aditya Birla Sun Life Mutual Fund and Value Research, gives you the exact figure, the exact monthly investment, and a fund selection simple enough to set up the same night.

Dhirendra Kumar opens with a number that surprises even parents who think they have been paying attention: private education inflation in India runs at 10 to 12 per cent every year, roughly twice the general rate of inflation. A degree that costs 15 to 30 lakh today will cost somewhere between one crore and one crore forty lakh eighteen years from now. The target is not arbitrary. It is built on a specific assumption: 12 per cent annualised returns from equity over a long period.

The video then walks through the three things every parent needs to know. First, the monthly number: Rs 14,000 in a SIP, held for 18 years, at a 12 per cent return, builds one crore rupees. Your contribution across those 18 years is 30 lakh. The market contributes the other 70 lakh. Second, the fund: start with one flexi cap fund. If you want two, add a large-cap index fund. Third, the exit strategy: with three years left before college, allocate the first year's expected expenses to a fixed-income fund. Leave the rest in equity until it is needed.

Dhirendra also names the three mistakes that quietly destroy education funds: starting late, stopping the SIP after the first market fall, and raiding the corpus just because is available. The discipline of not touching the money is, in his words, more important than the choice of fund.

The Numbers Behind the One Crore Target

Private education inflation in India runs at 10 to 12 per cent a year. That is roughly twice the rate of general inflation. Most parents discover this number at the worst possible moment: when the college fee letter arrives.

A private engineering degree in India today costs between 30 and 50 lakh rupees. For study abroad, the cost is already at one crore or higher, and that figure is not unusual. At 10 to 12 per cent annual inflation over 18 years, a degree that costs 15 to 30 lakh today becomes one crore to one crore forty lakh by the time your child is ready to apply. This is the number the plan is built around. It is an assumption, like all financial projections. Your child may get into a government college. The cost may be lower. But Dhirendra's reasoning is direct: this is a non-negotiable expense, one you cannot negotiate down at the last moment, so it is better to err on the side of a larger target than a smaller one.

The antidote to rising education costs is compounding over a long period. If you invest Rs 14,000 every month for 18 years in an equity fund earning 12 per cent, you put in 30 lakh rupees across that time. The market adds 70 lakh on top. That is 70 per cent of the final corpus coming from returns, not from your pocket. The ratio is not magic. It is the direct consequence of starting early and not touching the money. For parents who find it helpful to understand how the SIP calculator works with specific time horizons and return assumptions, running these numbers for your own situation takes less than 2 minutes.

If 14,000 a month is more than you can spare today, the answer is not to wait. Start with whatever you can, increase it every year as your income grows, and treat the corpus as untouchable. The compounding begins the moment the first unit is purchased.

Which Funds to Use and How to Set It Up Tonight

The fund choice matters less than the behaviour. Dhirendra makes this point several times, and it is worth sitting with. The difference in corpus between a great flexi-cap fund and a good multi-cap fund over 18 years is somewhere between 85 lakh and 1 crore 10 lakh. You do not know in advance which will be which. It is, as he puts it, entirely a matter of chance. So do not let fund selection become a reason to delay.

Start with one flexi cap fund. A flexi cap fund is an equity mutual fund that can invest across large, mid, and small companies without being restricted to any one category. This flexibility means the fund manager can move toward safety when markets are expensive and toward growth when they are cheap. It is a sensible single vehicle for a goal 18 years away. If you want a two-fund setup, add one large-cap index fund for stability. That combination gives you diversification across the market without requiring you to constantly monitor or rebalance.

The most important mechanical step is automation. Set up a UPI mandate. Give the standing instruction. Let the deduction happen every month without you having to decide to do it. The ability to automate is what actually builds the corpus. The SIP will run whether the market is up or down, and that consistency across all conditions is exactly where long-term returns come from. Do not look at the portfolio for the first three years. If you start looking in year one or year two, you will find a market decline or a stretch of flat returns that can feel discouraging. Every 18-year SIP goes through several such phases. Surviving the first one is what makes the rest possible.

How to Protect the Corpus in the Final Three Years

You spend 15 years building equity. Then, in the three years before your child enters college, the risk profile changes. The market is volatile in the short run, and you cannot let your child's first-year fees depend on whether the Nifty has a good week.

Dhirendra's framework here is simple. About 2 to 3 years before college begins, allocate 1/4 of the corpus to a fixed-income fund. That one-quarter represents the first year of college expenses. Keep the rest in equity. As each college year approaches, shift that year's expenses out of equity and into fixed income or a short-duration debt fund. The principle is: equity for the long stretch, and debt for the money you will need soon.

This is not a call to exit equity nervously when markets look uncertain. It is a scheduled transition tied to time, not to emotion. The corpus for year four of college stays in equity until year one is nearly over. You get the growth for as long as the time horizon permits it. For a practical breakdown of how to estimate future education costs and manage the transition from equity to debt across different ages, that article covers the full framework in one place.

The Three Mistakes That Destroy Education Funds

Thousands of parents start an education SIP. Fewer than you would expect actually use the corpus for education. Three patterns account for most of the failures.

The first is postponing the start. The reasoning sounds sensible each time: next month, when the salary hike comes, after the home loan EMI reduces, once things settle down. But each year of delay forces a higher monthly SIP for the same target, or a lower corpus for the same contribution. If you cannot get started any other way, Dhirendra suggests a specific trigger: do it on the child's birthday, using the gift money that arrives from relatives and grandparents. Give the fund a beginning, even a small one.

The second mistake is stopping the SIP after the first market fall. New investors almost always experience a fall within the first two years. The returns look poor. Everything feels wrong. This is precisely the moment when stopping the SIP costs the most, because the units being accumulated during a fall are the ones that produce the largest gains when the market recovers. Staying invested through a correction is not blind optimism. It is how the long-term return is actually earned.

The third mistake is raiding the corpus. Eighteen years is a long time. In those 18 years, you will want to buy a house, take a family trip abroad, cover a medical expense, and make a down payment on a car. The accumulated education fund will look like a convenient source of money. It is not. The mental framework Dhirendra recommends is treating it as a fixed obligation, a sum that belongs to your child, not to your present convenience. The corpus is sacrosanct. Every rupee taken out is a rupee that will not compound for the remaining years.

If this video raised questions about your own situation, here is where to go next. The Value Research SIP Calculator lets you run the exact numbers for your monthly amount, time horizon, and expected return in under two minutes: SIP Calculator. The free investment reports cover fund selection and long-term planning in depth: Free Reports. For a broader set of planning tools, including a step-up SIP calculator: All Calculators.

Frequently Asked Questions:

Is one crore rupees a realistic target for a child's college education 18 years from now?

Yes, and for many families, it may actually be a conservative estimate. A private engineering degree in India today costs between 30 and 50 lakh rupees. Private education inflation runs at 10 to 12 per cent annually, roughly twice the rate of general inflation. At that rate, a degree costing 15 to 30 lakh today will cost between one crore and one crore forty lakh in 18 years. For study abroad, the cost is already over one crore today. Planning for one crore is not pessimistic. It is a responsible central case that leaves some room if costs run higher than assumed.

How much do I need to invest each month to build a corpus of one crore for my child's education?

Rs 14,000 per month in a SIP earning 12 per cent annually over 18 years will build approximately Rs 1 crore. Your total contribution across those 18 years is 30 lakh. The market contributes the other 70 lakh through compounding. If 14,000 is more than you can manage today, start with whatever you can and increase it every year as your income grows. The key is to start now. Every year of delay raises the required monthly amount or reduces the final corpus.

Which mutual fund should I use for my child's education SIP?

Start with one flexi cap fund. A flexi cap fund invests across large, mid, and small companies, giving the fund manager flexibility to move across the market without being boxed in. The exact fund matters less than you think. The difference between the best and the good enough over 18 years is smaller than the difference between starting today and waiting six months. If you want two funds, add a large-cap index fund. Set up the SIP via UPI mandate and automate the deduction so it runs without any monthly decision from you.

What should I do with the education corpus three years before college begins?

Start shifting money out of equity and into a fixed-income fund about two to three years before your child enters college. Move approximately one quarter of the corpus at that stage, covering the first year's expected expenses. Keep the rest in equity until each year's fees are approaching. The market is volatile in the short run. Fees are not. You cannot let a market fall in year 17 cancel a year of college in year 18. Equity for the long stretch, fixed income for the money you will need soon: this is the framework.

What if I cannot afford Rs 14,000 a month right now?

Start with whatever amount you can afford today, even if it is much smaller. The compounding that matters most happens over the longest time frame. A smaller SIP started today is worth more than a larger SIP started three years from now. Increase the amount each year, even by a small percentage, in line with your salary growth. The goal is to have something running, earmarked, and untouchable. That mental commitment is more valuable than waiting for the perfect amount.

Why does Dhirendra Kumar say the choice of fund matters less than behaviour?

Over 18 years, a disciplined investor in a good fund will almost always outperform an undisciplined investor in an excellent fund. The difference in corpus between the best flexi cap fund and an equally good multi-cap fund over 18 years is modest. You cannot know in advance which will outperform. But you do know, with certainty, that stopping the SIP during a fall, or withdrawing the corpus early, costs far more than any fund selection error. Behaviour is the dominant variable in a goal this long. The fund is a vehicle. The discipline is the engine.

How is private education inflation different from general inflation in India?

Private education costs in India have been rising at 10 to 12 per cent annually, roughly twice the general rate of inflation. This means a financial plan built around general inflation assumptions will systematically underestimate what a private degree will actually cost. A corpus that looks adequate today may be significantly short at the time of admission. This is why targeting one crore, and erring on the side of caution, makes sense even if your child ultimately attends a college where the cost is lower. If the corpus is larger than needed, the surplus becomes part of your family's wealth.

Disclaimer: This page is based on a video by Dhirendra Kumar, founder of Value Research, who has tracked Indian markets since 1992. Value Research is an independent, SEBI-registered investment research platform. This content reflects the video's analysis and is not a personalised investment recommendation.

Other Videos

PM's Gold Appeal: Should You Sell Your Gold Fund?

15-May-2026 · 10,909 Views

Retirement Corpus That Beats Inflation Over Time

08-May-2026 · 24,882 Views

Stopping Your SIP to Stay Safe Is Your Costliest Move

01-May-2026 · 41,387 Views

3-Star Fund? Selling Won't Protect You

17-Apr-2026 · 10,007 Views

Where to Park Your Money After Selling a House

10-Apr-2026 · 48,651 Views

Why Gold Failed Its Biggest Test

03-Apr-2026 · 15,211 Views

3 Things to Do Before April 1

27-Mar-2026 · 52,437 Views

SEBI's New Rules: What They Mean For You

20-Mar-2026 · 46,526 Views

War, Wealth & What To Do

13-Mar-2026 · 30,325 Views

Women & Wealth: Why Earning Isn't Enough

06-Mar-2026 · 10,288 Views

Multi-Asset or Aggressive Hybrid: Which One Fits You?

27-Feb-2026 · 19,660 Views

SWP & Bucket Strategy for Retirement

20-Feb-2026 · 39,037 Views

NPS Changes 2026: Annuity Escape & Tax Benefits

13-Feb-2026 · 21,952 Views

CAGR vs XIRR vs Rolling Returns: Which Matters?

06-Feb-2026 · 22,275 Views

Union Budget 2026: Investor Checklist

01-Feb-2026 · 15,311 Views

Is ₹5 crore enough for your retirement?

23-Jan-2026 · 31,153 Views