Servicing the lower-end of the housing finance market by focusing on rural and semi-urban areas of the country, Gruh Finance commenced its operation in 1988 from Ahmedabad. The foundation of the company was laid in 1986 when it was promoted by HDFC and the Aga Khan Fund for Economic Development in July 1986.

The company gets majority (75 per cent) of its business from the states of Gujarat and Maharashtra. Gruh has a retail network of 130 offices across seven states in the country.

It has four housing finance schemes – Gruh Suraksha, Gruh Suvidha, Gruh Sajavat and Gruh Samruddhi that cover home loans for salaried, professional and self-employed, loans for repair and maintenance of houses and finance for commercial properties like offices for professionals.

Strengths

The company's board has enriching experience and expertise of HDFC; its parent company which has experience in housing finance for over 36 years. The company is headed by Keki M Mistry, who is also the Vice Chairman and CEO of HDFC.

• The company's asset quality is one of its key strengths – its gross non-performing assets (NPA) is just 0.53 per cent and net NPA is nil as it has maintained 100 per cent provisions for it. Gruh Finance's low NPA is appreciable with the kind of market segment it operates in, which is mostly rural and semi-urban areas where the loan size is typically low

• Gruh's operation in rural and semi-urban areas gives it a competitive advantage as competition is less among the NBFCs here and interest rates sensitivity is less because loan amounts are generally small and effective interest rates are low due to tax benefits of up to 2.5 lakh per annum. These factors give the company a good margin as it is able to pass on the rise in borrowing cost

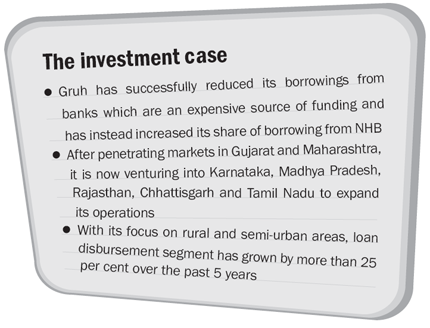

• Over the years, Gruh Finance has been successfully able to change its funding style and reduce its borrowing cost. It has reduced borrowings from banks which were an expensive source of funding and has increased its share of borrowing from National Housing Bank (NHB), up 49 per cent in FY12 from 17.4 per cent in FY07

Growth drivers

The company can leverage upon the various housing schemes which are promoted by the government. Like the Golden Jubilee Rural housing Scheme of the Government of India under which Gruh has disbursed Rs 528 crore during FY12. The National Housing Bank (NHB) scheme called the Rural Housing Fund – 2008 (RHF) for the families falling under the weaker section category. In FY12, Gruh claimed Rs 162 crore covering 3,922 families under the schemes.

• The home loan penetration in India is quite low – at around 7 per cent of the GDP – which is lowest among the developing countries. The demographic growth in India, coupled with rising income level in rural areas, further translate it into a huge opportunity. The company's focus on rural, tier II and tier III cities is right in direction for capitalising this opportunity

• Gruh can witness a surge in housing finance demand as the government has also been promoting it. This is evident from the Budget 2012-13, where exemptions were given from service tax for construction of low cost housing and the investment-linked deduction of capital expenditure on low cost housing was increased. The budget also increased the permitted External Commercial Borrowings (ECBs) for low cost housing

• The company has its operations mainly in Gujarat and Maharashtra that account for almost 75 per cent of its loans disbursement. After penetrating these market, the company is now venturing into new states such as Karnataka, Madhya Pradesh, Rajasthan, Chhattisgarh and Tamil Nadu where it can significantly expand its operations

Concerns

Gruh operates in rural areas and the average loan size per unit is low at Rs 7.53 lakh. Therefore, it escalates the servicing of loans like collection costs. Also, the company faces competition from local co-operative and public sector banks since banks like SBI operate on a larger scale and have a wider reach. The PSU banks have always had a significant market share in these areas.

• The cost of borrowing has gone up to 9.93 per cent in FY12 as compared to 7.89 per cent in FY10. Although return on loans has also gone up to 13.14 per cent from 12.14 in the same period, it has been not enough to maintain the interest spread and therefore, pushing it down from 4.25 per cent in FY10 to 3.21 per cent in FY12

• The housing finance schemes for individuals is a sensitive topic for the government and hence accustomed to adhere to dynamic polices which are very strict in nature. Any adverse changes in these policies by government to lure the public can impact the margins of the company and industry

Financials

The loan disbursement segment has grown more than 25 per cent over the past 5 years. Gruh has maintained its balance and achieved a growth of 28 per cent in net interest income over the same period. Total loan book as on December 2012 stands at Rs 5,003 crore, which grew 33 per cent over last year. The company has improved its capital adequacy ratio to 13.95 per cent in FY12 as compared to 13.32 per cent which was earlier a concern as it was declining in the past. NIMs at 4.6 per cent and return on assets of 3.20 per cent is one of the best among peers.

Valuations

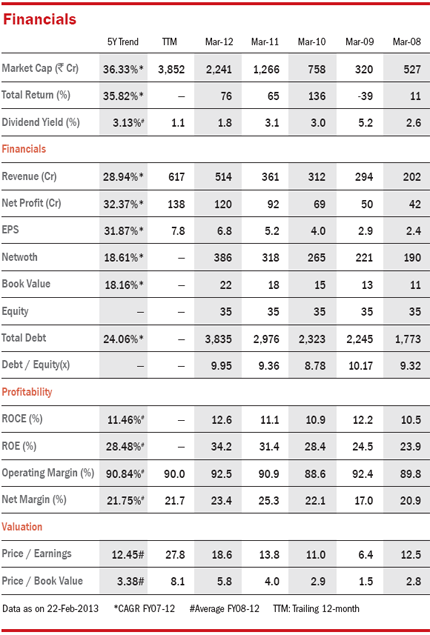

At current price of Rs 216, the stock is trading at price to book value of 8.08 which considerably higher than its five-year average of 4.30. Hence, it is not a value stock. But given the strength and growth drivers of the company, it has the growth potential. So hold it for the long-term. Accumulate more at lower valuations.

This article was originally published on April 17, 2013.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()