“Value” is one of the most overused words in investing. At its core, though, value investing is a straightforward idea, identifying companies trading below their intrinsic worth. Investors typically rely on familiar metrics like price-to-earnings (P/E), price-to-book (P/B) or the PEG ratio to spot such opportunities.

The underlying bet is that markets are inefficient in the short term but rational over time. Prices may deviate from fundamentals, but sooner or later, they converge. That process, commonly known as mean reversion, is what unlocks returns for patient value investors.

From Graham to Buffett, and beyond

Value investing built its roots with Benjamin Graham, who preached the virtues of a “margin of safety”, buying a dollar for 50 cents. Warren Buffett evolved the philosophy further by looking beyond cheapness to strong businesses. He sought companies with durable moats, capable management and predictable earnings.

Over the decades, the philosophy evolved from buying “cheap” stocks to identifying sustainable businesses trading below fair value. Indian investors, too, have shown an enduring fondness for low P/E names, a reflection of their instinctive belief that value eventually asserts itself.

The trap behind cheapness

Not all low-priced stocks are bargains. Even the seasoned investor sometimes faces the value trap: a stock that looks cheap but stays that way. Investors buy expecting a P/E rerating, only to be stuck with businesses that remain perpetually undervalued. The trap usually springs when low valuations mask deeper issues: weak earnings, high debt, poor cash flows, or governance lapses.

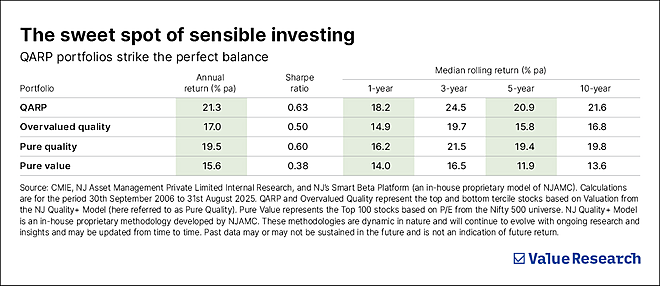

The data tells a clear story. When investors focus solely on low valuations and ignore quality, the results can be damaging. These ‘value traps’ generally exhibit higher volatility, steeper drawdowns, and a higher probability of loss.

The message is clear: buying cheap stocks without examining quality is like catching falling knives—statistically defensible, but painful.

Why quality is the new margin of safety

Quality is the antidote to the value trap. Businesses with sound balance sheets, steady cash flows, prudent capital allocation and transparent governance avoid the pitfalls that plague low-quality peers. These traits don’t just reduce risk; they enhance compounding.

But quality doesn’t usually come cheap. The higher price tag is the market’s way of saying these businesses can last. Paying up for such reliability is like paying an insurance premium for peace of mind. In today’s markets, value investing without a quality lens feels incomplete. Price matters, but context matters more.

Enter QARP: Where value meets quality

The modern answer to traditional value investing is QARP (quality at a reasonable price), an approach to identifying strong businesses available at fair or modestly discounted valuations. QARP avoids both extremes, overpriced quality stocks that test patience and “broken” value stocks that test nerves. It focuses on balance, the intersection where fundamental strength meets valuation discipline.

Data support this evolution. Portfolios that blend quality and value consistently deliver superior risk-adjusted returns. The QARP quadrant, low valuation and high quality, has historically outperformed its peers, offering better compounding and lower drawdowns.

In practice, QARP investors aren’t bargain hunters; they’re selective pragmatists. They prize financial stability and governance standards as much as they do attractive entry points.

The new definition of value

QARP is value investing upgraded for modern markets, a framework where quality is the new margin of safety. It filters out short-term noise, resists the temptation of “cheap for a reason” stocks, and anchors portfolios in businesses that endure across cycles. It also aligns perfectly with NJ AMC’s philosophy, 100 per cent rule-based, quality-focused investing that seeks undervalued opportunities within a quality universe.

QARP reminds us that the real bargain is not the lowest price, it’s the best value for money.

Nirmay Choksi is the Director and Head of Investment at NJ Asset Management Private Limited. The views expressed above are his own.

Ask Value Research ![]()