AI-generated image

AI-generated image

Mira, a 27-year-old professional earning Rs 50,000 a month, has been saving diligently for the past two years. With Rs 5 lakh sitting idle in her bank account, she's been contemplating when to start her investment journey. For months, she has watched the stock market surge, but just as she was about to take the plunge, the market took a slight dip from its highs. Now, with the Sensex hovering around 82,000, down from its recent peak of 86,000, Mira wonders whether this is the right time to invest.

With this dip in the market, she feels that maybe she shouldn't wait any longer. But should a small correction like this be the deciding factor?

There's no perfect moment, just the right approach

While the current market levels may seem tempting, market fluctuations are normal. Whether the Sensex is up or down by a few percentage points, Mira's most crucial decision is to start investing and not wait for the elusive "perfect time".

The key is not to invest the entire Rs 5 lakh at once, but to enter the market gradually. A systematic approach like a systematic investment plan (SIP) is ideal, especially when market levels fluctuate. With SIPs, Mira can invest a fixed amount every month, smoothing out her entry point over time and reducing the impact of market volatility.

Investing through SIPs not only takes the guesswork out of market timing but also allows her to benefit from market dips along the way. The time in the market is more important than trying to time the market.

Data shows that delaying investments by just five years can reduce your final corpus tremendously. For instance, starting an SIP at age 27 with an investment of Rs 5,000 per month could lead to a corpus of approximately Rs 1.76 crore after 30 years, assuming a 12 per cent annual return. However, if you delay by five years and start at 32, the corpus could shrink to around Rs 82 lakh. That's a huge difference of roughly 94 lakh.

Mira's roadmap to smart investing

Before Mira jumps in, she needs to identify her financial goals. Is she saving for a short-term objective like a vacation or a long-term goal such as retirement? Once she identifies her goals, she can select the right investment options.

For short-term goals (three to five years), safer investment options like short-term debt funds are a better fit, whereas for long-term wealth building (over five years), a diversified portfolio of equity funds will deliver better returns. Just to reiterate, Mira should use SIPs to enter the market gradually, rather than make a lump-sum investment.

Hybrid funds for beginners

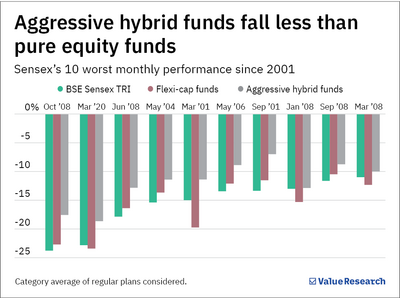

Since Mira is a first-time investor, she is hesitant to invest entirely in equity funds. A good starting point could be aggressive hybrid funds, which invest in both equities and debt. These funds offer exposure to stock market growth while cushioning the portfolio with stable debt assets. As a result, aggressive hybrid funds tend to fall less during market corrections, providing peace of mind to new investors like Mira.

Performance-wise, an average aggressive hybrid fund has returned over 15 per cent (SIP returns) in the last 10 years. If Mira's already accumulated money of Rs 5 lakh is meant for the long run, she can deploy this amount in aggressive hybrid funds across the next 12 to 18 months through an SIP. By doing so, she can reduce the risk of entering the market at a high point and benefit from rupee cost averaging. (For the uninitiated, rupee cost averaging helps you buy more units when prices are low and fewer when prices are high, helping to reduce the average cost of your investments over time.)

Riding out the market noise

Despite the slight dip in the Sensex from 86,000 to 82,000, Mira should remember that short-term market movements are unpredictable. Over a period of 10 years, the Sensex has delivered an average annual return of around 14 per cent, despite corrections. This shows that the market tends to reward investors who stay invested over the long term.

By investing regularly through SIPs and focusing on long-term goals, Mira can ride out market volatility without the stress of trying to predict daily movements.

Building a solid foundation

Before Mira begins her investment journey, it's essential that she takes care of a few financial basics:

- Emergency fund: She should set aside six months' worth of living expenses in a liquid fund or a sweep-in deposit.

- Life insurance: If Mira has financial dependents, she should get a pure term life insurance policy.

- Health insurance: Along with the policy provided by her employer, Mira should also have her own health cover.

Also read: How to retire at 45

This article was originally published on October 14, 2024.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()