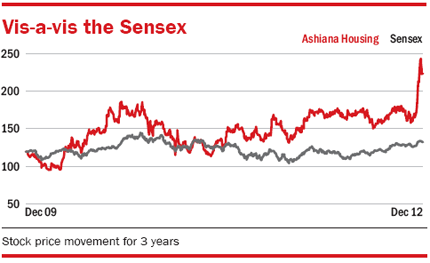

Ashiana Housing is a realty player unlike its peers. It does not build in any of the top cities – in fact, it consciously avoids them. Ashiana has no debt, is cash flow positive and its RoCE at 40 per cent during the last three years is the highest among its peers. First recommended in our August 2011 issue, Ashiana has gained nearly 50 per cent since our buy call.

Why you should buy Ashiana Housing?

Focus on tier II and III cities: Ashiana has focused on cities such as Bhiwadi, Jaipur, Jamshedpur, Halol (Gujarat) and Patna. Typically, the company has invested in towns that are developing into industrial hubs and those that are turning into IT hubs such as Ahmedabad, Jaipur, Nagpur, Nasik, Raipur and Vadodara.

Mid-income housing gains: Rather than going after the crème de la crème, it focuses on mid-income housing projects with a typical ticket size of Rs 25-45 lakh.

Projects awaiting clearances: Ashiana has 9.6 million sq ft lined up for development but is waiting government clearances for most of them. In Rajasthan alone it is waiting for clearances for 7.8 million sq ft. Such delays are expected to take a toll on the company's topline.

Bookings to pickup in FY14: Bookings are expected to gain momentum in FY14 with the company's 3.6 million sq ft project in Bhiwadi and two others in Uttarpara (West Bengal) and Halol expected to come up by H2FY14.

Lavasa legacy: The Ministry of Environment stopped all construction in Lavasa in November 2010. It eventually allowed construction in Q4FY12 and Ashiana's bookings at its old-age retirement community it is building in Lavasa have slowly picked up.

Future growth drivers: With cash of Rs 104 crore (September 2012), the company is looking at Bengaluru, Chennai, Haryana, Hyderabad and Pune for land deals.

Strong cash flows: Cash flows from bookings in current projects are expected to remain robust at between Rs 70-80 crore (CRISIL estimates) during the next 2-3 years.

Change in accounting: Ashiana changed its accounting methodology from percentage-completed to the more accurate possession-based with effect from April 2012. As a result, topline and PAT for the next two years are expected to decline (from FY12 levels) even though cash flows are expected to remain strong during this period.

Ebitda margin expansion: Ashiana's Ebitda margins are expected to expand by as much as 3.6 per cent over the next three years as contribution of high-margin projects like those of Rangoli Gardens, Jaipur and Utsav, Lavasa take centre-stage. On a NAV basis, Ashiana's fair value is estimated at Rs 256 per share (CRISIL estimates). At the CMP of Rs 220, there is still some value left and the stock trades at a very reasonable 6.4 times its ttm earnings. Buy with a 5-year horizon.

This article was originally published on January 30, 2013.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()