AI-generated image

AI-generated image

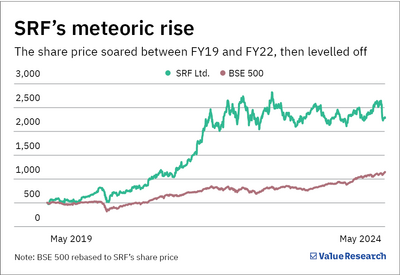

During the Covid pandemic, the Indian chemical industry found itself like a runner at the starting line. Supply chain disruptions from China created unprecedented opportunities, and Indian companies were ready to surge ahead. Leading the race was SRF Limited , which emerged as the largest chemical company in India by market capitalisation. SRF became a Dalal Street favourite. Between FY20-23, its share price jumped nearly 5.6 times, peaking at a valuation of Rs 83,779 crore in September 2022.

However, FY24 brought the gains to a halt. SRF's revenue and profit after tax declined 12 per cent and 38 per cent year-over-year (YoY), respectively, during the year. Its share price declined 9.2 per cent (as of May 27, 2024).

SRF's financial performance

Profitability took a plunge in FY24

| FY24 | FY23 | FY22 | FY21 | FY20 | FY19 | |

|---|---|---|---|---|---|---|

| Revenue (Rs cr) | 12,910 | 14,870 | 12,434 | 8,400 | 7,209 | 7,100 |

| Operating profit (Rs cr) | 1,911 | 2,954 | 2,586 | 1,680 | 1,066 | 939 |

| CFO (Rs cr) | 2,094 | 2,902 | 2,106 | 1,772 | 1,304 | 896 |

| EBIT (%) | 14.8 | 19.9 | 20.8 | 20 | 14.8 | 13.2 |

| ROE (%) | 12 | 22.9 | 24.5 | 20.3 | 20.2 | 15.4 |

|

CFO is cash flow from operations EBIT is earnings before interest and taxes ROE is return on equity |

||||||

The reason? Inventory dumping by Chinese competitors in its chemicals segment and heated domestic competition in packaging. Let's delve deeper.

-

The packaging segment

SRF manufactures plastic-based BOPP and BOPET films, which are widely used in the packaging industry. This segment saw significant growth during the pandemic due to increased demand for FMCG and pharma packaging products. The business' operating profit margins touched a record high of 27.3 per cent in FY21 and the operating profit jumped 61 per cent in the same period.

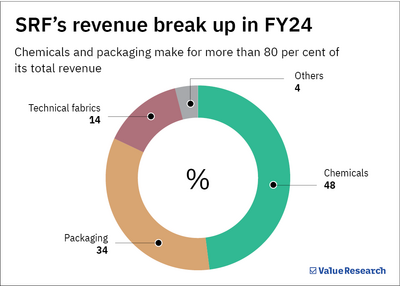

However, the entry of multiple new competitors domestically led to severe price competition, causing profitability to drop. In FY24, the segment's operating profit margin slumped below 5 per cent, and its share in overall profit was only 9.4 per cent despite a 34 per cent contribution to total revenue. Management expects no major improvement in this segment for at least the next couple of years.

-

The chemicals segment

SRF is the largest manufacturer of fluorine-based refrigerant chemicals in India. It also produces various specialty chemicals for the agriculture and pharmaceutical industries.

However, recently, the company succumbed to reduced demand and aggressive price competition from Chinese suppliers as China's economy reopened post-Covid. These factors led to a 15 per cent yearly contraction in this segment's profits in FY24.

Despite these hurdles, the business contributed 48 per cent to SRF's revenue and 74 per cent to its operating profit in FY24. Additionally, the company maintained an operating profit margin of 25.8 per cent, significantly higher than pre-Covid levels, demonstrating its operational efficiency and strong market position.

Betting on the crown jewel

Despite the blip in FY24, SRF is heavily counting on its core chemical business by pumping in epic proportions of money. In the last three years (FY22-24), it poured Rs 6,853 crore as total capital expenditure, which is almost equal to its operating cash flow generated over this time. Of the committed capex, nearly 80 per cent is meant for the chemicals business. As per management, the capex spree will continue in FY25.

The company has developed the finest quality of H32 gas (a hydrogen-based eco-friendly refrigerant), which is highly sought after in international markets, particularly in developed economies. To enhance its capacity, the company also commissioned a new plant for Rs 1,800 crore.

In the specialty chemicals segment, SRF has made significant strides in production and client acquisition for key intermediates used in the pharma industry. At its Dahej facility, nine dedicated plants will begin production by the end of 2024. Its high-margin agrochemical business has also performed well since FY21, with two new multi-purpose plants commissioned to further scale operations.

Management anticipates recovery in the chemical segment to begin in the second half of FY25 and projects a growth of 20 per cent while maintaining the operating profit margin above 25 per cent.

Will the chemical focus pay off?

SRF's heavy focus on scale over product differentiation could prove risky, given the price threat from competitors in China is far from over. Their large-scale refrigerants and specialty chemicals operations could jeopardise the domestic industry. Any further decline in prices can have a major impact on SRF's financials and profitability, especially considering the poor state of its packaging business. Moreover, the company is currently trading at a hefty valuation of 51.2 times. It remains to be seen whether SRF's aggressive investments will stand as a bulwark against industry headwinds or not.

This is not a stock recommendation. Investors must do their own due diligence before making an investing decision.

Also read: You may gain from this chemical manufacturer despite expensive valuations

Ask Value Research ![]()