An investor in 1992 could make more money in a month by just buying index stocks ahead of the budget than he would have by investing in a fixed deposit for a year. And he could have taken this risk with great success multiple times during that decade.

But no longer.

The Union budget is not what it used to be for equity markets. Wild swings in stock prices as the finance minister speaks to the nation about how the government is going to spend its money have been on the decline.

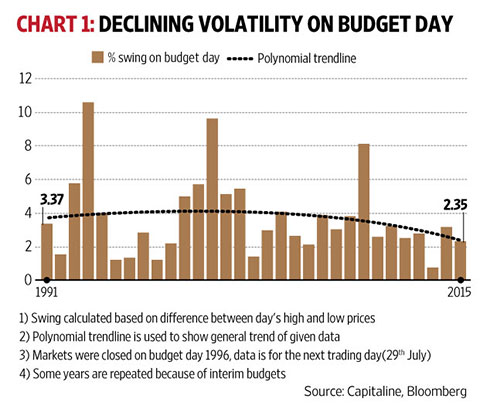

A Mint analysis of 31 budget day movements (including interim budgets) since 1991, the year when liberalisation began, shows that average budget day movement for the Sensex has been trending downwards, perhaps helped by the realization that reforms are not a budget-only phenomenon.

The market moved more than 10% (the difference between the day's high and low for the Sensex) when the government presented the budget in 1993. This was down to 2.35% in 2015. The average budget day move has decreased from 4.2% in the 90s to 3.78% in the subsequent decade, and 2.49% after 2010.

"Recent history shows that the budget is likely to be not an inflexion point for the market but rather another step in the direction of an economic recovery and long-term reform," says an 11 February report from investment bank Morgan Stanley.

Even anticipation of reforms or big-bang announcements seems to be declining. There were multiple occasions in the 90s when investors could have made more than 10% in the single month leading up to the budget. The pre-budget rise was as high as 36.29% in 1992. This was down to 7.37% in the 2000s.

The trend has shown a further downward drift since then. Gains have been limited, and one-month returns have actually been negative in the run-up to every budget since 2007.

Post-budget one-month returns tend to be negative if pre-budget expectations have been positive, especially in recent years. Eight out of 14 instances where market returns were positive before the budget have seen negative returns afterwards. There were positive returns in the one month after the budget eight times out of the 17 times that the Sensex was negative leading up to the budget.

What about the current year?

The Sensex was already down 5.29% by 15 February, making this month leading up to the budget the eighth worst (unless the trend is reversed in the next couple of weeks). This fall is greater than MSCI World (3.73%) and MSCI Emerging Markets (2.09%).

So could the current fall ahead of the budget be seen as a buying opportunity?

An 11 February Bank of America Merrill Lynch Equity Strategy report said that the market offers value even if the budget doesn't make much of a bang.

"While it is most likely impossible to catch the bottom, we believe the ongoing correction provides a good opportunity to add equity in India," said the report, authored by Sanjay Mookim, Anand Kumar and Ashish Kumar. They point out that market multiples are at long-term averages even after accounting for earnings cuts. There are also non-budget tailwinds such as lower lending rates and commodity prices, both of which are expected to help consumption. Implementation of the pay commission will also stimulate demand, they said.

That said many see this as the last budget in which the government can push through serious reforms. Thus, 2016 could be a year which bucks the trend of lower market volatility on budget day, whichever way finance minister Arun Jaitley turns.

In arrangement with HT Syndication | MINT

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()