John Bogle, the late founder of Vanguard and a pioneer in the investing world, is well-known for his advocacy of index funds and passive investing. (This is a style of investing where an investment is merely replicating an index, say the Nifty or the Sensex).

However, he always felt active funds - mutual funds that select stocks or debt instruments based on a fund manager's conviction - were a better option in an emerging economy like India because not everyone has equal access to company data and information in the country.

But given what we found when comparing active large-cap funds with the Nifty, Bogle's exception-to-the-rule may need a revisit... at least in the investing world of blue-chip companies.

Wolf in sheep's clothing

Look at any active large-cap fund. In theory, these funds rely on the fund manager's expertise to select the best large-cap stocks.

But most of them look almost like the Nifty 50 index. In number terms, 18 out of 25 active funds have more than 60 per cent overlap with Nifty 50, with some as high as 75 per cent.

So, if more than half the fund looks like an index, why not just invest in the index?

At this point, you as an investor would ask a simple question to the managers of these active funds: "If you aren't very different from the Nifty, why should I not invest in an index fund instead?"

Existential crisis of a performance

And if you want to look at the active large-cap funds' performance, look away.

We looked at the performance of 25 large-cap active funds over the last five years. To give these funds a fair chance, we looked at multiple aspects, but nothing proved flattering.

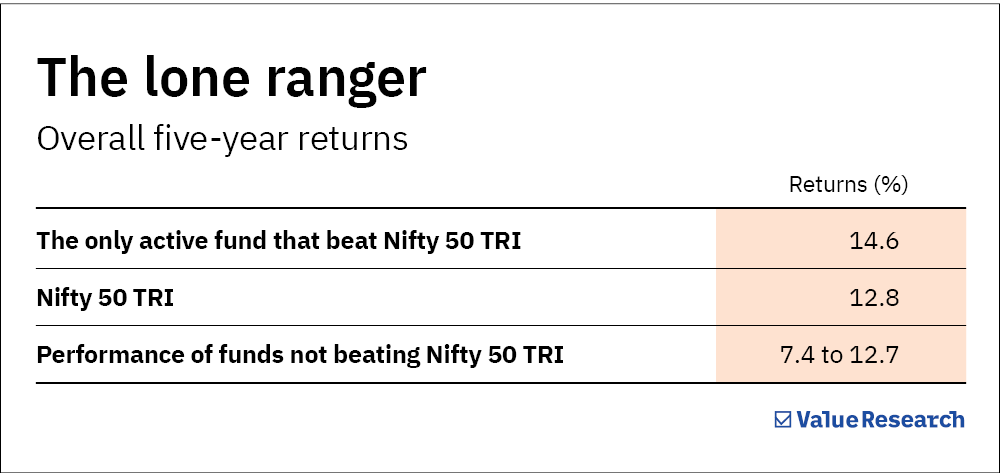

- In the five years from January 1, 2018 to December 31, 2022, only one (yes, just the ONE) active large-cap fund managed to beat the Nifty-50 index's 12.8 per cent returns! In fact, some of them underperformed by a wide margin, as you can see in the table below.

- Even if you look at the individual calendar year performance, only four active funds beat the Nifty in three out of five years. What's sobering is that there were a staggering ten active funds that could beat the index just once in five years.

- Sometimes, in the world of numbers, you can be guilty of slicing and dicing data to fulfil your preconceived notions. But nothing worked in this case.

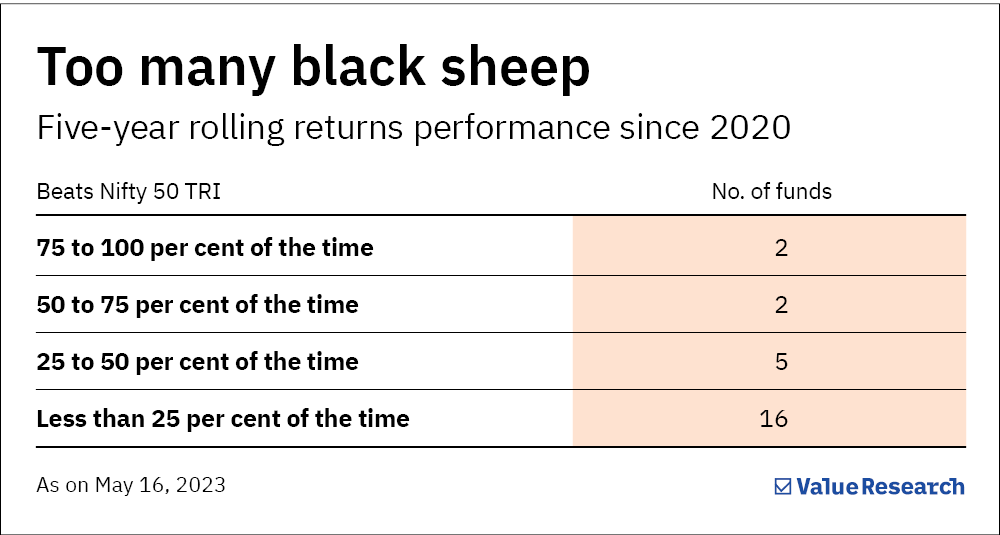

Active funds looked bad in the rolling returns department too. (Rolling returns are indicative of an investment's consistency). Based on five-year rolling returns since 2020, wherein your investment started in 2015, only four active funds were found beating the index majority of the time. Worse still, 16 of the 25 funds could barely beat the index even a quarter of the time.

No bang for buck

The underperformance aside, active funds charge almost 0.8 per cent more than index funds! That makes us wonder why you are paying more to get less.

Moreover, active funds are supposed to filter out low-quality stocks and give better returns, by staying away from questionable companies that either find their way into the index or remain an unwelcome guest long after they turn sour. Companies like Adani, Yes Bank, Reliance Communications and Suzlon Energy come to mind. They all were a drag on the Nifty and took a long time to exit the index, thereby hurting its overall returns. But despite this weakness, the active large-cap funds have failed to capitalise on it.

Our take

The simple conclusion from these numbers is that large-cap active funds have, quite literally, lost the plot. They look increasingly like a passive fund, charge you more and give you lesser returns. As an investor, it may be time to look elsewhere.

Also read: The John Bogle advice index fund fans don't tell you about

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()