The interest rate for senior citizen savings schemes (SCSS) increased from 7.6 per cent to 8 per cent recently, which is good news for the retired on the lookout for assured returns.

SCSS is eligible for everyone above 60. People between 55 and 59 can also put their money in SCSS, provided they have retired voluntarily or with superannuation benefits.

The maximum amount you can invest is Rs 15 lakh. It can go up to Rs 30 lakh if you jointly own the account with your spouse.

A risk-free scheme because the government backs it, SCSS provides a fixed income every three months - on the first working day of April, July, October and January. This gives retirees a regular flow of income.

This scheme also has a five-year lock-in, but that shouldn't alarm you, as your main objective is to remain invested in SCSS for the duration of your retirement years. In fact, you can choose to extend the lock-in period for a further three years.

The only drawback is that the interest earned is taxed as per your tax slab. And if the interest earned is above Rs 50,000 per annum, tax is deducted at source (TDS) itself.

What you should do

- SCSS is a better option than fixed deposit (FD).

- Visit a post office or a public/private bank to open an SCSS account.

- We recommend you invest the maximum permissible amount in SCSS, which is Rs 15 lakh for an individual account and Rs 30 lakh for a joint account with your spouse.

After putting a certain portion of your retirement corpus in SCSS, put the remainder of the money in the following two options:

4 Million+ copies sold! Get investment insights, market guidance, fund analysis, data stories, case studies and more. Subscribe to our digital & print magazine - Mutual Fund Insight.

1. Equity-oriented mutual funds

Investing in equity-oriented schemes in your retirement sounds counterintuitive. But in reality, equity funds have offered strong returns in the long run.

The returns you earn from these funds will help you maintain a rising standard of living during your retirement.

Hence, we suggest you allocate at least 40 per cent of your retirement corpus to an equity-oriented fund, such as a flexi-cap fund. If you want to play it conservatively, opt for a large-cap fund.

To learn more about equity-oriented funds, click here.

2. Short-duration debt mutual funds

Since short-duration debt funds are required to invest in bonds with an average maturity period of one to three years, the impact of rising or falling interest rates is limited.

In other words, these funds' performance is not as severely impacted by interest rate volatility as middle- to long-duration debt funds are.

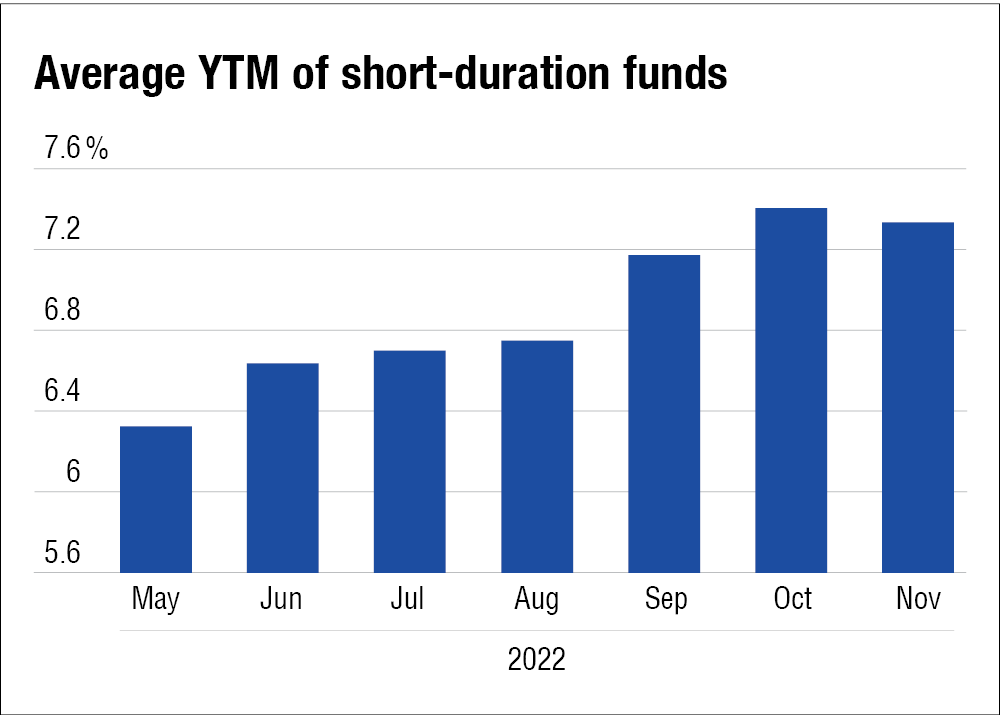

In fact, there is a slight uptick in short-duration funds' yield-to-maturity (YTM) when interest rates rise, as they did in 2022. That's because they can start investing in new bonds with higher yields.

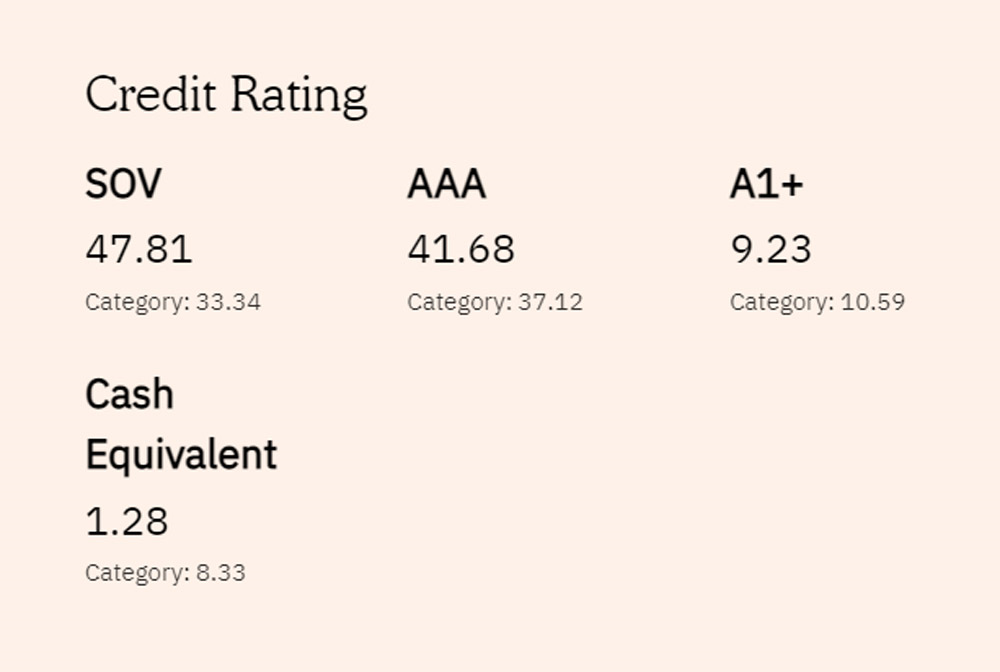

However, don't go by their returns alone when it comes to short-duration funds. Your money's safety is paramount when you invest in debt funds. Hence, ensure these funds have a predominant exposure to high-rated papers.

To assess the risk that your debt fund is taking, type the fund's name in the search bar above. This will open the fund page. Scroll down and click on the 'Portfolio' tab. You will find the break-up of your fund's holdings (see the below screenshot).

Short-duration funds are also liquid, meaning their investors can move out whenever they want.

In terms of taxation, if you hold short-duration funds for less than three years, the capital gains will be added to your income and taxed as per your tax slab. And if you hold the fund for more than three years, you will be taxed at 20 per cent after allowing indexation benefits.

Final thought

To summarise, you should put your retirement corpus in SCSS, equity-oriented funds and short-duration debt funds.

While SCSS can take care of your cash flow needs and short-duration debt funds can preserve your capital by delivering higher returns than a bank savings account, an equity-oriented mutual fund's relatively-higher returns will ensure you don't run out of money in your old age.

Suggested read: Are the new rates applicable to existing SCSS accounts?

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()