Incorporated in 1989, Sigachi Industries is involved in the business of manufacturing Microcrystalline Cellulose (MCC) which is primarily used as a valuable additive for finished dosages in the pharmaceutical industry. MCC is a non-reactive component that is used to manufacture pharmaceutical products without compromising their medicinal properties. At present, the company manufactures MCC in 59 grades - from 15 microns to 250 microns, which not only has its application in the pharma industry but also in several other industries such as food, nutraceuticals, and cosmetic industries. Sigachi Industries has three manufacturing units in total, two units in Gujarat and one in Hyderabad with a total capacity of 12,588 million ton per annum.

Sigachi Industries has also entered into a contract (June 2023) with Gujarat Alkalis & Chemical Ltd (GACL) for operating the manufacturing units owned by GACL. The company has a strong presence in the international market as they export to more than 41 countries such as Australia, the U.S., the U.K., Poland, Italy, etc. As MCC is a critical raw material for pharma products, none of their manufacturing units were shut down during the pandemic, and their products were categorised as 'essential goods'.

The global demand for MCC is expected to increase due to increase in production of pharmaceuticals and packaged foods. The market for MCC is expected to grow at 7.25 per cent to 1.4 billion USD by 2025. As MCC is a raw material, its demand is in direct correlation with demand for pharmaceutical products, which accounts for a significant share in the MCC market. Thus, due to increase in production of pharmaceuticals and increasing application in various industries, MCC manufacturers are expected to benefit globally.

Strengths:

1) Market leader: The company is one of the leading manufacturers of MCC under various grades in India. It also has a strong international presence, exporting to more than 40 countries with 73 per cent of its revenue from exports as of FY2021.

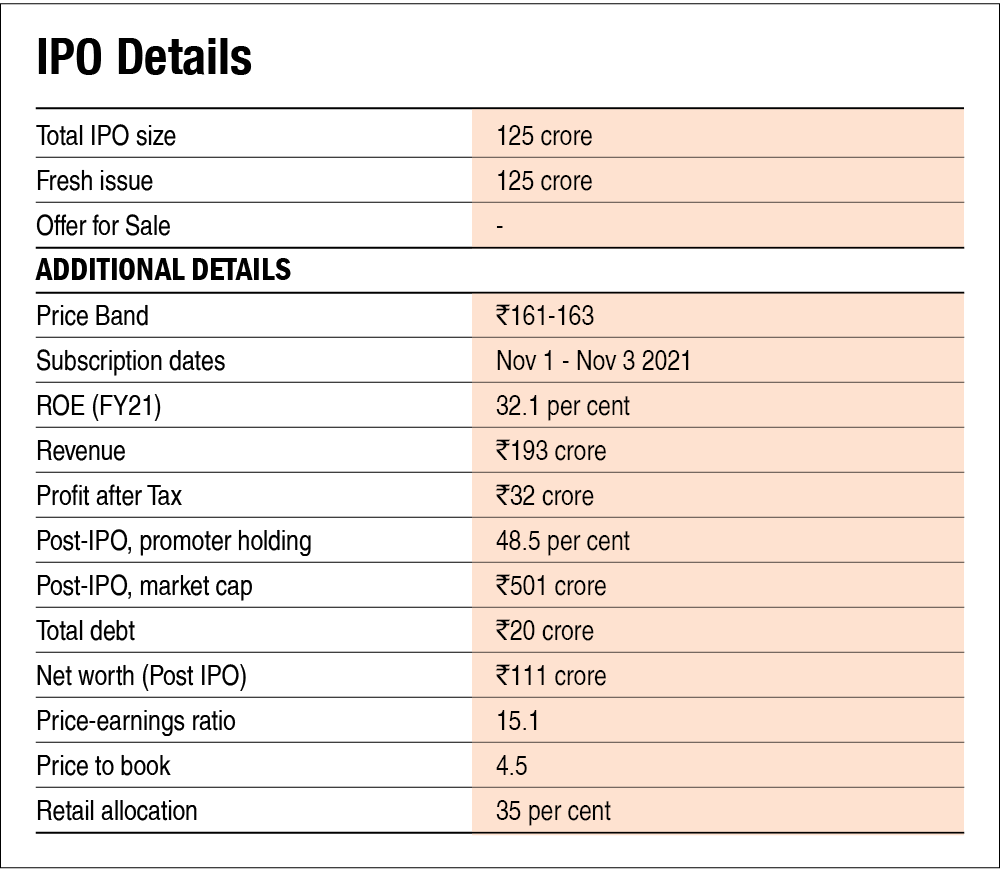

2) Attractive valuation: Post-issue, the company will trade at a P/E of 15 and a P/B of 4.5, which is attractive considering other players in the pharma market.

3) Consistent growth: The company has witnessed strong growth in financials with 22.2 per cent growth in revenue, 18.7 per cent growth in EBITDA, and 26.2 per cent growth in profits from 2019 to 2021.

Weaknesses:

1) Revenue concentration: Around 75 per cent of the company's revenue comes from the pharma industry and around 48 per cent from its top five customers. Any change in the industry or from customers would affect the revenue.

2) Dependence on few suppliers: 66 per cent of total raw materials are sourced from the top five suppliers. Any change in terms of contracts or delay in delivery would affect their production process. They do not have any long-term contracts with suppliers.

3) Huge working capital requirements: The company requires heavy working capital due to its revenue model where it gets revenue only after delivering the product. It has a cash conversion cycle of 88 days.

IPO questions

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

No, the company's earnings before tax for FY21 were Rs 38.5 crore.

2) Will the company be able to scale up its business?

Yes, the company has planned to utilise its proceeds from the issue to increase production capacity. With increased capacity and growing demand, the company should be able to scale up its business.

3) Does the company have recognisable brand/s, truly valued by its customers?

No. The company's products are used as raw materials in various industries. Thus being recognised as a brand in this market is limited.

4) Does the company have high repeat customer usage?

Yes. Even though they do not have any long-term contracts with their customers, they have maintained long-term relationships with many of their customers throughout the years.

5) Does the company have a credible moat?

No. Although the company is a leader in the domestic MCC market, there are other international players who can provide the same product, and the pharma companies themselves can develop the products in-house.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

No. The company gets around 73 per cent of its revenue, as of FY21, from exports and gets a significant portion of its raw materials through imports, so any change in the geopolitical scenario can affect the business.

7) Is the business of the company immune to easy replication by new players?

No, new entrants have to make sufficient spending on manufacturing units and R&D capacity to produce the product, which would be difficult considering that there are already established players in the market.

8) Is the company's product able to withstand being easily substituted or outdated?

Yes, as the product that the company manufactures is a critical raw material for the pharma industry, the product cannot be substituted or outdated.

9) Are the customers of the company devoid of significant bargaining power?

No, the company derives around 48 per cent of its revenue from the top five customers. They will be able to have significant bargaining power when negotiating contracts.

10) Are the suppliers of the company devoid of significant bargaining power?

No, the company sources around 66 per cent of its raw materials from its top five suppliers. Due to the absence of long-term contracts to fix prices, suppliers would be able to have significant bargaining power.

11) Is the level of competition the company faces relatively low?

No, the excipient market is filled with both organised and unorganised players both domestically and internationally.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than a 25 per cent stake in the company?

Yes, the founding members Rabindra Prasad Sinha and Chidambaranathan Shanmuganathan would continue to hold 11.3 per cent stake and promoters as a whole would continue to hold 48.5 per cent stake post-issue.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes, its CEO Amit Raj Sinha has been with the company since 2006, the promoters Rabindra Prasad Sinha and Chidambaranathan Shanmuganathan have been with the company since its inception.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. Although the company has one case related to indirect tax, it does not cast any doubt on the intention of the management.

16) Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17) Is the company free of promoter pledging of its shares?

Yes, the promoters' shares are free of pledging.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and a return on capital of more than 18 per cent?

Yes, the company generated an average of 35.3 per cent return on equity and 38.6 per cent return on capital employed from FY19 to FY21. For FY21, it generated 32.1 per cent return on equity and 37.8 per cent return on capital employed.

19) Was the company's operating cash flow positive during the three years?

Yes, the company has reported positive operating cash flow during the last three years. But they have reported a negative operating cash flow for Q1FY22.

20) Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenue grew at a rate of 22.2 per cent from FY19 to FY21.

21) Is the company's net debt-to-equity ratio less than one or is its interest-coverage ratio more than two?

Yes, the company has a debt-to-equity ratio of 0.24 as of June 2021, and an interest coverage ratio of 31.8 for FY21.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

No. Though the company has a strong cash position, it requires huge working capital due to its revenue model and cash conversion cycle of 88 days.

23) Can the company run its business without relying on external funding in the next three years?

Yes, the company has planned to utilise the proceeds from IPO for capacity expansion. They will not be needing any kind of external financing to run their business.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company's short-term borrowings decreased by 16.9 per cent from FY19 to FY21, but it is to be noted that it increased by 27 per cent from March 2021 to June 2021.

25) Is the company free from meaningful contingent liabilities?

No, the company has contingent liabilities of Rs 6.5 crore, which is 6.3 per cent of its equity, as of June 30, 2021.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock will only offer an operating-earnings yield of 7.9 per cent on its enterprise value.

27) Is the stock's price-to-earnings less than its peers' median level?

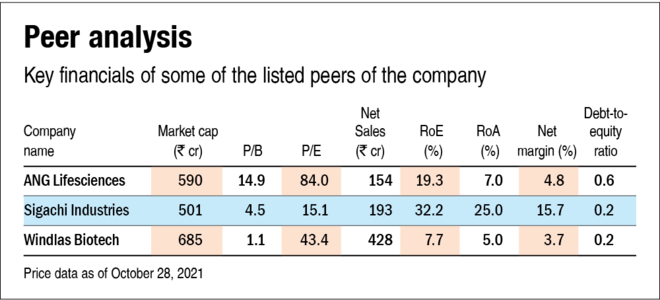

Not applicable. Although no other listed company is engaged in a similar MCC business, ANG Lifesciences and Windlas Biotech are similar players in end-use pharma products and contract manufacturing. Sigachi would trade at a P/E of 15.1 against the Median 63.7 of the other two companies.

28) Is the stock's price-to-book value less than its peers' median level?

Not applicable. Post-IPO, the company's stock will trade at a P/B of around 4.5, while ANG Lifesciences and Windlas Biotech trade at a P/B of 14.9 and 1.1, respectively.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()