Sudeep, a retiree, invested close to Rs 20 lakh in the shuttered schemes of Franklin. Though a small portion of the investment is still pending, he has received most of it. Driven by a safety-first mindset, Sudeep now wants to re-invest the funds for a regular income and wants to know about various available alternatives. Here is how he should go about investing in fixed-income instruments.

Government-backed guaranteed-return schemes

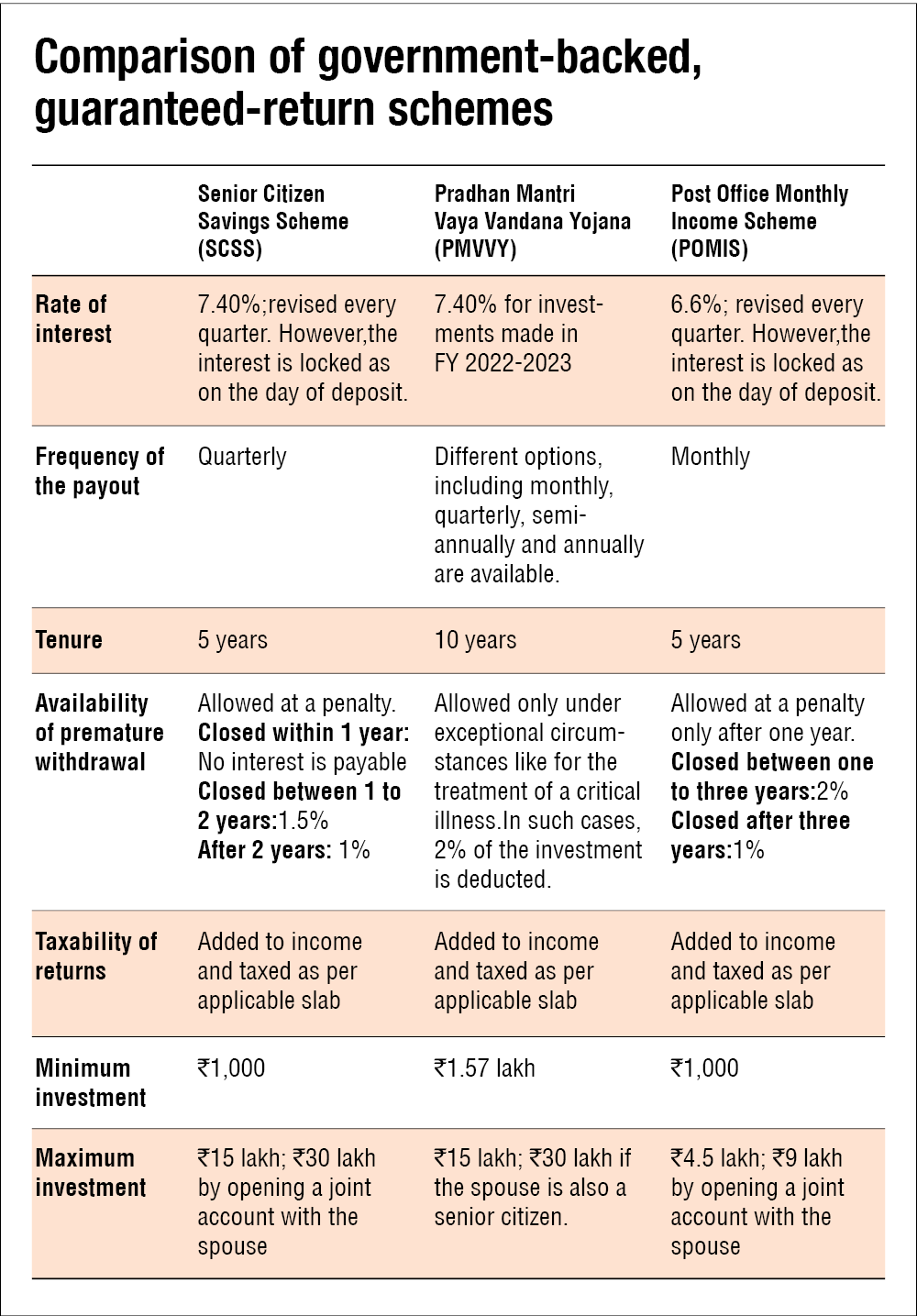

- While investing in fixed-income avenues to generate regular income, senior citizens should first utilise government-backed schemes, such as the Senior Citizen Savings Scheme (SCSS), the Pradhan Mantri Vaya Vandana Yojana (PMVVY) and the Post Office Monthly Income Scheme (POMIS).

- These schemes offer guaranteed returns, which are usually higher than those from any other fixed-income investments like bank fixed deposits. Also, since these schemes are backed by the Government of India, your investments in them will be absolutely safe.

Government and PSU bonds

- Right now, Sudeep is looking to invest an amount that is well within the maximum investment limit of the schemes mentioned above. However, the surplus, if any, can also be invested in bonds issued by the Government of India and PSU companies.

- These bonds are relatively safe but the interest-rate risk is still there. Also, by investing in these bonds alone, one may not be able to diversify.

- The RBI floating rate bonds are one of the safest fixed-income alternatives. Their interest rates are reset every six months and kept 35 basis points over and above the existing return on National Savings Certificate (NSC). The current return rate of these bonds is 7.15 per cent and the next reset will happen on January 1, 2023. Also, the interest is repaid twice a year - January and July. The interest earned on these bonds is added to the income and taxed as per the applicable slabs.

- Although these bonds have a tenure of seven years, premature withdrawals are allowed after the stipulated lock-in period, which is decided based on the age of the subscriber - six years for the age group of 60-70 years; five years for the age group of 70-80 years and four years for the age group of 80 years and above.

Corporate bonds and FDs

- Although corporate fixed deposits and bonds earn about 1-2 per cent more than bank FDs, they are not as much safe. It is like lending your money to a particular company.

- If Sudeep is ready to take a bit of risk, investing in a good short-duration fund would be a better idea, given the fact that his investment would be diversified among several such company bonds and deposits.

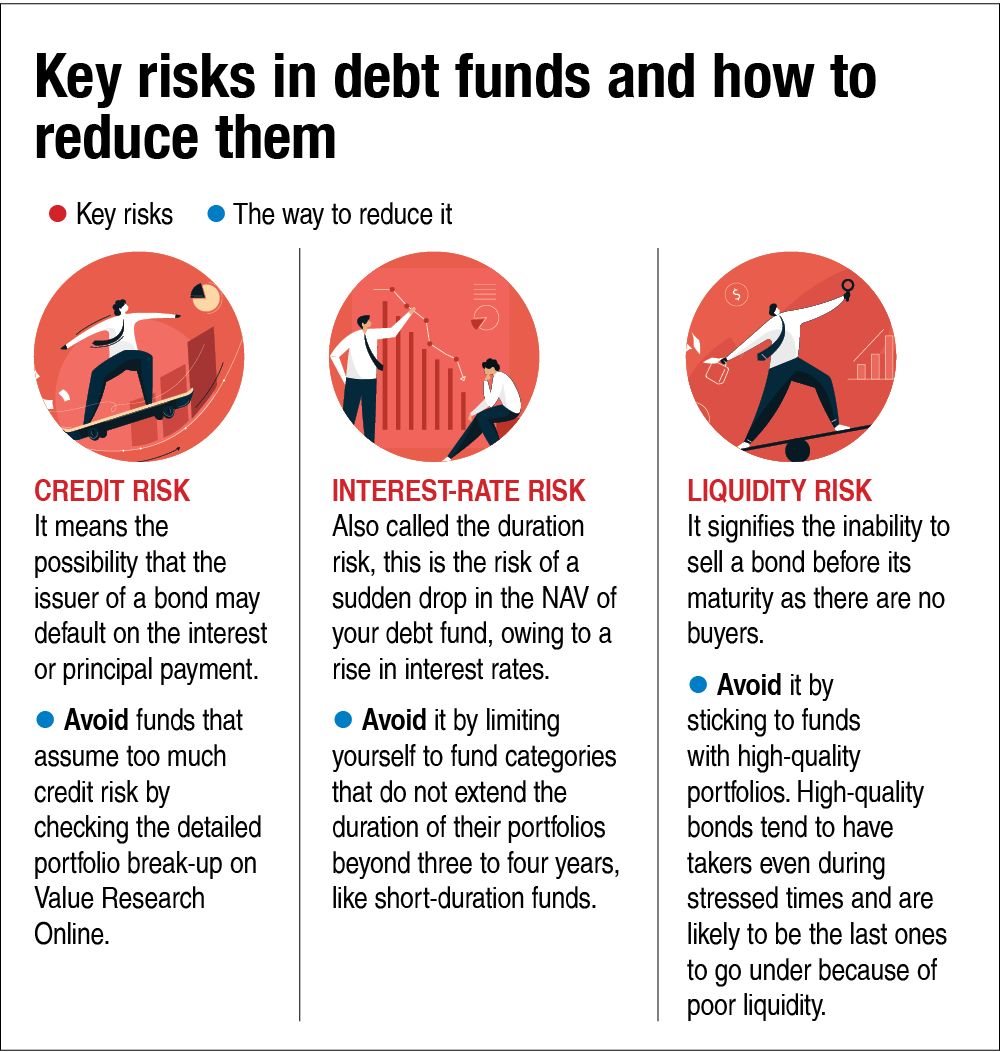

- Instances like the Franklin episode should not deter Sudeep from investing in debt funds altogether. Rather, it should be treated as a learning experience. Debt funds score higher on liquidity, returns and taxability

How to pick a debt fund after the Franklin episode?

- One must understand that risks are there in debt funds as well. Therefore, one must take all the precautions to reduce them.

- One should look for a well-diversified, high quality portfolio. It is better to avoid a fixed-income fund that is giving extra-ordinarily high returns than its peers. Do remember that extra return comes with extra risk.

- The new risk-o-meter is pretty informative and effective to assess the risk of a debt fund. One should also look at the risk grade, which is pictorially depicted and now changes every month with the portfolio.

Do not shun equities completely

- While it is true that equities are volatile, one must continue to invest at least one-third of the corpus in equities even after retirement. It will help one earn inflation-adjusted income.

- Ideally, the annual withdrawal should not exceed 4-6 per cent of the corpus.

- Relying only on fixed-income avenues may push you towards old-age poverty during the later years of retired life, owing to inflation. And if you invest only in fixed-income instruments, you need to have a sufficiently large corpus.

Don't ignore these

- Maintain a contingency fund equivalent to at least six month expenses in a combination of the liquid fund and sweep-in deposits.

- Have adequate health insurance for all your family members. You don't need life insurance unless you have financial dependents or enough net worth to financially support them in your absence.

This article was originally published on November 10, 2021, and last updated on September 28, 2022.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()