Benjamin Graham, the father of value investing said, "Confronted with a challenge to distill the secret of sound investment into three words, we venture the motto, margin of safety." The concept of margin of safety is central to value investing. It means that an investor should purchase a security when its market price is significantly lower than its intrinsic value. In the words of Warren Buffett, "When you build a bridge, you insist it can carry 30,000 pounds, but you only drive 10,000 pound truck across it. And that same principle works in investing."

At Value Research Stock Advisor, we fully understand this. That's why we go the extra mile in ensuring margin of safety in our stock recommendations. Margin of safety can have numerous facets. One of the ways in which investors bring this philosophy to investing is by applying the price-to-book (P/B) ratio. P/B is calculated as the market value of equity divided by the book value of equity. The market value of equity means market capitalisation, which is calculated by multiplying the number of shares by the market price per share. The book value of equity is the shareholders' equity or net worth.

Intuitively speaking, the lower the ratio (preferably closer to or less than one), the safer it is to invest in a stock. However, this is a very simplistic way of looking at valuation and is fraught with risks. The reason is contained in the calculation of P/B itself. The numerator, market value of equity, is forward looking and measures how excited the markets are about the future prospects of a company. The denominator, book value of equity, is backward looking and is governed by the accountant's valuation of assets and liabilities.

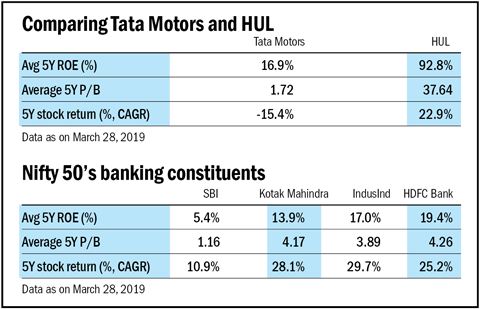

To understand this better, let us apply the P/B ratio to the entire spectrum of Nifty 50 stocks at the moment. With a P/B of 0.68, Tata Motors appears on the extreme left of the spectrum. Hindustan Unilever (HUL), on the other hand, appears on the extreme right, with a P/B of a whopping 52 times! What this means is that the markets are willing to give 32 per cent lower value to Tata Motors, compared to its book value. On the other hand, market is upbeat about HUL prospects and is giving it Rs 52 for every Rs 1 of book value.

So, going by the P/B yardstick, the shares of Tata Motors appear to be highly undervalued and those of HUL appear to be highly overvalued. The bargain sale of Tata Motors becomes even more convincing when we see that its shares have corrected by 56 per cent in the last one year, whereas the shares of HUL have appreciated by 30 per cent in the same interval. So, why are the markets not taking notice of the opportunity in Tata Motors and the overvaluation in HUL? The answer to this lies in the inherent flaws P/B suffers from, which restricts its applicability.

Flaws of P/B

Relying on P/B for valuation has many disadvantages. First, book value fails to capture the value of intangibles such as intellectual property, patents, formulas, trademarks, etc. This renders its applicability meaningless for industries such as IT, pharmaceutical, services, etc.

Secondly, book value does not reflect the current market value of assets, which appear at historical costs, adjusted for depreciation.

Thirdly, off-balance-sheet liabilities such as contingent liabilities, debt at a special-purpose entity, etc., may not be adequately represented in book value. This could be misleading as it artificially deflates liabilities.

Book value may also be unreliable on account of impairment of assets (such as goodwill or slow-moving items of inventory, etc.). Hence, in reality, the realisable value of assets could be markedly lower than the book value.

So, is it all curtains down for the P/B ratio, or does it have practical significance? The answer to this question is in the affirmative.

Usefulness of P/B

The P/B ratio has the following applications:

Easy to use: The ratio is preferred for ease of calculation and also for its intuitive appeal. However, being simplistic, it shouldn't be used in solitude.

Useful for capital-intensive companies and banks: It is useful for companies which have a higher proportion of fixed assets in their books. For banking companies, the ratio is avidly used as their assets and liabilities closely represent their current market value.

A substitute for P/E: The P/B ratio can still yield sensible results when the price-to-earnings (P/E) ratio breaks down. This happens when a company is loss-making. Further, as book value tends to be relatively stable, P/B is preferred when the earnings stream tends to be volatile.

Mean-reverting: P/B finds favour with investors who prefer the mean-reverting approach to investing. Such investors buy a stock when it falls below the median P/B and sell it when the price exceed the median.

P/B's companion is ROE

At Value Research Stock Advisor, we understand that tracking just one parameter can be misleading. When we see P/B, it is generally in conjunction with return on equity (ROE). ROE is calculated by dividing the net income by shareholders' equity. Its denominator is the same as that of P/B. High ROE companies earn a higher rate of return on the shareholders' equity. When these are again ploughed back into business and the company continues to earn higher rates of return, compounding of shareholders' wealth takes place at high rates.

Let us apply this to the Tata Motors-HUL example.

The story is not very different if this concept is applied to Nifty 50's banking constituents.

As may be seen, a lower P/B in itself is not enough for spotting winners and a high P/B does not necessarily imply that the stock is overvalued. A high ROE holds the key to value in the longer term.

Hence, outsized investment gains can be made when one spots the best combination of P/B and ROE. Stocks are undervalued when P/B is low and the estimated ROE is high. Stocks are overvalued when P/B is high and the estimated ROE is low.

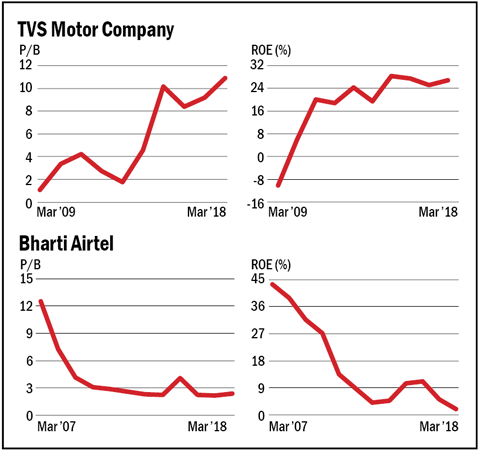

To illustrate this point, let us take the case of TVS Motors. The stock was trading at a P/B of one with an ROE of -10.5 per cent as of March 2009. It has turned around since then, with the ROE staging a continuous improvement to average 21.9 per cent between FY10 and FY18.

Those who spotted the trend early would have seen their investment register a 10-fold increase.

On the other side, let us analyse Bharti Airtel. The stock was trading at a P/B of 12.6 times with an ROE of 43.7 per cent as of March 2007. Its ROE kept on sliding on a continuous downward slope ever since then, averaging 14.2 per cent between FY07 and FY18.

Investors have lost 17 per cent of their investment value in the stock since FY2007.

This analysis illustrates that P/B has limited use. Avoid giving a high weight to this ratio in your research. If you do consider it, complement it with ROE. All in all, put it in some perspective. At Value Research Stock Advisor, we do such analyses all the time to find the best stocks. Hence, our subscribers always get stocks that don't have hidden negatives. We are ardent believers of Warren Buffett's statement, "Price is what you pay, value is what you get."

Sachin Kumar is Senior Equity Analyst at Value Research Stock Advisor.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()