India's farm animals need food and Godrej Agrovet provides it. It is India's leading compound animal feed provider based on installed capacity. It also makes money from dairy, crop protection, palm oil and poultry. The company operates out of 35 facilities to produce animal feed and has 4000 distributors. It was founded in 1991 and is primarily owned by Godrej Industries. The company has made several strategic acquisitions and joint ventures over time. In the process, it has diversified away from animal feed, reducing its share in revenues from 77% 2015 to 53% at present. Much of its future growth is likely to come from non-feed businesses such as palm oil and crop protection.

India's farm animals need food and Godrej Agrovet provides it. It is India's leading compound animal feed provider based on installed capacity. It also makes money from dairy, crop protection, palm oil and poultry. The company operates out of 35 facilities to produce animal feed and has 4000 distributors. It was founded in 1991 and is primarily owned by Godrej Industries. The company has made several strategic acquisitions and joint ventures over time. In the process, it has diversified away from animal feed, reducing its share in revenues from 77% 2015 to 53% at present. Much of its future growth is likely to come from non-feed businesses such as palm oil and crop protection.

The Pros

Revenue grew at a robust CAGR of 17% from 2013 while net income grew even faster at 28% CAGR. The secret sauce behind this growth has been Agrovet's acquisitions. The company bought Astec Lifesciences at a discount to its market price and managed it well. It's palm oil business has also done spectacularly. The company's segments have synergies - it deals with farmers as both suppliers and customers. It's vast distribution network is also a major advantage. Let us also not forget its parentage, the Godrej name evokes respect and trust.

The Cons

Agrovet's PE of 42 is anything but cheap. It operates in fairly competitive markets and faces large, deep pocketed rivals (Cargill in animal feeds, Venky's in poultry and Amul in dairy). Some of its business (such as palm oil) are heavily regulated and carry a significant regulatory risk. The company's ESOPs policy is remarkably generous. Its Managing Director was paid a remuneration of about 95 crores in FY 17, mostly through an exercise of ESOPs (its profit for the same period was about 273 crores). It does not have any formal licensing arrangements in place for use of the Godrej brand.

The acquisitions story

Godrej Agrovet acquired a stake in Creamline Dairy in 2005 to bolster its dairy business. It raised this stake to 52% in 2015. To get a leg up in the poultry business (heard of Real Good Chicken?), the company entered into a joint venture with Tyson Foods a major US company in 2008. In 2015, the company acquired Astec LifeSciences to enhance its crop protection and agrochemicals business.

Who's selling and how much?

Godrej Industries and V Sciences (a major shareholder) are selling part of their stake. Currently the promoters (primarily Godrej Industries) hold 68% and V Sciences holds about 20%. Post-issue, the promoter stake will fall to about 62% and V Sciences will see its stake will fall to 13%. There is also a fresh issue of shares worth 292 crores.

Offer

Fresh Issue: 292 crores

Offer for Sale (V Sciences+Godrej Industries): 865 crores

Purpose of fresh Issue

Primarily for repayment of working capital loans and commercial paper

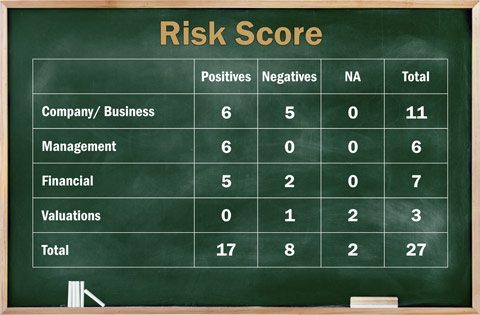

Company / Business

- Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes, the company's earnings before tax were 373 Crores in FY 2017. - Will the company be able to scale up its business?

Yes. Growth will come from segments such as dairy, palm oil and agro-chemical products. India is the world's largest palm oil importer and the Government is trying hard to encourage domestic production. In the agrochemical market, manufacturing is still dominated by high cost patent owning companies even as their products go off patent. This offers a major opening to low-cost producers such as Agrovet. - Does the company have recognizable brand(s), truly valued by its customers?

Yes. The company is part of the Godrej Group which has significant brand value associated with it. The company markets its product using the Godrej brand. However it has no formal licensing arrangement to use the this brand. - Does the company have high repeat customer usage?

Yes. The company develops products specific to the requirements of its consumers (animal feed). Once customer is accustomed to its product, the usage is regular. - Does the company have a credible moat?

No. The company operates in a highly competitive environment. Larger players introducing superior products having significant research capabilities and cost advantages can take business away from the company. - Is the company sufficiently robust to major regulatory or geopolitical risks?

No. Changes in regulations such as those dealing with the use of chemicals in agri-produce or affecting palm plantations can impact its business significantly. - Is the business of the company immune from easy replication by new players?

Yes. In order to sell its products to farmers located in various parts of the country, the company relies on the large distributor network that it has built over time. This cannot be easily replicated by new entrants. - Is the company's product able to withstand being easily substituted or outdated?

Yes. The company's products such as animal feed, milk, poultry and palm oil are essential products in various agricultural processes and are unlikely to be easily substituted or become outdated. - Are the customers of the company devoid of significant bargaining power?

No. The company faces intense competition from co-operative societies as well as private and unorganised players giving its customers plenty of choice. - Are the suppliers of the company devoid of significant bargaining power?

No. Except for its poultry business (where vendors are few in number), the company procures supplies from open market and is not dependent on a few suppliers. - Is the level of competition the company faces relatively low?

No. The company faces intense competition from co-operative societies as well as private and unorganised players for its agri-based businesses.

Management

- Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent in the company?

Yes. Godrej Industries Limited, the promoter of the company held 63.67% of the company as on March 31,2017. - Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The top three managers have more than 15 years of combined leadership. Two of the three have been with the company for more than 20 years. - Is the management trustworthy? Is it transparent in its disclosures which are consistent with Sebi guidelines?

Yes, we have no significant reason to believe otherwise. - Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes, we have no reason to believe otherwise. However the auditor has raised concerns about the remuneration paid to its Managing director in 2017 without full compliance with applicable legal provisions. - Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise. - Is the company free of promoter pledging of its shares?

Yes. No promoter holding is pledged.

Financial

- Did the company generate current and five-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes, the company's average five year ROE and ROCE were 33% and 41% respectively. Current ROE and ROCE stand at 30% and 33% respectively. - Was the company's cash flow-positive during the previous year and at least four out of the last five years?

Yes, the company's cash flow was positive during the previous year and four out of the last five years. - Did the company increase its revenue by 10 per cent CAGR in the last five years?

Yes. the company's revenue increased at a CAGR of 17% in last five years. - Is the company's debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes. Net debt to equity stood at 0.47x while the interest coverage was 5.3x.as on March 31,2017. - Is the company free from reliance on huge working capital for day to day affairs?

No. The company has to carry a large inventory. Its cash conversion cycle (the time taken for cash to become raw materials, finished goods and then cash again) is a relatively high 66 days. - Can the company run its business without relying on external funding in the next three years?

No. The company regularly procures working capital loans and other short term facilities to run its business and it will continue doing so in the future. - Have the company's short term borrowings remained stable or declined (not increased by greater than 15%)?

Yes. The company's short term borrowings have reduced from 1260 crores In March 2016 to 639 crores in March 2017, a fall of about 49%.

The Stock/Valuation

- Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No. The post IPO operating earnings yield of the company will stand at about 2.2% in its current price band. - Is the stock's price to earnings less than that of its peers on average?

Not Applicable. There are no suitable listed peers for Godrej Agrovet. In the current price band of 450-460, its PE ratio will be about 42. - Is the stock's price to book value less than that of its peers on average?

Not Applicable. There are no suitable listed peers for Godrej Agrovet. At a price band of 450-460, its price to book stands at about 8.3x.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()