Just Dial is one of the country's rare new-age business successes. Its business model hinges on signing up local businesses, services and products across categories. Users can call, SMS or browse on their phones or on the net for desired products and services. Unlike other e-commerce and mobile-related service providers that have raised billions in funding without any earnings to show, Just Dial has been operating at a profit in each of the last eight years. It also has ₹740 crore in cash.

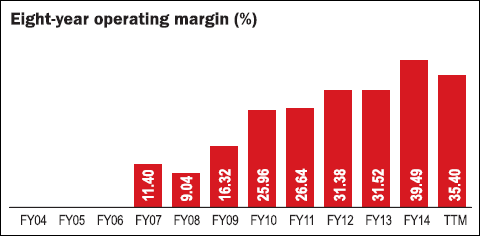

Profitability. EBITDA margins averaged at 26.5 per cent in the last five years. Q3FY15 saw margins expand 460 basis points (y-o-y) to 32.5 per cent on the back of lower ad spends. Margins could dip to 31 per cent in FY16 on higher ad spends, according to Kotak Securities, before moving to 40 per cent levels as premium search goes up.

Outlook. One of the biggest strengths of Just Dial is its first mover advantage, with a database of 14.7 million listings in about 2,000 Indian cities. It has one of the largest workforces in its sector - at around 9,000 - that add and update this database. Given the increased use of mobiles in search (35 per cent of the total searches are by mobiles), Just Dial appears best placed among competitors. The EPS has grown at 90 per cent annually in the last three years and could grow at 50 per cent and 80 per cent, respectively, in the next two years, says Kotak Securities.

Valuations. Just Dial trades at 72 times its earnings. This business is still in its investment phase but unlike other e-commerce players, Just Dial is not selling hopes of future earnings. It is making money today. Valuations, therefore, may remain elevated for some time. Wait for a market correction to buy.

This article was originally published on May 08, 2015.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()