Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

In 1974, a group of women in Ahmedabad walked into a government office. They wanted to start a bank.

They were street vendors. Head-loaders. Recycled-clothes sellers. They earned a few rupees a day. The government said they needed one lakh in share capital.

A woman named Chandabhen looked at the others. “We may be poor, but we are so many.”

With 6,287 women contributing Rs 10 each, they raised the capital. That bank became SEWA Bank — one of the first microfinance institutions in the world. Today, SEWA has 3.7 million members. Its loan repayment rate is 96 per cent.

Ten rupees. That’s where they started.

Not with a financial plan. Not with a PAN card. Not with a demat account. With ten rupees and the decision to begin.

This article is for you if you have money sitting in a savings account earning 3.5 per cent. Or gold sitting in a locker earning nothing. Or cash tucked between sari folds. If you’ve never taken the step into investing because it feels too complicated, too late, or too risky — it’s not. And you’re not behind. You’re exactly where millions of women start.

The two savings traps

Let me be honest about two things Indian women are told are “safe.”

The first is the bank fixed deposit. It feels safe because the number never goes down. Put in one lakh. Five years later, get back one lakh twenty-something thousand. But here’s what nobody mentions: inflation in India has averaged 6 per cent over the last decade.

If your FD earns 7 per cent and you pay tax on the interest, your real return — what your money can actually buy — is barely above zero. You’re not growing wealth. You’re running in place.

The second is gold. Indian households hold 25,000 tonnes of it. More than the reserves of five superpowers combined. Most sit in women’s jewellery boxes. Gold is extraordinary as a store of value. But physical gold doesn’t earn interest. It costs money to store. And selling it means melting something your mother gave you.

That’s not a financial decision. That’s an emotional hostage situation.

Don’t sell your gold. Don’t close your FDs. But add a third leg to the stool. The leg that actually grows.

The SIP: Your ten rupees

In Kerala, 4.5 million women are members of Kudumbashree. They save as little as a hundred rupees a week. During the 2018 floods, these women — saving a hundred rupees at a time — donated Rs 7 crore to the relief fund.

That matched Google and Apple. Exceeded the Gates Foundation.

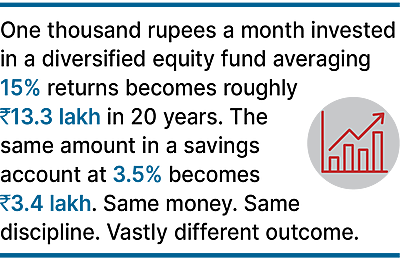

A hundred rupees a week. That’s the principle. Small, regular, disciplined amounts create extraordinary outcomes over time. That’s exactly what a Systematic Investment Plan — a SIP — does.

Here’s how it works. You invest a fixed amount every month into a mutual fund. You can start with Rs 500. The money auto-debits from your bank account. You don’t time the market, read stock charts, or watch business news. The SIP buys more units when prices are low, fewer when high. Time does most of the work.

What you actually need to start

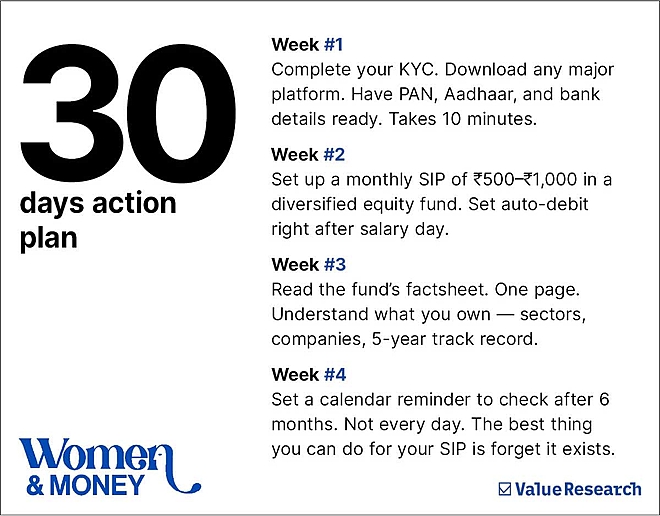

This is the part that stops most people. Not because it’s hard. Because nobody explains how simple it is.

You need three things: a PAN card, a bank account, and a completed KYC. That’s it. If you have Aadhaar and a smartphone, you can complete KYC online in 10 minutes. Most platforms — Groww, Kuvera, Coin by Zerodha, Paytm Money — walk you through it.

You don’t need a demat account. You don’t need a broker.

Let me repeat that: you don’t need anyone’s permission.

Addressing the fear

I know what you’re thinking. What if the market crashes?

Fair question. Let me answer it with a story.

In Solapur, Maharashtra, a vegetable vendor’s wife faced a choice. Her daughter, Swati, wanted to clear the UPSC exam. The family had almost nothing. The mother did the one thing in her power: she mortgaged her gold. Not sold. Mortgaged.

That distinction matters. Selling is permanent. Mortgaging is a bet. She wagered her only asset on the possibility that her daughter might, after five attempts, make it. Every year the exam wasn’t cleared, the interest grew. Swati finally cleared with an All India Rank of 492.

Investing in a mutual fund is the same kind of bet. But with better odds and lower stakes. You’re putting aside five hundred rupees a month. Betting on the Indian economy growing over the next ten to twenty years. India’s GDP has grown every decade since independence.

Short-term losses are real. Long-term growth is as close to certainty as investing gets.

The fear of loss is valid. But the cost of not starting is worse. Inflation doesn’t wait for you to feel ready.

Your first 30 days

Chandabhen started with Rs 10. Kudumbashree members started with a hundred a week. You can start with Rs 500 a month. The amount doesn’t matter. The act of beginning does.

You are not starting from zero. You are starting from now.

Her Money, Her Future • A 5-part Women’s Day special by Value Research

Next: The confidence gap is a knowledge gap

Ruchira Sharma, Senior Editor, Narrative & Long-form | Value Research

She writes about money the way it actually lives in Indian families, tangled with culture, silence, gold, and love. At Value Research, she anchors Investors' Hangout and Fund Manager Interviews, narrates Dhirendra Kumar's First Page, and leads the audio-visual team. Her Money, Her Future brings together her two crafts: the journalist's instinct for the untold story and the financial editor's demand for evidence in every sentence. Previously, 14 years at India Today: scripting, production, and long-form storytelling.

This article was originally published on March 06, 2026.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()