Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Let me tell you about an almirah.

Not a fancy one. A regular steel Godrej almirah. The kind that lives in the corner of every middle-class Indian bedroom. The kind whose key hangs from a hook that only one person in the house knows about.

In February 2026, a woman in Uttar Pradesh was cleaning hers out. Bundles of old five-hundred and thousand-rupee notes tumbled from between stacked saris. She had hidden them from her husband before demonetisation. That was November 2016. She had then, in the chaos of those weeks, simply forgotten.

Her daughter filmed the moment. Posted it on Instagram. Guys, ab mummy ro rahi hai. The mother stands, clutching worthless paper, asking whether banks will still accept them. The video went viral. The most liked comment: Papa ka reaction bhi post karna.

Everyone laughed. Honestly, it is funny.

But sit with that story for a minute.

This woman had money. Not a lot, but some. She had saved it for months or years, skimming carefully from the household budget. She hadn’t spent it on herself. She had hidden it — not in a bank account, not in a fixed deposit, not in a mutual fund. Between sari folds in a steel almirah. Because that was the only financial institution available to her. Her own cupboard.

Millions of Indian women maintain these secret reserves. Hidden in almirahs, between sari folds, inside kitchen containers. A parallel economy of survival. No finance minister has ever accounted for it.

Her savings were not investments. They were insurance. Against a husband’s temper. Against a medical emergency where she’d have to ask permission before spending. Against being told “yeh paisa kahan se aaya?”

Demonetisation didn’t just invalidate currency. For women like her, it invalidated years of quiet, invisible financial planning.

This article is about that almirah. About the millions of Indian women who manage household budgets brilliantly — but have never been told where the family’s investments are. What insurance exists? Whether a will has been written. About what that silence costs. And who pays the price?

The architecture of exclusion

Here’s the thing about financial exclusion in Indian families. It doesn’t look like exclusion. It looks like love. It sounds like tum tension mat lo, main dekh lunga. It sounds like arre, yeh sab tumhe samajhne ki zaroorat nahi. It sounds like protection. And that’s exactly why it works so well.

Women are included in spending decisions. What to buy for the kitchen. Which school should the children attend? Whether to renovate the bathroom this year or next. These require real intelligence, planning, and trade-offs. Indian women are extraordinarily good at them.

Anyone who has watched a middle-class Indian mother stretch a monthly budget across groceries, school fees, medical bills, festival expenses, and gifts for relatives knows this. That is not budgeting. That is financial engineering without a spreadsheet.

But spending is not wealth-building. And this is where the wall goes up.

Investment decisions happen in a different room. Insurance decisions happen there, too. Estate planning — whether a will exists, what it says, how property is divided — sits behind the thickest door. Women are rarely invited in.

Not because anyone deliberately locked them out. Because the architecture was built this way. Nobody thought to renovate.

Think about it. A father sits his son down. Explains the family’s finances — the fixed deposits, the property papers, the locker at the bank. He doesn’t sit his daughter down for the same conversation. Not because he loves her less. Because he assumes she’ll marry into another family. Her husband will handle “all that.”

The daughter doesn’t demand the conversation. She’s never seen her mother have it. The silence reproduces itself. Generation after generation. Nobody notices.

Literature knew before the data did

Indian writers saw this a century ago. They told this story before any survey confirmed it.

In 1936, Premchand published Godan — arguably the greatest Hindi novel ever written. Dhania, the protagonist’s wife, is a formidable financial mind. She argues. She strategises. She makes sharp economic calculations about every transaction. But she operates entirely within the domestic economy — the price of grain, the cost of a wedding, the debt owed to the moneylender.

The larger decisions about land, loans, and the family’s survival are made by the men. Often disastrously. Dhania sees the disaster coming. She warns against it. Nobody listens.

The family’s ruin is not caused by her ignorance. It is caused by her exclusion from the room where decisions are made.

Now read what R K Narayan wrote two years later. In The Dark Room (1938), Savitri’s husband controls every rupee. When he taunts her — “no end of expenses, money for this and money for that” — she has no answer. Not because she lacks courage. Because she lacks a bank balance.

Narayan wrote in his memoir that he was “obsessed with a philosophy of Woman as opposed to Man, her constant oppressor.” A man who assigned her a secondary place “with such subtlety and cunning that she herself began to lose all notions of her independence.”

Read that line again. That is the most precise description of financial exclusion ever written. It doesn’t happen with a locked door. It happens with a smile and a reassurance.

Fifty years later, Shashi Deshpande wrote That Long Silence (1988). Jaya is educated. Upper-middle-class. A writer in Bombay. When her husband is caught in financial fraud, she discovers she knows almost nothing about the family’s finances. The investments, the accounts, the legal exposure — all existed in a world she was never invited into.

Three writers. Three eras. Three regions. Three languages. One identical story. A capable woman is locked out of the room where financial decisions are made.

If literature is a mirror, this mirror has shown us the same reflection for a hundred years. We just haven’t looked.

But women have always known money

Here’s what makes this complicated. And more interesting than a simple tale of exclusion.

Indian women have never been passive bystanders in the economy. In many communities and many eras, they have been the economy. The problem isn’t that women don’t understand money. The problem is that the formal financial system was built as if they don’t.

Consider kitty parties. Yes, kitty parties.

A group of 12 to 20 women contribute a fixed monthly sum. Each month, one member receives the entire pool. The cycle continues until everyone has received the kitty once. India has an estimated 15,000 kitty-party organisations. The repayment rate is near-perfect. Enforced not by contracts, but by social trust.

Kitty parties emerged in post-Partition India. Displaced families needed savings mechanisms. Banks wouldn’t lend to women without a steady income. What started as survival became a permanent institution. Rural women use kitty proceeds for school fees. Urban women fund everything from appliances to business start-ups.

And then there is the most astonishing number of all.

Indian households hold 25,000 tonnes of gold. Eleven per cent of the world’s supply. More than the reserves of the US, Germany, Italy, France, and Russia combined. Value: two trillion dollars. Most of it sits in women’s jewellery boxes.

The Supreme Court has ruled that stridhan — gold given to a woman at marriage — belongs solely to her. Cannot be claimed by husband or in-laws. Even during divorce. Yet many women maintain gold as secret reserves.

This isn’t jewellery. It’s the world’s largest women-controlled sovereign wealth fund. No CEO. No annual report. No board of directors. Just almirahs.

So here is the paradox. Indian women are simultaneously among the most financially active people in the country and among the most financially excluded. They run a parallel economy that the formal economy pretends doesn’t exist.

The cost of not knowing

Every system of exclusion has a price. The bill always lands on the person kept in the dark.

Think about widowhood. In one day, a woman goes from budget manager to needing to know everything. Bank accounts. Fixed deposits. Insurance policies. Property papers. PAN numbers. Nominee forms. If her husband handled “all that,” she may not know which bank held the salary account.

Or think about divorce. When Pooja Sharma, a Delhi resident, walked away from her marriage, her husband kept her gold. Gold that was legally her stridhan. Her absolute property under the law. She lost it not because the law failed her. Because nobody told her the law existed.

Or think about scams. In December 2025, a Pune homemaker ordered a Biba dress online for Rs 1,700. A scammer sent QR codes. Over two days, she made 10 UPI transactions totalling Rs 6,82,000. She had never handled a UPI transaction before her husband set up the app.

The mothers who knew different

The generational loop is the saddest part. A mother excluded from financial conversations raises a daughter who accepts exclusion as normal. The silence inherits.

But it doesn’t have to. We know this because other models exist. Within India itself. Within living memory.

In Manipur, Ima Keithel — the Mothers’ Market — has been run entirely by women for five hundred years. Over five thousand vendors. Stalls passed mother to daughter. The market’s own union runs a credit system for traders. An indigenous financial institution that predates modern microfinance by centuries.

In Ahmedabad, in 1974, self-employed women decided to start their own bank. Told they needed one lakh in share capital, a woman named Chandabhen declared: “We may be poor, but we are so many.” With 6,287 women contributing Rs 10 each, they raised the capital. SEWA now has 3.7 million members.

In Kerala, 4.5 million women in Kudumbashree save a hundred rupees weekly. During the 2018 floods, they donated seven crore to the relief fund. Matched Google and Apple. Exceeded the Gates Foundation.

These are not fairy tales. These are real institutions proving that when women start the money conversation themselves, the results are extraordinary.

What we lost along the way

Here is a history most of us don’t know. In ancient Indian law, women had absolute property rights. The concept was called stridhan — from Sanskrit: stri (woman) + dhan (wealth). All gifts given to a woman before, during, or after marriage. Plus any property she earned herself. Hers alone. Neither husband nor in-laws had a legal claim.

The British destroyed this. The Hindu Inheritance Act of 1928 allowed only male heirs to inherit. Families began “compensating” daughters with gifts at marriage. Voluntary stridhan became coerced dowry.

What we call “dowry” today is not an ancient tradition. It is a colonial-era distortion of a system designed to protect women’s financial independence.

Premchand dramatised this transformation in Nirmala (1927). When Nirmala’s father dies, the groom’s family withdraws. Not because of any flaw in Nirmala. Because the anticipated dowry has evaporated. The result: a mismatched marriage to a man twenty years her senior. Suspicion. Jealousy. Tragedy. Premchand saw, a hundred years ago, the moment when women’s wealth became women’s burden.

Section 14 of the Hindu Succession Act, 1956, attempted to restore what was lost. The 2005 Amendment extended coparcenary rights to daughters. The law is slowly walking back. But law alone cannot undo a century of cultural programming. The conversation has to change, too.

The conversation that needs to happen now

So, where does this leave us? With a paradox and a checklist.

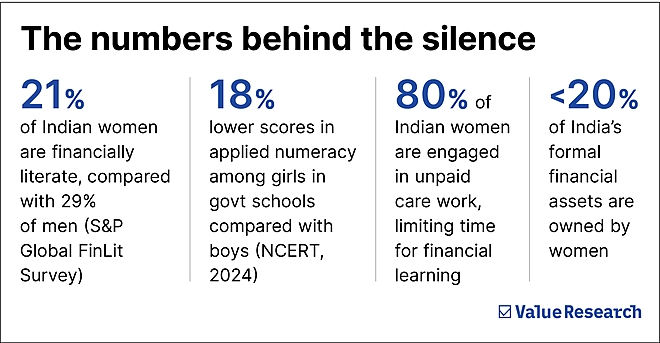

The paradox: Indian women are some of the most financially competent people in the country. And some of the most financially excluded. They can stretch a household budget to breaking point. Negotiate gold prices with a jeweller. Run a kitty party with the precision of a fund manager. But ask where the term insurance policy is, and the answer is silence.

That silence was built. By a culture that confused protection with exclusion. By colonial laws that stripped women’s property rights. By a financial system designed by men for men. By families that taught daughters to cook, sew, study, and marry — but never to read a bank statement.

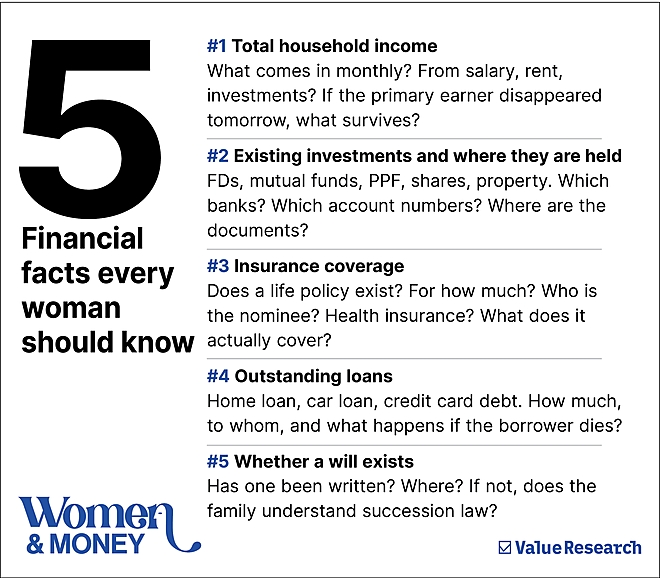

Breaking it requires five conversations. Five questions. Five facts every woman should know.

This is not about becoming a financial expert overnight. It is about refusing to be the last person in the room to know what’s happening with your own family’s money.

Remember that woman in Uttar Pradesh? Clutching her demonetised notes? She didn’t lack financial instinct. She had saved, systematically, from whatever she could access. What she lacked was the conversation with her husband, with a bank, with anyone who would have turned hidden notes into an actual investment.

That conversation didn’t need a finance degree. It needed permission.

Start today. Open the almirah. And this time, don’t hide anything in it. Ask.

Her Money, Her Future • A 5-part Women’s Day special by Value Research

Next: Starting from zero

Ruchira Sharma, Senior Editor, Narrative & Long-form | Value Research

She writes about money the way it actually lives in Indian families, tangled with culture, silence, gold, and love. At Value Research, she anchors Investors' Hangout and Fund Manager Interviews, narrates Dhirendra Kumar's First Page, and leads the audio-visual team. Her Money, Her Future brings together her two crafts: the journalist's instinct for the untold story and the financial editor's demand for evidence in every sentence. Previously, 14 years at India Today: scripting, production, and long-form storytelling.

This article was originally published on March 05, 2026.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()