Summary: A decade ago, active mid-cap funds won 68 per cent of the time. Now it’s just 26 per cent. Dive into the data behind this dramatic reversal, the structural changes hurting fund returns and whether passive mid caps are the smarter bet going forward.

If an investor had asked a decade ago whether to invest in mid caps through a passive route, the answer would have been a firm no. In the years following the global financial crisis, actively managed mid-cap funds consistently beat their benchmark, maintaining an edge of around four to five percentage points.

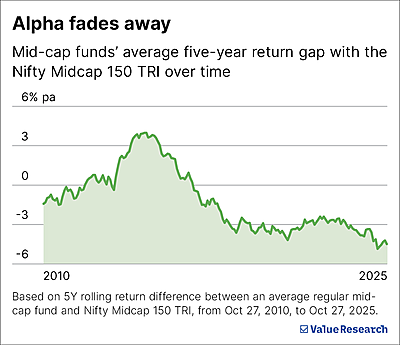

Ask the same question today, and the answer is no longer clear-cut. Some would argue yes, others would hesitate. What has changed in this time? The answer lies in the graph titled ‘Alpha fades away’, which shows how the average performance of mid-cap funds has shifted against their benchmark, the Nifty Midcap 150 TRI. While the early weakness could be explained by the side-effects of 2008, the long-term pattern tells a different story—a steady erosion of alpha. Over the years, the category’s outperformance of roughly 4 per cent has turned into an underperformance of similar magnitude.

When alpha changes sides

For several years, fund managers operated in an environment without rigid definitions for large, mid and small-cap categories. This allowed them a degree of flexibility in portfolio construction. A mid-cap fund could hold select large or emerging small-cap names as part of its strategy, provided the portfolio broadly maintained its intended market-cap orientation. This flexibility seems to have worked to investors’ advantage, enabling fund managers to capture opportunities across the spectrum and generate consistent alpha.

That flexibility, however, came to an end when SEBI introduced a uniform categorisation framework, clearly defining the investment universe for each fund type. The move brought greater clarity and comparability across schemes, but it also confined each category to a narrower set of stocks. The timing was unfortunate. These definitions came into effect in the first half of 2018, just as mid-cap and small-cap stocks began to correct. The newly imposed limits meant that fund managers had little room to reposition portfolios during the downturn. Even through the strong bull run that followed over the next five years, both categories have found it difficult to deliver meaningful outperformance over their benchmarks. Mid caps, often viewed as the ideal blend of growth and stability, have also felt the pinch.

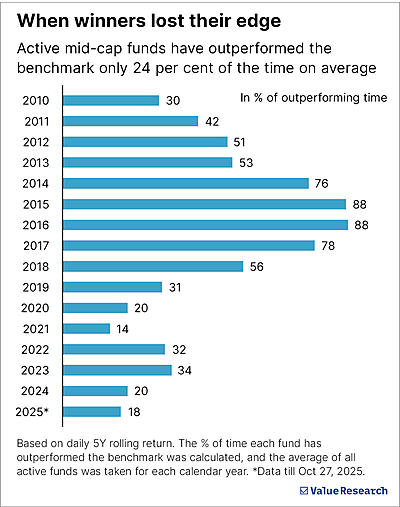

To test this, we examined the daily five-year rolling returns of all mid-cap funds and compared them with their benchmark over the last 15 years. We asked a simple question: on average, for what percentage of time did the average active mid-cap fund outperform the benchmark? Dividing the data into two periods, 2010–2017 and 2018 onwards, yielded a stark contrast. Between 2010 and 2017, the average active mid-cap fund beat their benchmark 68 per cent of the time, a healthy record for active management. Since 2018, that figure has plunged to just 26 per cent.

When viewed year by year, the decline is even clearer. The graph titled ‘When winners lost their edge’ shows the percentage of time, each calendar year, that the average active mid-cap fund outperformed the Nifty Midcap 150 TRI. The trend forms a downward slope that mirrors the category’s fading dominance.

The case for mid-cap investing

This slide in active fund performance, however, should not be mistaken for weakness in the mid-cap segment itself. The mid-cap universe continues to deliver impressive long-term returns and remains a vital component of diversified portfolios.

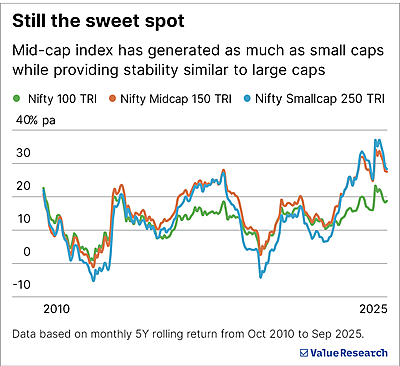

As the graph titled ‘Still the sweet spot’ shows, the Nifty Midcap 150 TRI has generated returns comparable to small caps while displaying volatility closer to large caps. That stability stems from mid caps’ unique position in the corporate lifecycle. These are companies with established business models and proven profitability, yet they retain enough runway for meaningful growth. For investors who often have to choose between the safety of large caps and the thrill of small caps, mid caps offer a compelling middle path.

A no-go for active investing?

Despite the structural headwinds, the decline in category-wide alpha does not imply that investors should avoid active mid-cap funds altogether. Some funds have still managed to deliver exceptional performance. It’s just that the narrower playing field simply demands deeper research, disciplined stock selection and sharper conviction from fund managers.

Yet, the case for passive investing in this space is strengthening. The steady erosion of alpha suggests that for many investors, especially those who prefer simplicity and cost efficiency, index options now deserve serious consideration.

That said, there is one practical limitation. Passive investing in mid caps remains underdeveloped in India. Investors currently have only five choices; four exchange-traded funds (ETFs) and a single index fund, with an AUM of just Rs 2,631 crore. Liquidity, particularly in ETFs, is still a concern. So, even if passive investing in India remains heavily tilted towards large caps, it may take time before mid caps see comparable depth and accessibility.

Moreover, performance cycles in equity markets are never permanent. The underperformance of active mid-cap funds over the last seven years could prove temporary. Should the market structure or valuation dispersion change, active managers could regain their footing.

Still, the data speaks plainly. Alpha in mid caps has become far harder to generate. The balance between active and passive strategies is tilting, slowly but unmistakably, towards the latter.

This article was originally published on November 20, 2025.

Ask Value Research ![]()