Ever wondered what happens when a government spends more than it earns? Think of it like running up your credit card bill. If the money's spent wisely - say, on education or infrastructure - it's an investment in the future. But if it's all going towards dining out and impulse buys, you've got a problem. This gap between what the government spends and what it earns is called the fiscal deficit, and it's one of the most important indicators of a country's financial health.

For 2024-25, India's fiscal deficit is projected at Rs 16.13 lakh crore, or 4.9 per cent of GDP. But don't let the numbers scare you - let's break it down into bite-sized pieces so you can sound like an economist without breaking a sweat.

What is fiscal deficit?

Simply put, the fiscal deficit is the amount the government needs to borrow to cover its expenses. It's the difference between total spending and total revenue (excluding borrowings). But there's more to it than meets the eye. A moderate fiscal deficit can actually fuel growth by funding infrastructure, healthcare, and education. The trouble starts when deficits run too high for too long, leading to rising debt, inflation, and a jittery economy.

Breaking down the components

Let's zoom in on what makes up a fiscal deficit:

- Revenue deficit: This is when the government's day-to-day expenses — like salaries and subsidies — exceed its earnings. For 2024-25, India's revenue deficit is estimated at 1.8 per cent of GDP.

- Primary deficit: This excludes interest payments from the fiscal deficit, showing how much borrowing is purely for new expenses.

- Effective revenue deficit: Think of this as the revenue deficit adjusted for grants used for capital expenditure, giving a sharper view of operational imbalances.

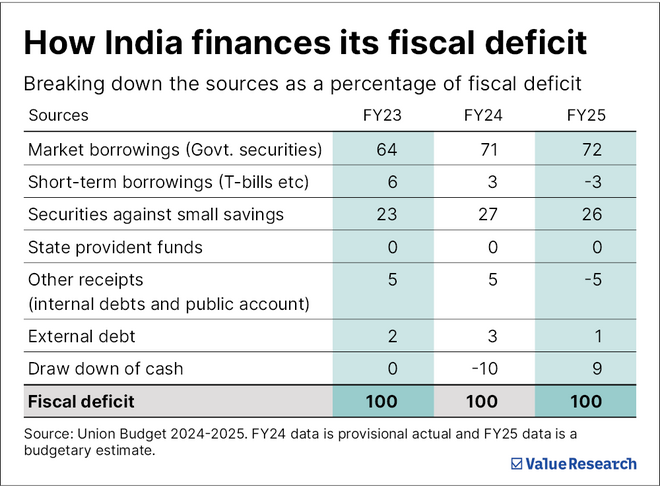

How does the government finance the fiscal deficit?

When expenses outweigh earnings, the government taps into these key sources:

- Market borrowings: Issuing bonds and securities that investors buy, effectively lending money to the government.

- Small savings schemes and provident funds: Using funds from schemes like Public Provident Fund (PPF) and National Savings Certificates (NSC) — basically borrowing from citizens.

- Foreign loans: Borrowing from international institutions like the World Bank or issuing bonds in global markets.

A lesson from history: The 1991 crisis

Back in 1991, India's fiscal deficit soared past 8 per cent of GDP, triggering a balance of payments crisis. Foreign reserves dried up, forcing the government to pledge gold and implement sweeping reforms. This wake-up call put fiscal discipline at the forefront of India's economic strategy, shaping policies for decades to come.

How to interpret fiscal deficit

Understanding fiscal deficit is about more than just numbers — it's about context:

- Trends over time: Is it rising or falling? For 2024-25, the slight reduction signals fiscal prudence.

- Global comparisons: Advanced economies can sustain higher deficits, but for developing nations like India, careful management is key.

- Productive vs. unproductive spending: Borrowing to build highways? Smart. Borrowing to pay routine bills? Not so much.

Balancing growth and stability

Think of fiscal deficit as the government's financial tightrope walk - it's not about eliminating the gap entirely but managing it smartly. Policies like rationalising subsidies, broadening the tax base, and encouraging private investments are crucial to reducing dependency on borrowing. Just like with your credit card, the key lies in spending wisely and borrowing within limits. As India navigates a changing global economy, how we handle the fiscal deficit today will determine the economic landscape for years to come. And hey, next time someone throws the term "fiscal deficit" into conversation, you can drop some knowledge like a pro!

Keep playing "Budget Lingo"

Revisit the previous term: Union Budget explained: What it is and why it matters

Learn the next term: Revenue deficit demystified: Is the government overspending?

Stay with us as we continue to decode the terms that demystify India's Union Budget.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()