NMDC Ltd., a government-owned enterprise, is India’s single largest producer of iron ore. This navaratna company is fully under the administrative control of the Ministry of Steel. Its principal operations include the running of three iron-ore mines at Kirandul and Bacheli in Chhattisgarh, Donimalai in Karnataka; and one diamond mine at Panna.

Sources of moat

Large reserves of high-grade iron ore. The company has access to large proven and probable reserves of high grade iron-ore, consisting principally of hematite ore with a ferrous content greater than 64 per cent. Greater the ferrous content of iron-ore, the more sought after it is in steel manufacturing. Its high grade ore quality gives NMDC a strong competitive advantage and helps it command premium pricing and strong customer loyalty.

India’s largest iron ore producer. NMDC is the largest producer of iron ore by volume, producing around 13 per cent of the country’s iron ore output. It produced 2.38 crore tonnes of iron ore in FY10. Being such a large producer puts it in a strong negotiating position vis-à-vis buyers.

Low-cost producer. The company’s cost of production compares favourably with that of the world’s leading iron ore producers. It is seeking to further lower its costs across all its operations. Some of the factors that contribute to the company’s low cost of production include the mechanisation of its mines, continuous focus on reducing cost of mining, seeking improvements in operational efficiency, including logistics, and its access to a large and inexpensive pool of labour and talent in India.

In-house exploration capability. The company possesses strong in-house capability for undertaking exploration aimed at expanding its reserves. It is also using this capability to try and diversify into the production of other minerals besides iron ore. The company has a large research and development centre at Hyderabad which is capable of taking up assignments in the field of iron ore beneficiation and mineral processing.

What could cause moat to be breached

Rise in input costs. The company’s competitiveness and long-term profitability in large measure depend on its ability to maintain a low-cost base, including low labour and transport costs.

In recent times, the company has incurred increased insurance cost as a result of increased terror threats from Naxalites and other insurgent groups operating around its mines and areas of operation. Its labour cost has increased significantly over the last two years, partly due to increased competition for skilled labour. Therefore, any increase in input costs could have an adverse effect on the company’s business and could reduce its cost competitiveness.

Intense competition. The company’s business depends upon obtaining and maintaining leases to mining sites, some of which are in the process of renewal. Intense competition from the private sector in securing fresh mining leases could affect the company’s profitability and operating margins.

Ability to access mineral reserves. With the passage of time, mineral reserves decline. The company’s future results and margins will depend upon its ability to access mineral reserves with geological characteristics that allow mining at competitive costs. Replacement reserves may not be available when required. If available, they may not be of a quality capable of being mined at costs comparable to that incurred in mining from earlier mines.

Moreover, the company may err in assessing accurately the geological characteristics of any reserves that it acquires. This could lead to a situation where the company’s existing iron ore reserves cannot be mined at competitive costs.

Concerns

Expiration of contracts. The company generates a significant portion of its revenue from certain key customers. In particular, Rashtriya Ispat Nigam Limited (VSP) and Essar Steel Limited together accounted for 37 per cent and

39 per cent respectively of revenues from the sale of iron ore in FY09. The company generally enters into five-year contracts with its customers. Many of the current agreements for exports, for instance, are due to expire in 2011. Although the company has entered into long-term contracts with certain key customers, there is always the risk that the counterparties to such contracts may not fulfil their contractual obligations or that on expiration these contracts may not be renewed.

Price volatility. Selling price and volume in the iron ore mining industry both depend on the prevailing and expected level of demand for iron ore in the global steel industry. The global steel industry is cyclical in nature. A number of factors influence the state of this industry, the most significant being the global demand for steel products. During periods of sluggish or declining regional or world economic growth, demand for steel products generally decreases. This leads to corresponding reduction in the demand for iron ore.

Prices of steel products are influenced by many factors, including demand, worldwide production capacity, capacity-utilisation rates, raw-material costs, exchange rates, trade barriers and improvements in steel-making processes. Accordingly, any significant decrease in either the demand or the price of steel products has the potential to affect both the demand and the price of iron ore. This would have an adverse effect on the company’s revenues.

Attacks by insurgent groups. Some of the company’s mining facilities are located in areas that are exposed to the risk of attacks by insurgent groups. Such attacks may disrupt its operations.

Inability to retain key personnel. The company is in particular dependent on the continued service and performance of its senior management team and other key team members in its business units. It does not maintain key man life insurance for certain of the senior members of its management team, its other directors, and other key personnel. Competition for senior management is intense in this industry and NMDC may not be able to retain senior management personnel or attract and retain new ones in future. These key team members possess technical and business capabilities that are hard to replace. The loss or diminution in the services of the company’s senior management or other key team members could have an adverse effect on the company’s business, operational results, and financial performance.

An iron ore producer like NMDC also faces the risk high inventory accumulation and difficulty in its disposal in times of suppressed demand.

Growth drivers

NMDC proposes to augment production of iron ore from the current level of 30 million to 50 million tonnes by 2015. It has also chalked out plans for value addition by setting up pelletisation plants in Chhattisgarh and Karnataka, and setting up an integrated steel plant in Chhattisgarh. NMDC is also planning to venture into the mining of coal and other minerals.

Financials

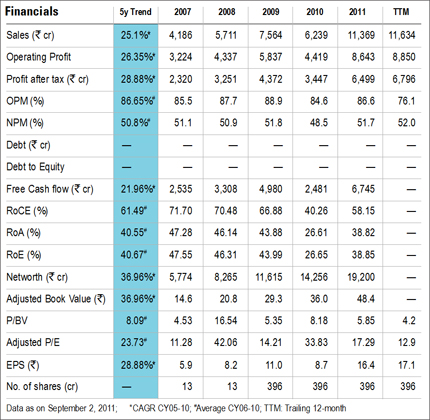

NMDC is a zero-debt company. Over a span of five years, the free cash flow of the company has increased at a compounded annual growth rate (CAGR) of 21.96 per cent. During this period it has delivered a five-year average return on capital employed of 61.49 per cent and return on net worth of 40.67 per cent.

Valuation

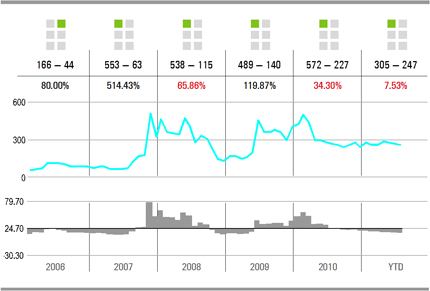

The stock is currently trading at a price-to-earnings ratio (P/E) of 12.93 which is much lower than its five-year median P/E of 24.57. Over the last five years its earnings per share has grown at a CAGR of 26.83 per cent, which translates into a price-earnings to growth (PEG) ratio of 0.48 times. An investor with a horizon of at least five years may invest in this resource-rich company.

This article was originally published on September 13, 2011.

Ask Value Research ![]()